Point Of Care Hematology Diagnostics Market Research, 2030

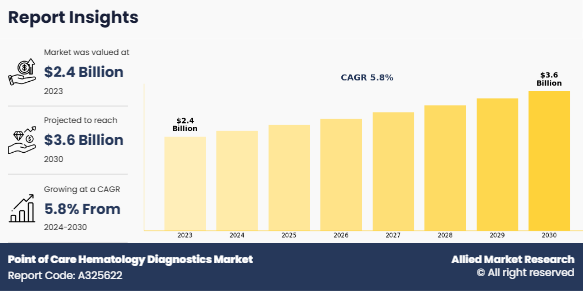

The global point of care hematology diagnostics market was valued at $2.4 billion in 2023, and is projected to reach $3.6 billion by 2030, growing at a CAGR of 5.8% from 2024 to 2030.The growth of the point of care hematology diagnostics market is driven by the rise in demand for rapid and accurate blood testing at the patient’s bedside, especially in emergency and remote settings. In addition, increase in prevalence of blood-related disorders and the need for immediate clinical decisions contribute to market growth.

Key Takeaways

- On the basis of test type, the complete blood count (CBC) segment dominated the global point of care hematology diagnostics market size in 2023. However, the coagulation testing segment is expected to register the highest CAGR during the point of care hematology diagnostics market forecast period.

- On the basis of mode of prescription, the prescription-based product segment dominated the global point of care hematology diagnostics market size in 2023. However, the OTC based product segment is anticipated to be the fastest-growing segment during the forecast period.

- On the basis of end user, the hospitals segment dominated the market in terms of revenue in 2023. However, the other segment is expected to register the highest CAGR during the forecast period.

- North America dominated the market in terms of revenue in 2023. However, Asia-Pacific is anticipated to grow at the highest CAGR during the forecast period.

Point-of-care hematology diagnostics refer to medical tests conducted near or at the site of patient care, specifically focused on analyzing components of human blood such as red blood cells, white blood cells, hemoglobin levels, and platelets. These diagnostic tools are designed to provide quick, accurate, and actionable results without the need to send samples to centralized laboratories. These devices help healthcare professionals make timely decisions for patient treatment and management by enabling immediate blood analysis, especially in critical care, outpatient, and rural settings. This approach improves efficiency, enhances patient outcomes, and reduces the turnaround time for blood-related diagnoses.

Market Dynamics

The point of care hematology diagnostics market growth is primarily driven by increase in demand for rapid, accurate, and accessible diagnostic solutions that are used at or near the site of patient care. One of the key growth drivers is the rise in prevalence of hematological disorders such as anemia, leukemia, and hemophilia, which require frequent blood monitoring and early detection for effective disease management. In addition, the aging global population and the surge in chronic disease cases have heightened the need for real-time diagnostic tools that offer quick results, enabling immediate clinical decisions, which is expected to drive the point-of-care (POC) hematology diagnostics market growth.

The shift toward decentralized healthcare systems, particularly in developing regions, propels the adoption of portable hematology analyzers that reduce dependency on centralized laboratory infrastructure. In addition, technological advancements in microfluidics, lab-on-a-chip platforms, and biosensor integration have significantly improved the accuracy, portability, and affordability of POC hematology devices. These innovations make diagnostics more accessible in remote, rural, and underserved areas, thus addressing the unmet needs of large patient populations.

Government initiatives promoting early diagnosis and the integration of POC devices in primary healthcare settings further boost market expansion. For instance, various national programs targeting maternal and child health include the deployment of POC devices for anemia screening, particularly in low- and middle-income countries.

Another contributing factor is the surge in preference for home-based and self-monitoring diagnostic kits, driven by increase in consumer awareness and the trend toward personalized healthcare. For instance, F. Hoffmann-la Roche Ltd provides the CoaguChek XS system which is ready for use anywhere at any time. Patients can use it for self-monitoring at home or while on vacation. Market players are also investing in product innovation, strategic partnerships, and regional expansions to strengthen their presence and cater to the diverse demands of global healthcare providers. The commercial availability of compact, user-friendly, and multi-parameter testing analyzers is facilitating the quick adoption of POC hematology diagnostics across emergency care, outpatient settings, and ambulatory surgical centers.

However, the high cost of advanced POC hematology devices limits adoption of POC testing products, especially in low-resource settings and smaller healthcare facilities. In addition, concerns regarding the accuracy and reliability of POC testing compared to centralized laboratory methods remain a barrier, as false results can lead to misdiagnosis or delayed treatment thereby restricting the point of care hematology diagnostics market growth.

On the other hand, advancements in microfluidics, and smartphone-integrated diagnostic technologies are paving the way for next-generation POC hematology devices that provide faster, more accurate, and multiplexed testing capabilities which provides a lucrative opportunity for the market growth.

Segmental Overview

The point of care hematology diagnostics industry is segmented on the basis of test type, mode of prescription, end user, and region. By test type, the market is classified into complete blood count (CBC), coagulation testing, hemoglobin testing & anemia diagnosis, and others. By mode of prescription, the market is segregated into Prescription based products and OTC based products. By end user, the market is fragmented into diagnostic centers, hospitals, blood banks & transfusion centers, and others.

Region-wise, the market is analyzed across North America (the U.S., Canada, and Mexico), Europe (Germany, France, the UK, Italy, Spain, Hungary, and rest of Europe), Asia-Pacific (China, Japan, Australia, India, South Korea, and rest of Asia-Pacific), and LAMEA (Brazil, Saudi Arabia, South Africa, and the rest of LAMEA).

By Test type

The complete blood count (CBC) segment dominated the point of care hematology diagnostics market share in 2023. This is attributed to its widespread use as a fundamental diagnostic tool for assessing overall health and detecting a wide range of conditions such as anemia, infections, blood cancers, and immune system disorders. Its routine application in primary care, emergency settings, and pre-surgical evaluations makes CBC one of the most ordered blood tests globally.

However, the coagulation testing segment is expected to register the highest CAGR during the forecast period. This is attributed to the increase in prevalence of blood clotting disorders such as deep vein thrombosis, pulmonary embolism, and hemophilia, along with the growing need for monitoring patients undergoing anticoagulant therapy.

By Mode of prescription

The prescription-based product segment dominated the point of care hematology diagnostics market share in 2023. This is attributed to its increased reliance on physician-recommended diagnostic tools for accurate and timely disease detection, particularly in clinical and hospital settings. Healthcare professionals continue to prefer prescription-based point-of-care hematology devices due to their higher reliability, regulatory approval, and integration with established treatment protocols.

However, the OTC based product segment is expected to register the highest CAGR during the forecast period. This is attributed to the growing consumer preference for convenient, accessible, and cost-effective diagnostic solutions that allow for self-monitoring without the need for a physician’s prescription. Rising health awareness, especially regarding early detection and preventive care, is driving demand for over-the-counter hematology test kits that can be used at home.

By End user

The hospitals segment dominated the market share in 2023. This is attributed to the high volume of patient admissions, the availability of advanced diagnostic infrastructure, and the need for rapid & accurate hematological assessments in emergency and inpatient care settings. However, the others segment is expected to register the highest CAGR during the forecast period. This is attributed to the increasing shift toward decentralized healthcare services and the growing demand for rapid diagnostics in non-traditional care settings.

By Region

The point of care hematology diagnostics market is analyzed across North America, Europe, Asia-Pacific, and LAMEA. North America region dominated the point of care hematology diagnostics market size in terms of revenue in 2023. This is attributed to the presence of well-established healthcare infrastructure, high adoption of advanced diagnostic technologies, and a growing focus on early disease detection and preventive care. The region benefits from a prevalence of chronic and hematological disorders, which drives consistent demand for point-of-care hematology diagnostics across hospitals, clinics, and home care settings. In addition, supportive government policies, favorable reimbursement frameworks, and increased healthcare spending contribute to widespread utilization of POC diagnostic tools.

However, the Asia-Pacific is expected to grow at the highest rate during the point of care hematology diagnostics market forecast period. This is attributed to the rapidly expanding healthcare infrastructure, increasing healthcare investments by governments and private sectors, and the rise in prevalence of hematological and chronic diseases across densely populated countries such as China and India. The growing awareness about early disease detection, coupled with a shift toward decentralized and affordable diagnostic solutions, is driving the adoption of point-of-care testing in rural and semi-urban areas. In addition, advancements in portable diagnostic technologies, along with the surge in mobile health initiatives and community-based healthcare programs, are expanding access to POC hematology diagnostics.

Competition Analysis

Key players such as EKF Diagnostics Holdings plc. and HORIBA, Ltd. have adopted acquisition, partnership, and agreement as key developmental strategies to improve the product portfolio of the point of care hematology diagnostics market. For instance, in Novemeber 2021, EKF Diagnostics acquired ADL Health, a Texas-based molecular diagnostic testing laboratory, to expand its capabilities in infectious disease testing. This strategic move enhances its portfolio in point-of-care and laboratory-based diagnostics.

Recent Developments in Point of Care Hematology Diagnostics Industry

- In August 2023, PixCell Medical announced that its HemoScreen analyzer has received FDA clearance for direct capillary sampling using a finger-prick of blood. This advancement enables faster, simpler, and less invasive CBC testing at the point of care. The update enhances accessibility and supports rapid clinical decisions in non-laboratory settings.

- In September 2022, PixCell Medical, innovator of rapid hematology testing solutions at the point-of-care, announced that it has signed an exclusive distribution agreement with Katalyst Diagnostics, a new division of Katalyst Laboratories, to distribute HemoScreen across the United Kingdom and Ireland. HemoScreen is the only 5-part differential Complete Blood Count (CBC) analyzer that is FDA-cleared, CE-marked and TGA-approved for point-of-care (POC) use.

- In March 2021, HORIBA announced the acquisition of MedTest Dx and Pointe Scientific, two U.S.-based companies specializing in clinical chemistry diagnostics. This strategic move expanded HORIBA's capabilities in laboratory-based chemistry testing, complementing its existing hematology and point-of-care portfolios. The acquisition aims to strengthen HORIBA's global presence and enhance its integrated diagnostic offerings across both centralized and decentralized healthcare environments.

- In February 2021, HORIBA Medical obtained CE Mark certification for its next-generation Microsemi CRP LC-767G point-of-care hematology analyzer. This advanced device offers simultaneous measurement of complete blood count (CBC) and C-reactive protein (CRP), providing rapid results in under 4 minutes. The certification affirms the analyzer's compliance with safety and performance standards, supporting its deployment in near-patient and decentralized care settings across Europe.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the point of care hematology diagnostics market analysis from 2023 to 2030 to identify the prevailing point of care hematology diagnostics market opportunity.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the point of care hematology diagnostics market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global point of care hematology diagnostics market trends, key players, market segments, application areas, and market growth strategies.

Point of Care Hematology Diagnostics Market Report Highlights

| Aspects | Details |

| Market Size By 2030 | USD 3.6 billion |

| Growth Rate | CAGR of 5.8% |

| Forecast period | 2023 - 2030 |

| Report Pages | 340 |

| By Test Type |

|

| By End User |

|

| By Mode of Prescription |

|

| By Region |

|

| Key Market Players | SoulBrain Holdings Co Ltd, F. Hoffmann-La Roche Ltd., Madison Industries, EKF Diagnostics Holdings plc., HORIBA, Ltd., Sysmex Corporation, Danaher Corporation, Abbott Laboratories, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc. |

Analyst Review

This section provides various opinions of top-level CXOs in the global point of care hematology diagnostics market. According to the insights of CXOs, the global point of care hematology diagnostics market is expected to exhibit high growth potential due to increase in demand for rapid and accurate diagnostic solutions, especially in remote and resource-limited settings. Rise in the prevalence of hematological conditions such as anemia, leukemia, and clotting disorders drives the need for immediate testing and treatment decisions, which point-of-care devices effectively support.

CXOs further added that advancements in portable and user-friendly diagnostic technologies, combined with growing awareness of early disease detection, accelerate market adoption. Government healthcare initiatives and rise in trend of decentralized healthcare further contribute to market potential. Furthermore, North America dominated the market in terms of revenue in 2023, owing to the strong presence of key industry players, rise in prevalence of hematological disorders, well-established healthcare infrastructure, and early adoption of advanced diagnostic technologies. In addition, increase in emergency department visits and demand for rapid diagnostic solutions are expected to further boost market expansion during the forecast period. However, Asia-Pacific is anticipated to witness notable growth owing to rise in cases of hematological disorders such as anemia and leukemia, particularly in densely populated countries such as India and China. In addition, rise in awareness about early diagnosis, high investments in healthcare infrastructure, and increase in government initiatives to improve rural healthcare access drive market growth in the region.

The total market value of point of care hematology diagnostics market was $2.4 billion in 2023.

The forecast period for point of care hematology diagnostics market is 2024 to 2030.

The market value of point of care hematology diagnostics market is projected to reach $3.6 billion by 2030.

The base year is 2023 in point of care hematology diagnostics market .

Top companies such as Sysmex Corporation, Danaher Corporation, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Abbott Laboratories, and HORIBA, Ltd. held a high market position in 2023.

Loading Table Of Content...

Loading Research Methodology...