5G in Defense Market Summary

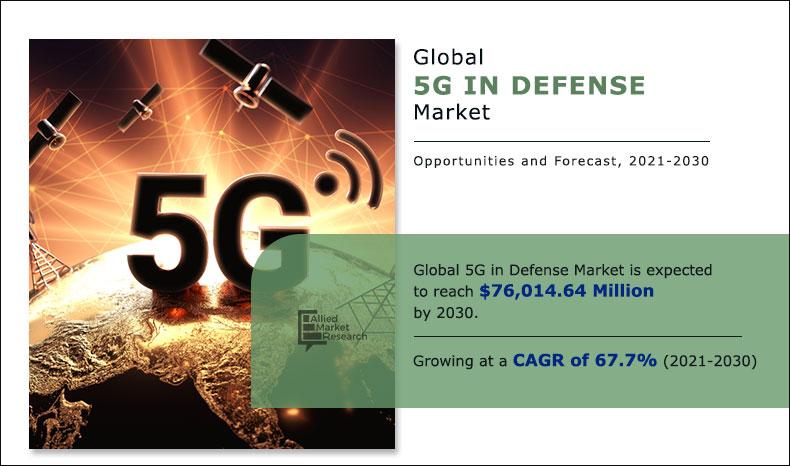

The global 5G in defense market size was valued $551 million in 2020 and is projected to reach $76,014.6 million in 2030, registering a CAGR of 67.7% from 2021 to 2030.

Key Market Trends and Insights

Region wise, Asia Pacific generated the highest revenue in 2020.

The global 5G in defense market share was dominated by the fog computing segment in 2020 and is expected to maintain its dominance in the upcoming years

The millimeter wave chipset segment is expected to witness the highest growth during the forecast

Market Size & Forecast

- 2020 Market Size: USD 551 Million

- 2030 Projected Market Size: USD 76,014.6 Million

- Compound Annual Growth Rate (CAGR) (2021-2030): 67.7%

- Asia Pacific: Generated the highest revenue in 2020

Market Dynamics

5G or 5th generation mobile network has the capability to connect practically everyone and everything together comprising objects, devices, and machines. The deployment of 5G technology is gradually increasing across the globe. 5G will considerably increase the speed of data transfer and improve bandwidth over 4th generation or 4G technology, in turn supporting new military and commercial uses. The use of impressively fast 5G networks for the defense and security purposes could advance intelligence, surveillance, and reconnaissance (ISR) systems and processing; modernize logistics operations for improved efficiency, and develop new methods of command and control (C2); among others. Military equipment and technology companies will make use of 5G software and hardware for present and future systems, benefiting from valuable properties as quick response times and wide bandwidths that will soon make extremely fast transmission and reception of images demonstrating real-time battlefield scenarios possible.

Rise in investments by countries in 5G technologies is expected to propel the global 5G in defense market growth during the forecast period. For instance, in October 2020, the U.S. Department of Defense announced $600 million for 5G test bed and experimentation undertakings at 5 U.S. military test locations. Over the years, the work will be expanded across several additional military bases.

By Communication Infrastructure

Radio Access Network is projected as the most lucrative segment

Increase in autonomous defense vehicles, drones, and robots

Autonomous vehicles, drones, and robots play a vital role in the defense industry. These are fully autonomous tools that employ telecommunication technology such as the 5G network, at the disposal of defense agencies to provide services in real time at dangerous, inconvenient, and impossible areas of operation namely remote surveillance for enemy infantry. Various countries across the globe have focused on the development of unmanned systems to be utilized in public and national safety applications. Multiple governments from developed and emerging nations such as the U.S., Russia, China, India, and others have invested billions of dollars toward autonomous defense projects. For instance, Europe launched a defense research and development program of €7.9 billion in January 2021 toward financing defense R&D projects.

The adoption of autonomous technologies helps in the reduction of operational costs and increases efficiency significantly. For instance, during the operation of a naval destroyer for a single day $700,000 are spent by the U.S. navy whereas in the case of an autonomous ship's operation costs would come down to $15,000 to $20,000 per day. Moreover, for increased efficiency; several nations around the world are deploying the use of 5G in the operation of autonomous defense vehicles, robots, and drones. For instance, U.S. ignite launched a technology pilot program in January 2021 for the 5G Living Lab at Marine Corps Air Station (MCAS) Miramar situated in San Diego. Moreover, several pilot projects aimed at the utilization of 5G in autonomous defense vehicles, drones, and robots are underway globally.

By Core Network Technology

Fog Computing is projected as the most lucrative segment

Rise in adoption of autonomous technology to improve the defense capabilities of the nation globally is anticipated to propel the growth of the global 5G in defense market during the forecast period.

Rise in support of government toward the development of 5G

5G helps governments across the world to provide secure, reliable, and agile safety for its civilian and property. These features motivate the governments to increase their support toward the development of 5G technology. For instance, National Communications Commission (NCC), Taiwan, announced an allocation of US$ 948.5 million as a subsidy for the deployment of a 5G network from 2021 to 2025 to five telecom operators. This indicates the positive intention of governments toward incentivizing the evolution of 5G technologies.

By Network Type

Massive Machine Type Communications is projected as the most lucrative segment

Encouragement of such as government subsidies, R&D grants for 5G suppliers, and others provided from governments aid the telecommunications companies and other companies associated with the 5G industry in establishing high-cost infrastructures and services to support the growth of 5G. Several companies namely, L3Harris Technologies, Inc., Raytheon Technologies Corporation, Telefonaktiebolaget LM Ericsson, and Nokia Corporation benefit from this move. For instance, the U.S. Department of Defense (DoD) increased funding for 5G telecommunications to US$430 million from US$200 million toward accelerated 5G equipment development for military and civilian use. Moreover, countries such as Brazil, China, and India are planning to implement 5G in private as well as government applications.

Government support augments the growth of the 5G market. The rise in initiatives taken by the governments worldwide is expected to increase the growth of the 5G in defense market during the forecast period.

By Chipset

Millimeter Wave Chipset is projected as the most lucrative segments

Cybersecurity threats to 5G network

5G is a complex and onerous technology that involves the interconnection of multiple identical or non-identical devices. Different actors such as communication service providers (CSPs), network infrastructure providers, and virtual mobile network operators (VMNOs) are responsible for designing, implementing, and maintenance of 5G networks, synchronizing different priorities toward privacy and security policies among these actors will be a challenge. Moreover, 5G networks have smaller network coverage area when compared to 4G network consequently, increasing the need for multiple smaller antennas, which improve the precision of location tracking and can be further tapped and exploited from the antenna by the attacker to perform attacks such as a botnet, eavesdropping, worm propagation, network jamming, and personal attack.

5G network is ready to be rolled out at a mass scale by several nations, although, there have been various technological developments such as multiple-input multiple-output (MIMO), enhanced mobile broadband (eMBB), and others, several threats and vulnerabilities are yet to be resolved. For instance, researchers found that cybercriminals can attain device fingerprinting to carry out targeted attacks namely man-in-the-middle offenses in the 5G network. Moreover, the use of 5G in IoT devices reveals the exact identity of the device which further facilitates the conduction of a targeting attack. Furthermore, the use of technologies such as Software-Defined Networking (SDN) and Network Functions Virtualization (NFV) in the 5G network exposes more vulnerable points, which increase the chances of attacks such as Denial of Service (DoS) or Distributed Denial of Service (DDoS). For instance, Huawei Technologies Co., Ltd. was banned by the UK, the U.S., Australia, and New Zealand for the possibility of a state-sponsored hack via its 5G equipment. These hacks have an adverse effect on vital networks such as shutting down power stations, gaining access to confidential information, toolkit attacks, and others. These instances increase security concerns regarding military collaboration with 5G network vendors. These security and privacy concerns restrain the growth of the 5G in defense market.

By Platform

Airborne is projected as the most lucrative segment

Technological advancements in 5G network

The evolution of technologies around the world increased the demand for fast and reliable transmission networks to support the connection of advanced devices such as robots, sensors, drones, and autonomous vehicles used by defense agencies. 5G network offers real-time connectivity, machine-to-machine communication, high network speed, and other features, which aid in the interconnection of the smart devices used in surveillance and intelligence activities performed by the homeland security and intelligence agencies. Application of ultra-high frequency (UHF) radio spectrum with a frequency range from 300 MHz to 3 GHz in 5G network offers frequency hopping for tactical radios to be used by the military, federal agencies, and public agencies. For instance, modulation of sub 6GHz and mmWave 5G network can be used in border surveillance where high power and low-latency networks are required, and in smart bases where low power and long-range networks are required. Moreover, the development of small cell base stations helps in the expansion of wireless network capacity. Furthermore, the introduction of Network Functions Virtualization (NFV) at the edge and in the core of the 5G network, beam-forming antennas, 5G New Radio (NR) technology, Cellular Vehicle-To-Everything (C-V2X) technology and MIMO antennas aids in architecture development, increased coverage, enhanced communication and high throughput per connection in the radio network. 5G offers more immersive services such as mobile cloud, ultra-high-definition (UHD) 3D video, virtual reality, and augmented reality through the use of these technologies and hardware, which increases the productiveness of key defense mechanisms.

Technological advancements in the 5G network to increase the efficiency and productivity of military bases and defense operations offers lucrative market expansion opportunities for the 5G in defense market.

By Region

Asia Pacific would exhibit the highest CAGR of 72.2% during 2021-2030.

Segment Review

The 5G in defense market size is segmented into communication infrastructure, core network technology, network type, chipset, platform, and region. Based on communication infrastructure, the market is divided into small cell, macro cell, and radio access network (RAN). On the basis of core network technology, the market is categorized into software defined networking (SDN), fog computing (FC), mobile edge computing (MEC), and network functions virtualization (NFV). Depending on network type, it is fragmented into enhanced mobile broadband (eMBB), ultra-reliable low-latency communication (URLLC), and massive machine type communications (mMTC). On the basis of chipset, the market is classified into application specific integrated circuit (ASIC) chipset, Radio-Frequency Integrated Circuit (RFIC) chipset, and millimeter wave (mmWave) Chipset. Based on platform, the market is distributed into land, naval, and airborne. Region wise, the 5G in defense industry is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Competitive Landscape

Key players operating in the global 5G in defense market include Telefonaktiebolaget LM Ericsson, Huawei Investment & Holding Co., Ltd, Nokia Corporation, Samsung Electronics Co., Ltd, NEC Corporation, Thales Group, L3Harris Technologies, Inc., Raytheon Technologies Corporation, Ligado Networks, and Wind River Systems, Inc.

COVID-19 Impact Analysis

- The COVID impact on the 5G in defense market share is unpredictable and it is expected to remain in force till the second quarter of 2021.

- The COVID-19 outbreak forced governments across the globe to divert their investments and other activities from 5G technologies to strengthen healthcare services for managing the spread of the virus. This led to significant delays in the deployment of 5G services across several nations.

- Moreover, nationwide lockdowns disrupted supply-chain as several 5G component manufacturers had to partially or fully shut down their operations.

- The adverse impacts of the COVID-19 pandemic have resulted in delays in activities and initiatives regarding development of innovative 5G technologies.

Key Benefits For Stakeholders

- This study presents the analytical depiction of the global 5G in defense market analysis along with the 5G in defense market trends and future estimations to depict imminent investment pockets.

- The overall 5G in defense market opportunity is determined by understanding profitable trends to gain a stronger foothold.

- The report presents information related to the 5G in defense market segmentation, key drivers, restraints, and opportunities of the global market with a detailed impact analysis.

- The current 5G in defense market forecast is quantitatively analyzed from 2020 to 2030 to benchmark the financial competency.

- Porter’s five forces analysis illustrates the potency of the buyers and suppliers in the 5G in defense industry.

5G in Defense Market Report Highlights

| Aspects | Details |

| By Communication Infrastructure |

|

| By Core Network Technology |

|

| By Network Type |

|

| By Chipset |

|

| By Platform |

|

| By Region |

|

| Key Market Players | Telefonaktiebolaget LM Ericsson, Thales Group, NEC Corporation, Samsung Electronics Co., Ltd, Wind River Systems, Inc., Huawei Investment & Holding Co., Ltd, Nokia Corporation, Ligado Networks, L3Harris Technologies, Inc., Raytheon Technologies Corporation |

Analyst Review

The global 5G in defense market is expected to witness significant growth due to rise in demand for 5G services to modernize military operations across the globe with superior interconnection of devices, machines, and vehicles.

Increase in number of autonomous defense vehicles, drones, and robots; rise in support of government toward development of 5G, and increase in demand for surveillance activities are expected to drive the global 5G in defense market growth during the forecast period. However, cybersecurity threats to 5G network and high infrastructure costs for the deployment of 5G are anticipated to hamper the growth of the market during the forecast period. Moreover, technological advancements in 5G network and upgradation of military bases are expected to offer lucrative opportunities for the market in future.

Superior communications are a crucial component of any military operation and connections must be unfailing, protected, and without interruptions. Military authorities expect that the 5G technologies will play a vital role in the improved usage of hypersonic missiles, comprising nuclear warheads, which move at a speed higher than Mach 5. With the purpose of guiding missiles on changing paths, altering course in milliseconds to avoid interceptor missiles, it is essential to collect, process, and communicate massive amounts of data in a very short duration.

5G technology will also play a critical role in improving battlefield networks. 5G has the ability to connect lots of transceivers at the same time in a defined region. It will help the defense personnel, divisions, and individuals to exchange photos, maps, and other data about the operation proceeding almost in real time. The millimeter-wave (mm-wave) frequency range provides superior communication speeds to enhance several military applications, for instance, real-time intelligence, control of swarming unmanned aerial vehicles (UAVs), dynamic RF spectrum use, distributed command, and control, and smart warehousing and logistics.

Increase in technological advancements regarding the development of superior 5G software and hardware for military needs is anticipated to bolster the demand for 5G in defense applications over the years. Moreover, rise in initiatives by nations across the globe to deploy 5G technologies in coming years is anticipated to offer lucrative opportunities for 5G in defense market during the forecast period.

Among the analyzed regions, Asia-Pacific is the highest revenue contributor, followed by North America, Europe, and LAMEA. On the basis of forecast analysis, Asia-Pacific is expected to maintain its lead during the forecast period, owing to increase in funding for the deployment of 5G technology in the region and rise in demand for faster data speeds in big markets such as China, Japan, South Korea, and India.

The global 5G in defense market size was valued at USD 551 million in 2020, and is projected to reach USD 76,014.64 million by 2030.

The global 5G in defense market is projected to grow at a compound annual growth rate of 67.7% from 2021-2030 to reach USD 76,014.64 million by 2030.

Key players operating in the global 5G in Defense market include Telefonaktiebolaget LM Ericsson, Huawei Investment & Holding Co., Ltd, Nokia Corporation, Samsung Electronics Co., Ltd, NEC Corporation, Thales Group, L3Harris Technologies, Inc., Raytheon Technologies Corporation, Ligado Networks, and Wind River Systems, Inc.

Asia Pacific region accounted for the highest revenue contributor in 2020 and is expected to see lucrative business opportunities during the forecast period.

Increase in autonomous defense vehicles, drones, and robots, Rise in support of government toward the development of 5G, Cybersecurity threats to 5G network, Technological advancements in 5G network majorly contribute toward the growth of the market.

Loading Table Of Content...