Industrial Emission Control Systems Market Overview:

Global Industrial Emission Control Systems Market is expected to garner $21,133 million by 2022. Electrostatic precipitators (ESP) are estimated to dominate the market from 2015-2022. Industrial emission control systems monitor and reduce harmful products that are released by combustion and other emission processes, which cause environmental pollution.

Industrial segments, such as power generation, cement, mining & metals, chemical industries, and others, use these equipment to convert hazardous air contaminants such as unburned hydrocarbons, carbon monoxide, nitrogen oxides, and sulfur oxides into water vapor and carbon dioxide, which can be safely released into the atmosphere.

Regulatory agencies such as the Environmental Protection Association (EPA) have placed stringent limitations on acceptable emission levels that can be released into the atmosphere. Compliance with these regulations has led industries to increase their usage of emission control systems, while failure in adoption of these standards results in governments imposing substantial fines.The global market for industrial emission control systems is driven by the stringent environmental regulation standards, increase in industrialization, rise in usage of coal for power in developing countries, and growth in the cement sector. The market growth is restrained by the growth in use of alternate sources of energy such as solar, wind, and hydropower and decrease in coal power investments in developed economies.

Segment Overview:

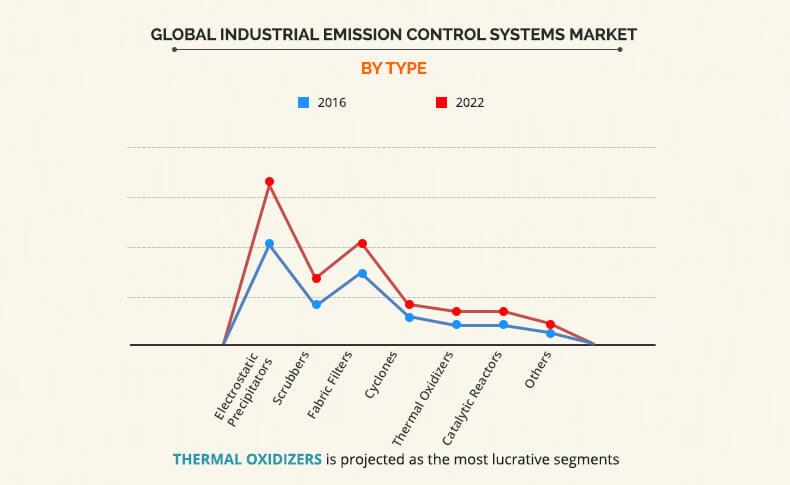

The global market for industrial emission control systems is segmented based on equipment type, emission source, and geography. The market is analyzed across four regions, namely, North America, Europe, Asia-Pacific, and LAMEA, along with their prominent countries. Based on equipment type, it is divided into electrostatic precipitators, fabric filters, scrubbers, cyclones, thermal oxidizers, and others. Electrostatic precipitators led the industrial emission control systems market. Electrostatic precipitators are capable of operating at over 99% efficiency levels and have applications in power plants, steel and paper mills, smelters, cement plants, and petroleum refineries. Thermal oxidizers equipment are estimated to grow at the highest CAGR during the forecast period owing to increase in applications in industries and their high efficiency levels.

Based on geography, Asia-Pacific is the major contributor to the revenue, followed by North America. Governments in these regions are in the process of implementing stringent regulations to effectively regulate emissions from the industrial segment. The emission control systems market in Asia-Pacific is also driven by the newly formulated mercury emission regulations.

Top Impacting Factors for Global Industrial Emission Control Systems Market

Stringent Emission Regulations:

The market for industrial emission control systems is affected by the emission regulations on the industries. Industrial sectors such as refineries, power plants, chemical & petrochemical sectors, mining & metals industries need to largely comply with these standards or potentially face substantial fines that will have a significant impact on their operations and profitability. The impact of these regulations is currently high, which is expected to continue to have severe impact on the adoption and relative growth of the market.

Cement Industry Growth: Cement and lime producing industries are key end-user segments for industrial emission control systems. These industries generate the most harmful emissions such as carbon dioxide, particulate, NOx, and SOx, which have adverse impact on the environment causing occupational hazards, and adverse effects on crops, orchids, and building. Cement industry is also highly regulated with respect to air pollution standards and release of harmful emissions. The growth in the cement industry due to infrastructure developing increases the potential growth for industrial emission control systems.

Industrial Growth in Emerging Countries:

The industrial growth in emerging countries is driven by China and India. Globalization has led to various manufacturing companies from developed countries to migrate to these low-cost countries. This establishment of local manufacturing companies increases the demand for emission control systems. With the rise in industrialization, environmental regulations in emerging regions are also being directed towards cleaner working environments and reduction in environmental emissions.

Major players operating in this market include General Electric Company, Mitsubishi Hitachi Power Systems Ltd., Fujian Longking Co., Ltd, Johnson Matthey PLC, Ducon Technologies Inc., Babcock & Wilcox Co., AMEC Foster Wheeler PLC, CECO Environmental Corp, Hamon Corporation, Thermax Ltd, and BASF SE.

Other players in the value chain include APC Technologies Inc., Auburn Systems LLC, Air Clear LLC, Epcon Industrial Systems, Anguil Environmental Systems Inc., PPC Air Pollution Control Systems, Advanced Cyclone Systems, Dust Control Systems Ltd, Pennar Industries, Marsulex Environmental Technologies, and United Air Specialists Inc.

Key Benefits

- The study provides an in-depth analysis of the global industrial emission control systems market, with current trends and future estimations to elucidate the imminent investment pockets.

- Information regarding key drivers, restraints, and opportunities with a detailed impact analysis is explained.

- Porter’s Five Forces Model illustrates competitiveness of the market by analyzing various parameters such as threat of new entrants, threat of substitutes, strength of the buyers, and strength of the suppliers.

- Value chain analysis signifies the key intermediaries involved and elaborates their roles and value additions at every stage.

- Quantitative analysis of the market from 2014 to 2022 is provided to elaborate the market potential.

Industrial Emission Control Systems Market Report Highlights

| Aspects | Details |

| By EQUIPMENT TYPE |

|

| By EMISSION SOURCE |

|

| By Region |

|

| Key Market Players | CECO Environmental, Thermax Ltd., Amec Foster Wheeler, BASF SE, General Electric Company (GE), Fujian Longking Co., Ltd, DUSTEX CORPORATION, Hamon Group, Ducon Technologies Inc., BABCOCK & WILCOX ENTERPRISES, Mitsubishi Hitachi Power Systems Environmental Solutions Ltd., Johnson Matthey PLC, GEA Group AG |

Analyst Review

The global market for industrial emission control systems is estimated to witness significant growth over the forecast period. This market is driven by the change in regulatory environment globally. Industries worldwide need to comply with various international, federal, state, and local government legislations, failing which they would have to potentially face large fines or suspensions in operations. Governments have set out strong regulations for power plants and other emission sources to cut down their carbon and other harmful pollutant footprints. The enforcement of these regulations is expected to provide significant boost to the market.

The major emission sources for industrial air pollution are coal and thermal power plants. These plants emit a wide range of harmful air contaminants such as particulate matter, nitrogen oxides, sulfur oxides, mercury, and other contaminants, which can potentially cause lung failure and other diseases. To control these emissions, adoption of emission control equipment becomes a priority for industries. The power generation segment contributes to around 45.4% of the global market for industrial emission control systems. This segment utilizes advanced emission control technologies such as selective catalytic reactors (SCR), electrostatic precipitators, fabric filters, and other equipment to regulate the emissions from the industry.

The power generation segment is expected to witness substantial growth over the forecast period as its growth is driven by the installation of new coal-fired power plants in China, India, and other emerging regions. The market for this industry is also fueled by several retrofit programs that are being undertaken. The key factor restraining the market growth is increase in use of alternate sources for power generation such as wind, solar, and hydropower in developed regions such as North America and Europe.

Loading Table Of Content...