5G Femtocell Market Overview

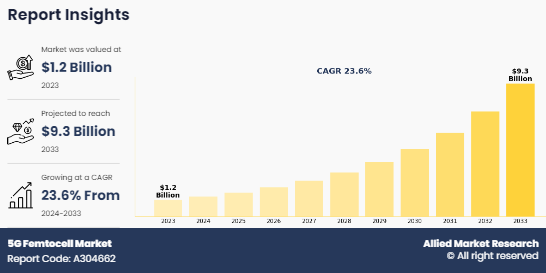

The global 5g femtocell market was valued at USD 1.2 billion in 2023, and is projected to reach USD 9.3 billion by 2033, growing at a CAGR of 23.6% from 2024 to 2033.

A 5G femtocell is a small cellular-base station that offers enhanced indoor coverage and capacity for 5G networks. It works by leveraging existing internet connections to extend the reach of cellular networks, particularly in poor coverage areas and high user concentration, such as homes, offices, and public places. Furthermore, 5G femtocell play a vital role in the expansion and optimization of 5G networks, offering improved indoor coverage, enhanced capacity, and cost-effective solutions for network operators, thereby offering better user experiences and increased connectivity in both residential and commercial areas.

The 5g femtocell market is segmented into Deployment, Application, End User and Network Type. The growth of the global 5G femtocell market is majorly driven by rise in remote work culture coupled with rapid digitalization and increase internet penetration. In addition, the growth in adoption of 5G technology across the world strengthens the market growth. Moreover, the surge in demand for high-speed, low-latency connectivity in indoor environments and increase in deployment of 5G networks and Internet of Things (IoT) devices are expected to propel the growth of the 5G femtocell market forecast. However, regulatory challenges and spectrum availability, security & privacy concerns, and high initial investment costs hamper the growth of the 5G femtocell industry. Furthermore, the need for efficient network off-loading and congestion management as well as a rise in government initiatives to boost 5G infrastructure development are expected to provide lucrative opportunities for market growth. In addition, integration of 5G femtocell with smart city initiatives and growing collaboration between telecom operators and enterprises for customized solutions are anticipated to create numerous opportunities for the 5G femtocell market growth in the coming years.

Key Takeaways

- Depending on deployment, the standalone segment is accounted for the largest 5G femtocell market share in 2023.

- Based on application, the indoor segment is accounted for the largest market share in 2023.

- On the basis of end user, the commercial segment is accounted for the largest market share in 2023.

- Region wise, Asia-Pacific generated the highest revenue in 2023.

Top Impacting Factors

Increase in deployment of 5G networks and IoT devices

The Increase in deployment of 5G networks and the proliferation of IoT devices serve as the notable drivers of the 5G femtocell market. As the demand for high-pace, low-latency connectivity continues to develop exponentially, mainly in indoor environments, 5G networks represent the subsequent evolution in telecommunications technology. However, traditional macrocell towers often struggle to penetrate buildings effectively, leading to coverage gaps and degraded network performance indoors. With the deployment of 5G femtocell, telecom vendors can efficiently deal with these indoor coverage challenges by extending the attain of 5G networks into houses, workplaces, and other indoor spaces. By leveraging present internet connections, femtocell offers customers with dependable, high-speed connectivity for a wide range of applications, such as streaming, gaming, video conferencing, and IoT devices.

Moreover, the proliferation of IoT devices emphasizes the significance of enhanced indoor coverage and potential. As rising of number connected devices, spanning from smart home appliances to industrial sensors, the requirement for sturdy and reliable connectivity solutions inside indoor environments is expected to grow simultaneously, thereby augmenting the 5G femtocell industry. Furthermore, 5G femtocell plays a vital role in meeting the demand by providing uninterrupted connectivity for IoT devices, facilitating real-time data transmission, and unleashing the full potential of IoT applications. Therefore, these factors are collectively driving the adoption of 5G femtocell and unlocking the new opportunities for innovation and growth in the industry.

Development of open RAN architectures for interoperability and flexibility

The development of open RAN architectures acts as an important trend of the industry, due to its emphasis on interoperability and flexibility. Open RAN architectures aim to analyze network elements, allowing for interoperability between hardware and software components from different vendors. This approach enables femtocell manufacturers to develop solutions that seamlessly integrate with diverse network environments, encouraging interoperability between femtocells and macrocell. In addition, open RAN architectures provide flexibility in network deployment and management, enabling vendors to customize and optimize their networks according to specific requirements. By embracing open RAN principles, the 5G femtocell industry can accelerate innovation, reduce deployment costs, and enhance the scalability and efficiency of femtocell deployments within 5G networks.

The global 5G femtocell market is segmented into deployment, application, end user, network type, and region. By deployment, the market is bifurcated into standalone and non-standalone. Depending on application, it is categorized into indoor and outdoor. On the basis of end user, it is segregated into residential, commercial, and public places. By network type, the market is bifurcated into public and private. Region wise, it is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Depending on application, the global 5G femtocell market size was dominated by the indoor segment in 2023 and is expected to continue this trend in the upcoming years, owing to advances in technologies enabling 5G femtocell to transform indoor coverage. However, the outdoor segment is expected to witness highest growth, as outdoor femtocell supports emerging applications such as smart cities, autonomous vehicles, and industrial IoT by providing reliable connectivity in outdoor environments.

Region wise, Asia-Pacific dominated the 5G femtocell market share in 2023, due to increase in investments in advanced technologies such as AI and IoT devices to improve businesses and customer experiences in the region. However, LAMEA is expected to exhibit the highest growth during the forecast period. This is attributed to the increase in penetration of digitalization and higher adoption of connected technology.

Competition Analysis

The key players operating in the global 5G femtocell market are Telefonaktiebolaget LM Ericsson, Fujitsu Limited, Aricent, Inc., Nokia Corporation, Cisco System Inc., Huawei Technologies Co. Ltd., Samsung Electronics Co. Ltd., Vodafone Group Plc, Corning Incorporated, and ZTE Corporation. These players have adopted various development strategies such as business expansion, new product launches, and partnerships to strengthen their foothold in the competitive market. For instance, in February 2023, Cisco partnered with T-Mobile to launch businesses Cisco Meraki's first-ever 5G cellular gateways for fixed wireless access (FWA), the MG51 and MG51E. With the help of this solution, businesses of all sizes will be able to differentiate experiences for their customers using simplified, scalable, and reliable network managed services and the cloud-first Cisco Meraki platform.

Key Developments in the 5G femtocell Industry

In February 2024, ZTE Corporation, a global leading provider of information and communication technology solutions, and U Mobile, the award-winning mobile and digital services provider signed a memorandum of understanding (MOU) to enhance collaboration in 5G and 5G Advanced technology, containerization, and autonomous network initiatives, as well as 5G adoption for businesses.

In October 2021, Nokia and TPG Telecom launched the first live 5G femtocell in Asia-Pacific. The solution enables operators to offer their consumers enhanced indoor 5G coverage via a dedicated femtocell by utilizing Nokia's unique modular 4G/5G Smart Node. The Nokia Smart Node is a specialized indoor solution with exceptional coverage and capacity that can be readily expanded from one to several units.

In May 2021, Nokia Corporation launched the Nokia Smart Node, a unique indoor mobile module solution that delivers high-quality 4G and 5G indoor mobile coverage for residential and small-medium enterprise use. The modular design can be deployed readily in any environment to support evolving consumer applications. It is future-proofed to support 4G and 5G networks when required and both non-stand-alone and stand-alone 5G applications through a software upgrade.

Key Benefits for Stakeholders

This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the 5G femtocell market analysis from 2023 to 2033 to identify the prevailing market opportunities.

The market research is offered along with information related to key drivers, restraints, and opportunities.

Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

In-depth analysis of the 5G femtocell market segmentation assists to determine the prevailing market opportunities.

Major countries in each region are mapped according to their revenue contribution to the global 5G femtocell market.

Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

The report includes the analysis of the regional as well as global 5G femtocell market trends, key players, market segments, application areas, and market growth strategies.

5G Femtocell Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 9.3 billion |

| Growth Rate | CAGR of 23.6% |

| Forecast period | 2023 - 2033 |

| Report Pages | 281 |

| By Deployment |

|

| By Application |

|

| By End User |

|

| By Network Type |

|

| By Region |

|

| Key Market Players | Samsung Electronics Co Ltd., Aricent Inc., Telefonaktiebolaget LM Ericsson, Cisco System Inc., Vodafone Group Plc, Fujitsu Limited, Nokia Corporation, Corning Incorporated, ZTE Corporation, Huawei Technologies Co. Ltd. |

Analyst Review

The 5G femtocell is instrumental in meeting the escalating demand for high-speed, low-latency connectivity in indoor environments. With the proliferation of bandwidth-intensive applications, IoT devices, and remote work scenarios, consumers and enterprises alike expect reliable connectivity that transcends traditional coverage limitations. By strategically deploying femtocells, businesses can ensure that their networks deliver consistent performance and meet the evolving connectivity needs of their customers. Moreover, major players understand the transformative potential of femtocells in unlocking new revenue streams and business opportunities.

By leveraging femtocell technology, telecom operators can offer value-added services such as premium indoor coverage packages, IoT connectivity solutions, and enterprise-grade networking services. This not only enhances customer satisfaction but also drives revenue growth and strengthens competitive positioning in the market. In addition, businesses recognize the importance of femtocells in optimizing network efficiency and reducing operational costs. By offloading traffic from macrocell towers to femtocells, telecom operators can alleviate network congestion, improve spectral efficiency, and enhance overall network performance.

Furthermore, prominent market players are exploring new technologies and applications to meet the increasing customer demands. Product launches, collaborations, and acquisitions are expected to enable them to expand their product portfolios and penetrate different regions. For instance, in October 2023, Ericsson launched a new software toolkit to strengthen 5G standalone network capabilities and enable premium services with differentiated connectivity. The portfolio enhancement comes as the growth of new use cases and rising mobile user expectations on the quality of 5G experience are putting greater demands on network capacity and performance. Such emerging enhancements are anticipated to create notable opportunities for the 5G femtocell market expansion during the forecast period.

The global 5g femtocell market was valued at USD 1.2 billion in 2023, and is projected to reach USD 9.3 billion by 2033

The 5g femtocell market is projected to grow at a compound annual growth rate of 23.6% from 2024 to 2033 reach USD 9.3 billion by 2033

The key players operating in the global 5G femtocell market are Telefonaktiebolaget LM Ericsson, Fujitsu Limited, Aricent, Inc., Nokia Corporation, Cisco System Inc., Huawei Technologies Co. Ltd., Samsung Electronics Co. Ltd., Vodafone Group Plc, Corning Incorporated, and ZTE Corporation.

Asia-Pacific dominated the 5G femtocell market

The Increase in deployment of 5G networks and the proliferation of IoT devices serve as the notable drivers of the 5G femtocell market.

Loading Table Of Content...

Loading Research Methodology...