Market")

Europe In Vitro Fertilization (IVF) Market Overview:

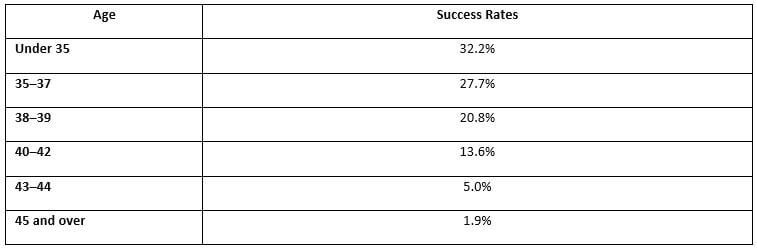

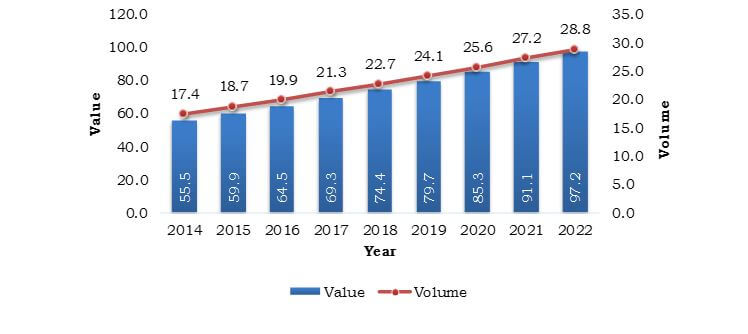

The European IVF Market was valued at $3,054 million in 2015 and is estimated to reach $4,447 million by 2022, growing at a CAGR of 5.4% during the analysis period. In vitro fertilization is a type of assisted reproductive technology-based fertility treatment across the clinical industry. Delayed pregnancy in women is a major factor that drives the IVF market, as the chances of conceiving lowers with age. The success rate of getting pregnant with IVF technique is higher in the age group of 35–39 years.

The major factors that limit this market growth are cost incurred and stringent government regulations. A patient may need to undergo several cycles of pregnancy owing to the lower success rate of IVF procedures, thereby adding to the overall cost. The average cost of this procedure is approximately $10,000–$20,000, which often acts as a major limitation, to the adoption of the technique. In addition, ethical considerations and lack of reimbursements are other challenges that impede the market growth. The companies profiled in this report include Thermo Fisher Scientific, Inc., DRK Kliniken Berlin, Sun Pharmaceutical Industries Ltd., Cadila Healthcare Ltd., LG Life Sciences, and EMD Serono Inc.

The growing trends of delayed pregnancy have steadily increased across Europe and other countries. In older women, eggs produced by the reproductive system are less efficient for the process of fertilization with the male spermatozoa, resulting in risk of genetic disorders. According to Centers for Disease Control and Prevention (CDC), the rate of fertilization in the age group of 35–39 years through IVF is considerably high.

IVF techniques play a significant role in addressing infertility. The success rates in Denmark range from 26% to 29% for patients in the age group of 25–37 years. The pregnancy rate is 12–16% for the age group of 37-45 years; however, clinicians claim that there are more chances of miscarriage in this age group, resulting in birth rate of about 8–10%. A single standard IVF cycle in Denmark costs approximately $4,800, which is less than that in the rest of European countries. However, these costs are higher as compared to that in Russia and Spain.

The key companies offering these products includes include Thermo Fisher Scientific, Inc., DRK Kliniken Berlin, Sun Pharmaceutical Industries Ltd., Cadila Healthcare Ltd., LG Life Sciences, and EMD Serono Inc

Key Benefits for Stakeholders:

- This report provides an in-depth analysis of the European IVF market across eight major countries along with cross-sectional analysis of the total number of IVF cycles performed and the total revenue generated during the forecast period.

- It includes the strategies adopted by various IVF clinics and hospitals across major countries to capitalize on the latent opportunities in the market.

- The projections are made by analyzing the current market trends and highlighting the market potential, in terms of value and volume, from 2015 to 2022.

- Extensive analysis of the market is conducted by following the key product positioning and monitoring the top contenders.

Europe In Vitro Fertilization (IVF) Market Key Segments:

By End Users (Value and Volume)

- Fertility Clinics

- Hospitals

- Surgical Centers

- Clinical Research Institutes

By Cycle Type (Value and Volume)

- Fresh Cycle (Non-Donor)

- Thawed IVF Cycle (Non-Donor)

- Donor Egg IVF Cycle

By Cycle Type Country Level Analysis (Value and Volume)

- Germany

- France

- UK

- Italy

- Spain

- Denmark

- Russia

- Rest of Europe

Analyst Review

The emerging trend of delayed pregnancies and increasing average age of parenthood over the last decade are major factors that drive the growth of the IVF market. France has witnessed a rise in trend in same-sex couples seeking parenthood. In addition, polygamy and polyandry have also increased, though to a lesser extent, increasing the demand for alternative reproductive treatments. Countries such as UK have recently accepted three-parent IVF methods, commonly banned in other countries worldwide. This method is expected to boost the growth of UK IVF market owing to its inherent benefits of avoiding gene-linked mitochondrial DNA diseases in newborns.

The growth in government interventions and support, especially in UK where lower fertility, aging population, and lack of workforce have triggered severe implications, is further expected to boost the market growth. Government support and regulations (such as HFEA act and guidelines), favorable policies such as three-parent IVF, and availability of reimbursements are expected to drive the UK IVF market growth at a CAGR higher than rest of the European countries.

Loading Table Of Content...