Market")

Quantum Dots Market Overview:

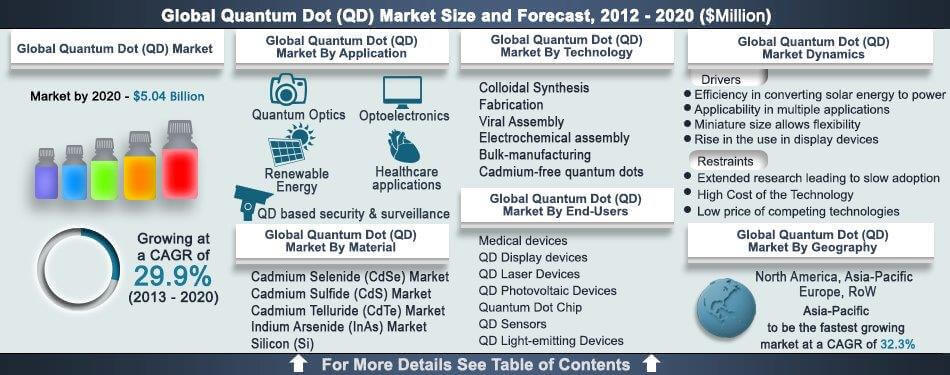

Quantum Dots Market was valued $316 million, and is expected to reach $5,040 million in 2020, supported by a CAGR of 29.9%. Quantum dot is small semiconductor in crystal format that is used in business verticals that use display and monitor devices and many other types of equipment.

Global Nano-optimized industry is expected to reach 3 trillion by 2015. Increasing demand for optimized devices with better performance and resolution quality is a major driving force to adopt this technology into various application areas. Brightness of quantum dots is 10-20 times higher than organic dyes. As the semiconductor material shrink to quantum-dot level, it helps in altering the light wavelength material and covert material from insulator to conductor. Thus, demand in Quantum Dots (QD) market has increased over the past five to six years. Quantum dots are semiconductors that can be used for different devices instead of searching for new semiconductor with special chemical composition. Major application for quantum dots (QD) are display and monitor as quantum dots are used in LED. However, the process of manufacturing Blue quantum dots in size that is smaller than average is very difficult over other colors of quantum dots, this is acting as major limiting factor to adopt quantum dots in display and monitor products. Despite few disadvantages, quantum dots are going to capture attention by major players, but it is very difficult for manufacturers to analyze potential application of quantum dots. This report covers potential application segment and size of the revenue generated by each segment.

Quantum Dots (QD) Market Key Benefits:

- This report analyses the factors that are driving and limiting the development of the Quantum Dot market

- Estimations of Quantum Dots market are done according to the current and emerging trends, and share for the forecast period 2013-2020

- Analysis of key strategies adopted by industry players through their press releases would assist in providing in-depth understanding of the industry intelligence

- Deep-dive analysis of Quantum Dots market in association with various geographies would give an understanding of the trends in various regions so that companies can make region specific plans

- In-depth analysis of segments such as applications, end-users (devices), technologies and materials provide insights that would allow companies to gain competitive edge

By Application

The QD industry is segmented into various applications such as biological imaging, optoelectronics, quantum optics, security & surveillance, and renewable energy. The biological imaging sector is the most mature segment in terms of revenue and it is expected to contribute to the growth of the Quantum Dots market. However, the optoelectronics application is expected to have the highest potential for the analysis period 2013 and 2020. The renewable energy application is the next fastest growing application in the QD market.

By Devices

The quantum dot based devices are the end-users of the technology as these particles are used to develop devices for various applications. The end-user segment consists of QD Medical Devices, QD LCD and LED Display Devices, QD Laser Devices, QD Photovoltaic Devices, QD Chip, QD Sensors, and QD LED Lighting Devices. The QD based medical devices currently have the highest share as medical scientists have been engaged in developing these devices for more than two decades. However, the display devices are expected to have the highest growth rate in the QD market, as the technology enhances the color quality of display devices and saves energy; this is followed by photovoltaic devices segment.

By Technology

QDs are produced by using various technologies such as colloidal synthesis, fabrication, viral assembly, electrochemical assembly, bulk manufacturing and cadmium free QD technology. Colloidal synthesis is the most popular technology in the sector currently, as it has the potential to produce QDs at a large scale. However, it is expected that bulk manufacturing would have the highest revenue share with the highest growth rate due to its ability of large scale QD production with better quality. The cadmium free QD technology is expected to have the second highest growth, as it would be used in consumer applications, since cadmium has restrictions for use in these applications.

By Material

QDs are produced by processing some materials such as Cadmium Selenide, Cadmium Sulphide, Cadmium Telluride, Indium Arsenide, and Silicon. Cadmium Selenide was the most commonly used material to produce QDs in 2013 followed by Cadmium Sulfide, as these were the first materials that were ever used in the process. However, Indium Arsenide would have the highest growth rate for the analysis period 2013-2020 along with the highest revenue by 2020. This is followed by the silicon material, since it is observed that the light emission capacity of silicon is in excess of 70% and can be used in electronic devices to increase efficiency.

By Geography

The Quantum Dots market is geographically segmented into North America, Europe, Asia-Pacific and Rest of the World (RoW). Currently, North America has the highest revenue share followed by Europe due to early adoption of the QD technology. However, for the analysis period of 2012-2020, it is expected that the Asia-Pacific region would have the highest growth rate followed by the RoW region.

Competitive Analysis

Key Companies profiles included in this report are Sony Corporation; Altair Nanotechnology,Inc; Evident Technologies, LG Display, Life Technologies Corporation, Microvision Inc; Quantum Material Corporation; Samsung Electronics Co. Ltd, Nexxus Lighting Microvision Inc. The companies have opted for partnerships and collaborations as a key strategy so that they can share the expertise to develop better QD based products and solutions, as it is an evolving technology.

High-Level Analysis

The report analyses the potency of suppliers and buyers along with threats of new entrants and substitute products based on the Porters five force analysis. The report also analyses the impact of the drivers, restraints and opportunities as per the current trends and projected future scenario. The key investment pockets are analyzed in the report based on the estimations of the application segment.

Reason for doing the study

The commercial prospects of the sector are inclined towards growth due to the efficiency of QDs to produce energy efficient and flexible products and solutions. The industry is currently at a pre-commercialized stage and the report covers the research efforts undertaken to commercialize the market. Estimation of market share and size are made on the basis of some assumptions of the past years volume production and expected production in the future and projected price fluctuations. The report gives a deep dive-analysis on applications in various sectors of the sector to give prominent players an understanding of various lucrative segments. The report also studies the impact and penetration of the QD technology in various geographic regions so that companies can understand end-user preferences to gain competitive advantage.

Quantum Dots (QD) Market Report Highlights

| Aspects | Details |

| By Application |

|

| By End Users |

|

| By Technology |

|

| By Material |

|

| By Geography |

|

| Key Market Players | QD Vision, Sony Corporation, Samsung Electronics Co. Ltd, LG Display Co. Ltd, Altair Nanotechnologies, Inc., Nanoco Technologies, Quantum Material Corporation, Nexxus Lighting |

Analyst Review

The commercial prospects of the market are inclined towards growth due to the efficiency of QDs to produce energy efficient and flexible products and solutions. The market is currently at a pre-commercialized stage and the report covers the research efforts undertaken to commercialize the market. The market estimation are made on the basis of some assumptions of the past years volume production and expected production in the future and projected price fluctuations. The report gives a deep dive-analysis on applications in various sectors of the market to give market players an understanding about the important growth potential to maximize profits. The report also studies the impact and penetration of the QD technology in various geographic regions so that companies can understand end-user preferences to gain competitive advantage.

The report analyses the potency of suppliers and buyers along with threats of new entrants and substitute products based on the Porter’s five force analysis. The report also analyses the impact of the drivers, restraints and opportunities of the market as per the current market trends and projected future scenario. The key investment pockets are analyzed in the report based on the growth estimations of the application segment.

Loading Table Of Content...