Direct Primary Care Market Research, 2032

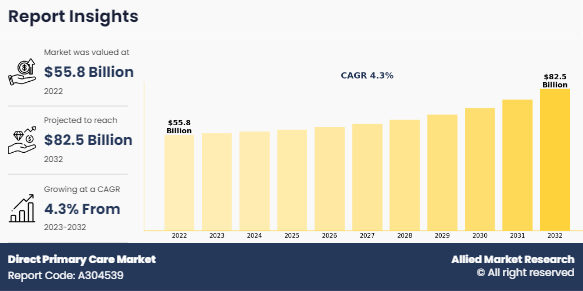

The global direct primary care market size was valued at $55.8 billion in 2022, and is projected to reach $82.5 billion by 2032, growing at a CAGR of 4.3% from 2023 to 2032. Direct primary care is a revenue model that is capable of boosting patient access and availability to healthcare services while also stabilizing medical practice revenue. In this arrangement, medical providers deal directly with patients, bypassing third parties and insurance programs. The direct primary care model often consists of regular payments (monthly, quarterly, and annually.) in exchange for a wide range of primary care services. The strategy is especially well-suited for those who lack insurance or have high-deductible catastrophic insurance policies.

Market Dynamics

DPC physicians prioritize a holistic approach, taking into account the patient's general health, lifestyle, and unique circumstances. This strategy goes beyond treating symptoms to address the underlying causes of health problems. DPC doctors strive to deliver comprehensive and integrated treatment by considering a patient's physical, mental, and emotional well-being. Holistic care frequently places a major emphasis on preventative measures.

DPC providers interact with patients to identify risk factors, encourage healthy lifestyle choices, and prevent the onset of chronic illnesses. This preventive focus aligns with the broader healthcare trend of shifting from reactive to proactive care. Physicians spend more time with patients, actively listening to their concerns, understanding their values and preferences, and involving them in decision-making processes. This patient-centric approach fosters trust and collaboration between the provider and the patient. Thus, all these factors are anticipated to drive the direct primary care market growth.

DPC covers only essential primary care services. Patients may still buy extra protections or pay out of pocket for specialty care, hospitalizations, and other services not included within the DPC participation. DPC is not a substitute for comprehensive well-being protections. Patients may still require protections for major therapeutic costs, surgeries, and crises. Although DPC is regularly more reasonable for scheduled essential care services, the month-to-month enrolment expenses may be challenging for a few individuals or families to afford. This will restrain consumers to get DPC for certain socioeconomic groups.

In addition, regulatory and legal factors can pose challenges for DPC practices. These may include state laws governing medical licensure, scope of practice, and telemedicine regulations, as well as federal regulations related to Medicare reimbursement and compliance with healthcare privacy laws such as the Health Insurance Portability and Accountability Act (HIPAA). All these factors are anticipated to restrain the direct primary care market share growth.

Direct primary care involves telehealth services, enabling patients to speak with vendors simply for consultations, follow-ups, and minor health concerns. Furthermore, with DPC, companies can schedule cell visits or house calls as needed, reducing time spent on administrative tasks and allowing for a greater focus on patient care. By opting out of insurance plan billing and decreasing paperwork, providers can enhance efficiency, streamline operations, and provide a greater customized experience.

DPC vendors prioritize preventive care and focal point on constructing sturdy provider–patient relationships. With longer appointment times, vendors can perform thorough check-ups, offer comprehensive health screenings, and grant personalized health guidance, emphasizing ordinary well-being. These factors are anticipated drive the direct primary care market size in the upcoming years.

The key players profiled in direct primary care industry report include One Medical, Oak Street Health, Paladina Health, Forward Health, Crossover Health, EverMed, Plum Health, Nextera Healthcare, Boston Direct Health, and PeakMed. Investment and agreement are common strategies adopted by major market players. For instance, in July 2022, MDVIP expanded its National Primary Care Network with the addition of Richard M. Del Sesto, a board-certified internist in Rhode Island.

The direct primary care market is segmented into type and region. By type, the market is segregated into clinical services, laboratory services, consultative services, and others. Region wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

By Type

The clinical services segment dominated the direct primary care market share in 2022. Clinical offerings play a quintessential position in the DPC market, as they constitute the core healthcare services provided without delay to patients. Regular physical examinations and preventive care are foundational in DPC. This consists of fitness screenings, vaccinations, and way of life counseling to stop the onset or progression of illnesses. DPC medical doctors regularly focal point on managing continual stipulations such as diabetes, hypertension, and asthma. Regular monitoring and personalized care plans help sufferers higher manage and cope with their persistent health issues. DPC practices furnish instant interest and care for acute illnesses, minor injuries, and infections. DPC can further offer primary diagnostic checks such as blood tests, urinalysis, and different point-of-care diagnostics. These offerings assist in early detection and monitoring of health conditions.

By Region

North America dominated the global direct primary care market in 2022The increasing prevalence of chronic diseases in the U.S. is driving the demand for primary care services. The National Association of Chronic Disease Directors estimates that by 2022 almost 60% of adults in the U.S. would be suffering from at least one chronic disease. Furthermore, approximately 40% of these adults have multiple chronic diseases (MCC), increasing their risk to new ones as they age. The increased burden of chronic illnesses among individuals is a crucial factor driving the growth of the direct primary care industry.

In addition, more primary care physicians were transitioning to DPC practices, attracted by the promise of a more direct doctor–patient relationship and reduced administrative burdens associated with insurance billing. Many DPC practices were incorporating telemedicine into their service offerings, allowing patients to access care remotely when appropriate. This trend was accelerated by the COVID-19 pandemic, which highlighted the importance of virtual healthcare solutions.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the direct primary care market analysis from 2022 to 2032 to identify the prevailing direct primary care market opportunity.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the direct primary care market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global direct primary care market trends, key players, market segments, application areas, and market growth strategies.

- Depending on type, the clinical services segment emerged as the global leader in 2022 and is anticipated to be the fastest growing sub-segment during the direct primary care market forecast period.

Direct Primary Care Market Report Highlights

| Aspects | Details |

| Market Size By 2032 | USD 82.5 billion |

| Growth Rate | CAGR of 4.3% |

| Forecast period | 2022 - 2032 |

| Report Pages | 320 |

| By Type |

|

| By Region |

|

| Key Market Players | Forward Health, Paladina Health, Oak Street Health, One Medical, Nextera Healthcare, Plum Health, PeakMed, Boston Direct Health, EverMed, Crossover Health |

Direct primary care emphasizes a patient-centric model, focusing on personalized and preventive care. This approach appeals to individuals seeking more direct and unhurried interactions with healthcare providers. DPC often offers a subscription-based or fee-for-service model, making healthcare costs more transparent and predictable for patients. This can be particularly appealing for individuals without comprehensive health insurance coverage.

The major growth strategies adopted by direct primary care market players are investment and agreement.

Asia-Pacific is projected to provide more business opportunities for the global direct primary care market in the future.

One Medical, Oak Street Health, Paladina Health, Forward Health, Crossover Health, EverMed, Plum Health, Nextera Healthcare, Boston Direct Health, and PeakMed are the major players in the direct primary care market.

The clinical services segment acquired the maximum share of the global direct primary care market in 2022.

The potential customers of the DPC industry include a diverse range of individuals and organizations seeking alternatives to traditional fee-for-service healthcare.

The report provides an extensive qualitative and quantitative analysis of the current trends and future estimations of the global direct primary care market from 2022 to 2032 to determine the prevailing opportunities.

The incorporation of telehealth services within DPC practices is likely to increase, providing patients with remote access to healthcare professionals and enhancing convenience. DPC providers may increasingly leverage electronic health records (EHRs) and other health information technologies to streamline operations and improve patient care.

Loading Table Of Content...

Loading Research Methodology...