Satellite Ground Station Market Research, 2035

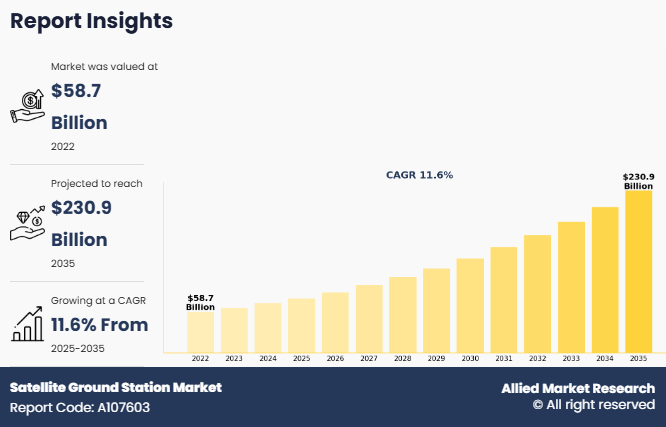

The global satellite ground station market size was valued at $58.7 billion in 2022, and is projected to reach $230.9 billion by 2035, growing at a CAGR of 11.6% from 2025 to 2035. The satellite ground station market growth is driven by rapid increase in satellite launches, rising demand for high-speed and reliable connectivity, expanding applications of Earth observation and remote sensing, and proactive investments by key industry players and governments. The global surge in satellites ranging from small satellites and CubeSats to large constellations in low Earth orbit (LEO) has created consistent demand for advanced ground station infrastructure capable of tracking, commanding, and receiving data from multiple satellites simultaneously. As space agencies, commercial operators, and private enterprises deploy more satellites for communication, navigation, weather monitoring, and imaging, ground stations are under pressure to handle higher data volumes, improve link availability, and ensure uninterrupted mission operations. This has prompted organizations to invest in high-performance, automated ground stations equipped with multi-band antennas, software-defined radios, and cloud-integrated network management systems to enhance operational efficiency and reduce latency.

The growing deployment of low earth orbit (LEO) satellite constellations is creating significant opportunities for the satellite ground station market, as LEO networks require a much denser and more geographically distributed ground infrastructure compared to traditional GEO and MEO systems. The high orbital velocity and shorter visibility windows of LEO satellites increase the frequency of handovers and data downlink sessions, driving demand for a larger number of automated, multi-mission ground stations capable of seamless telemetry, tracking, and command (TT&C) as well as high-throughput data reception. This is accelerating investments in scalable ground station networks, virtualized control systems, and cloud-integrated architectures to efficiently manage the surge in satellite traffic.

In addition, large-scale LEO programs led by operators such as SpaceX (Starlink) and Amazon (Project Kuiper) are encouraging partnerships with commercial ground station service providers to expand global coverage quickly without building all infrastructure in-house. This trend is opening new revenue streams for ground station-as-a-service models, shared infrastructure platforms, and edge data processing solutions. Moreover, the proliferation of small satellites and CubeSats within LEO constellations is fostering demand for cost-effective, modular, and software-defined ground stations, creating opportunities for technology providers to innovate in antenna design, automation, AI-driven scheduling, and network optimization.

Key Takeaways

- On the basis of platform, the fixed segment dominated the satellite ground station market share in 2024. However, mobile segment is anticipated to grow at the fastest CAGR during the forecast period.

- On the basis of function, the communication segment dominated the satellite ground station market in 2024. However, navigation segment is anticipated to grow at the fastest CAGR during the forecast period.

- On the basis of orbit, the LEO segment dominated the satellite ground station market in 2024. However GEO segment is anticipated to grow at the fastest CAGR during the forecast period.

- On the basis of end user, the commercial segment dominated the satellite ground station marketin 2024. However, defense segment anticipated to grow at the fastest CAGR during the forecast period.

- The North America region accounted for the largest satellite ground station market share in 2024. However, Asia-Pacific is anticipated to grow at the fastest CAGR during the forecast period.

Market Dynamics

Surge in satellite deployments, expanding space-based services, and the rapid commercialization of the space industry are fueling demand in the satellite ground station and driving the growth of the Satellite Ground Station Market Size. The proliferation of low Earth orbit (LEO) constellations for broadband connectivity, Earth observation, navigation, and defense applications is significantly increasing the need for scalable, high-throughput, and software-defined ground infrastructure. Modern satellite networks require flexible, automated, and virtualized ground stations capable of supporting multi-orbit operations (LEO, MEO, and GEO), real-time data processing, and secure communications. The growing adoption of high-throughput satellites (HTS), electronically steerable antennas, and cloud-integrated ground segment architectures is accelerating investments across commercial, government, and defense sectors. In addition, the rising demand for satellite-based IoT, remote sensing, maritime connectivity, aviation broadband, and disaster management solutions is strengthening the need for distributed, globally connected ground station networks with enhanced telemetry, tracking, and command (TT&C) capabilities.

The expansion of Industry 4.0, smart agriculture, environmental monitoring, and autonomous systems is further driving the integration of satellite data into enterprise and public-sector decision-making frameworks. Governments are increasingly prioritizing space sovereignty, national security, and resilient communications infrastructure, leading to higher defense budgets and modernization of legacy ground systems. Moreover, the emergence of Ground Station as a Service (GSaaS) models and cloud-based virtualization is enabling satellite operators and new space startups to reduce capital expenditure and accelerate time-to-market without building dedicated ground infrastructure. Automation, artificial intelligence–driven network management, and software-defined networking (SDN) technologies are also transforming ground operations by improving spectrum efficiency, reducing latency, and enhancing operational agility. However, the satellite ground station market faces several restraints. High initial capital investment for antenna systems, RF equipment, secure facilities, and spectrum licensing can limit entry for smaller operators. Regulatory complexities related to spectrum allocation, cross-border data transmission, and licensing approvals can delay project execution.

In addition, vulnerability to cybersecurity threats, signal interference, and space weather disruptions presents operational risks. Supply chain challenges, particularly for specialized RF components, semiconductors, and advanced antenna systems, can result in longer deployment timelines and cost fluctuations. Integration challenges between legacy infrastructure and next-generation, software-defined architectures also create technical and operational hurdles for established operators.

Despite these challenges, the market presents substantial Satellite Ground Station Market growth opportunities. The rapid deployment of mega-constellations, expansion of Earth observation analytics, and increasing defense-focused space programs are expected to drive sustained demand for scalable and automated ground infrastructure. The Asia-Pacific region, particularly China, India, Japan, South Korea, and Southeast Asia, is witnessing strong investments in indigenous satellite programs, digital connectivity initiatives, and space research capabilities, supporting regional ground station expansion. Furthermore, advancements in phased-array antennas, optical ground stations, edge processing at ground nodes, and AI-based network orchestration are enhancing performance, resilience, and cost efficiency which further drive the growth during Satellite Ground Station Market Forecast. The growing emphasis on interoperability, open architectures, cybersecurity-by-design, and long-term lifecycle support is also creating new avenues for differentiation, as satellite operators and governments seek secure, future-ready, and globally integrated ground segment solutions.

Segmental Overview

The satellite ground station market is segmented into platform, function, orbit, end user, and region. On the basis of platform, it is segmented into fixed, portable, mobile. On the basis of function, it is classified into communication, earth observation, space research, navigation, and others. On the basis of orbit, it is classified into LEO, MEO, and GEO. On the basis of end user, it is classified into commercial, government, defense. Region-wise, the market is segmented into North America ( U.S., Canada, and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia, and rest of Europe), Asia-Pacific (Japan, China, Australia, India, South Korea, Thailand, Malaysia, Indonesia, and rest of Asia-Pacific), and LAMEA (Brazil, Saudi Arabia, South Africa, UAE, Argentina and Rest Of LAMEA).

By Platform

On the basis of platform, it is segmented into fixed, portable, and mobile. The fixed segment dominated the market share in 2024, The fixed segment dominated the satellite ground station market share in 2024, primarily owing to its critical role in supporting high-capacity, mission-critical satellite operations across communication, defense, earth observation, and space research applications. Fixed ground stations are typically equipped with large, high-gain antennas and advanced RF systems, enabling reliable and continuous connectivity with satellites in LEO, MEO, and GEO orbits. These installations are designed for long-term operations, offering superior performance, higher bandwidth capabilities, and enhanced signal stability compared to mobile or transportable ground stations.

By Function

On the basis of function, it is classified into communication, earth observation, space research, navigation, and others. The communication segment dominated the market in 2024. The communication segment dominated the market in 2024, primarily driven by the surge in global data consumption, expansion of broadband connectivity, and the rapid deployment of high-throughput satellites and LEO constellations. Increasing Satellite Ground Station Market demand for satellite-based services such as DTH broadcasting, enterprise VSAT networks, in-flight and maritime connectivity, and rural broadband significantly boosted the need for advanced ground station infrastructure. The growing investments by satellite operators and service providers, including companies such as SpaceX and OneWeb, further strengthened the communication segment by expanding global gateway networks and enhancing real-time data transmission capabilities.

By Orbit

On the basis of orbit, it is classified into LEO, MEO, and GEO. The Leo segment dominated the market in 2024. driven by the rapid deployment of large-scale low Earth orbit constellations aimed at delivering high-speed, low-latency connectivity worldwide. The growing demand for broadband internet, real-time data services, IoT connectivity, and defense communications significantly increased the need for advanced ground station networks capable of tracking and communicating with a high volume of fast-moving LEO satellites.

By End User

On the basis of end user, it is classified into commercial, government, defense. The commercial segment dominated the market in 2024 driven by the rapid expansion of private satellite operators, telecom providers, broadcasting companies, and space-tech startups investing heavily in satellite communication and data services. The increasing deployment of LEO constellations by companies such as SpaceX and OneWeb significantly boosted demand for commercial ground station infrastructure to support broadband connectivity, enterprise networks, IoT applications, and media broadcasting.

By Region

Region wise, North America was the largest shareholder in the satellite ground station market in 2024, supported by strong investments in space infrastructure, the presence of leading satellite operators, and advanced technological capabilities. The region benefits from a well-established ecosystem led by organizations such as NASA and private space companies such as SpaceX, which continuously expand satellite constellations and require extensive ground station networks for mission control, data processing, and communication.

Competition Analysis

Key players in the satellite ground station industry include Kratos Defense & Security Solutions, Inc, Comtech Telecommunications Corp, Viasat, Inc., SES S.A. EchoStar Corporation, GILAT SATELLITE NETWORKS, General Dynamics Corporation, Kongsberg Gruppen AS, ST Engineering, and Communications & Power Industries LLC.

Recent Developments in Satellite Ground Station Industry

- In February 2023, Cobham Satcom and RBC Signals, a global provider of satellite data communication solutions, announced the expansion of their existing partnership through a renewed agreement. Under this extended collaboration, RBC Signals will deploy Cobham Satcom’s flexible Tracker 6000 and 3700 series ground station systems across multiple global locations. The partnership is aimed at significantly strengthening RBC Signals’ owned and partner ground station network, enabling the company to deliver enhanced, integrated communication services. This expansion will particularly support non-geostationary orbit (NGSO) missions and satellite constellations serving applications such as Earth observation, Internet of Things (IoT), and space situational awareness.

- In February 2023, China Aerospace Science and Technology Corporation (CASC) announced the successful launch of the Zhongxing-26 communications satellite. Built on the DFH-4E satellite platform, Zhongxing-26 represents a significant technological milestone for China, becoming the country’s first communications satellite capable of delivering data transmission speeds exceeding 100 gigabits per second (Gbps).

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the satellite ground station market analysis from 2022 to 2035 to identify the prevailing satellite ground station market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the satellite ground station market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global satellite ground station market trends, key players, market segments, application areas, and market growth strategies.

Satellite Ground Station Market Report Highlights

| Aspects | Details |

| Market Size By 2035 | USD 230.9 billion |

| Growth Rate | CAGR of 11.6% |

| Forecast period | 2022 - 2035 |

| Report Pages | 374 |

| By Function |

|

| By Platform |

|

| By Orbit |

|

| By End User |

|

| By Region |

|

| Key Market Players | General Dynamics Corporation, GILAT SATELLITE NETWORKS, EchoStar Corporation, Kongsberg Gruppen AS., SES S.A., Comtech Telecommunications Corp., ST Engineering, Communications & Power Industries LLC, Viasat, Inc., Kratos Defense & Security Solutions, Inc. |

Analyst Review

According to the opinions of various CXOs of leading companies, the satellite ground station market is expected to witness an increase in demand during the forecast period. The rise in satellite deployments, particularly Low Earth Orbit (LEO) constellations, and the increasing focus on real-time data delivery and low-latency communication are expected to drive the demand for satellite ground stations. Ground stations play a critical role in tracking, telemetry, and command (TT&C) as well as in receiving large volumes of payload data from satellites, making them integral to the efficient operation of modern satellite missions. As satellite operators seek to optimize network performance, improve coverage continuity, and reduce communication latency, investments in advanced ground station infrastructure provide opportunities to enhance data throughput, automate operations, and improve mission reliability. This demand is particularly evident in sectors such as telecommunications, Earth observation, defense, and weather monitoring, where continuous connectivity and rapid data access are mission-critical.

Moreover, the growing focus on digitalization and cloud-based ground station services is a key driver for the adoption of next-generation satellite ground station solutions. As satellite operations become more complex and data-intensive, traditional standalone ground stations are being complemented or replaced by virtualized, software-defined, and cloud-integrated ground station networks. These solutions enable flexible scaling, global coverage through shared infrastructure, and cost-efficient operations, making them attractive to both established satellite operators and emerging Smallsat and CubeSat mission providers. Their ability to support multi-mission operations, automate scheduling, and integrate with advanced analytics and AI-based monitoring aligns with the industry’s shift toward smarter, more resilient space-ground communication architectures. As organizations aim to enhance operational efficiency while managing rising data volumes, the adoption of modern satellite ground station platforms is expected to accelerate, supporting sustained market growth.

The top companies holding significant market share in the global Satellite Ground Station Market include a mix of traditional aerospace & defence players and specialist ground-segment providers such as General Dynamics Mission Systems, L3Harris Technologies, Inc., RTX (Raytheon Technologies), Airbus Defence and Space, Lockheed Martin Corporation, Kratos Defense & Security Solutions, Inc., Viasat, Inc., SES S.A., Hughes Network Systems, LLC, Gilat Satellite Networks, and Kongsberg Satellite Services (KSAT).

The satellite ground station market was valued at $58,700.00 million in 2022 and is estimated to reach $230,924.09 million by 2035, exhibiting a CAGR of 11.6% from 2025 to 2035.

The largest regional market for the Satellite Ground Station Market is North America, driven by its mature space ecosystem, substantial investments by government agencies and commercial players, and a high concentration of ground station infrastructure.

The leading application of the Satellite Ground Station Market is Communication & Data Transmission, driven by rising demand for broadband connectivity, satellite internet (LEO constellations), enterprise networks, and secure government/military communications worldwide.

Key upcoming global trends in the Satellite Ground Station Market include the rapid shift toward Cloud-based and Ground-Station-as-a-Service (GSaaS) models with automated, software-defined operations, and the integration of optical/laser communications, AI, and advanced phased-array antennas to support dense LEO/MEO satellite constellations and high-throughput data links.

Loading Table Of Content...

Loading Research Methodology...