Int'l : +1-503-894-6022 | Toll Free : +1-800-792-5285 | help@alliedmarketresearch.com

A01200 | Pages: NA | Charts: NA | Tables: NA |

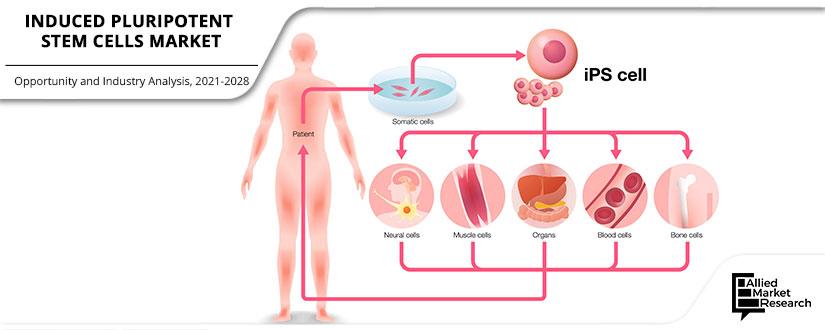

Pluripotent stem cells are embryonic stem cells that have the potential to form all adult cell types and help in repairing of damaged tissues in the human body. An induced pluripotent stem cells, or iPSCs, are taken from any tissue (usually skin or blood) from a child or an adult and is genetically modified to behave like pluripotent stem cells or embryonic stem cells.

Induced pluripotent stem cells market is in emerging state mainly due to its ability to make any cell or tissue the body might need to encounter wide range of diseases like diabetes, spinal cord injury, leukaemia or heart disease, these cells can potentially be customized to provide a perfect genetic match for any patient. Furthermore, these cells are very useful in understanding the earliest stage of human development and offer the opportunity to create customized, rejection-proof cells and tissues for transplantation. Also, government and private sectors are increasing funding and growing industry that focuses on different research work related to iPSCs and people are getting more aware about the stem cells through different organisations. However, factors such as high cost associated with the reprograming of cells, ethical issues and lengthy processes are impeding the induced pluripotent stem cells market growth. Low efficiency, potential tumor risk and incomplete programming are added factors limiting iPSCs market growth.

The global iPSCs market has been segmented based on derived cell type, application, end-user and geography. Based on derived cell type, the market is segmented into hepatocytes, fibroblasts, keratinocytes, amniotic cells and others. Based on application, the market is segmented into academic research, drug development and toxicity testing and regenerative medicine. Based on end-user, the market is segmented into hospitals and research laboratories. The market is analyzed on the basis of four regions, namely, North America, Europe, Asia-Pacific, and LAMEA.

Product launch, collaboration & merger, and acquisition are the key strategies adopted by market players. Healthcare giant such as Fujifilm Holding Corporation has acquired Cellular Dynamics International, Inc. in March 2019 creating a high growth in iPSCs market. Also, Juno Therapeutics and Fate Therapeutics collaborated to improve the products market.

Comprehensive competitive analysis and profiles of major market players such as Fujifilm Holding Corporation, Astellas Pharma Inc., Fate Therapeutics, Inc., Bristol-Myers Squibb Company, ViaCyte, Inc., Celgene Corporation, Aastrom Biosciences, Inc., Acelity Holdings, Inc., StemCells, Inc., Japan Tissue Engineering Co., Ltd. and Organogenesis Inc. is also provided in this report.

KEY MARKET BENEFITS:

Key Market Segments

Key Market Players

{kind=link}