Structural Steel Tube Market Research, 2033

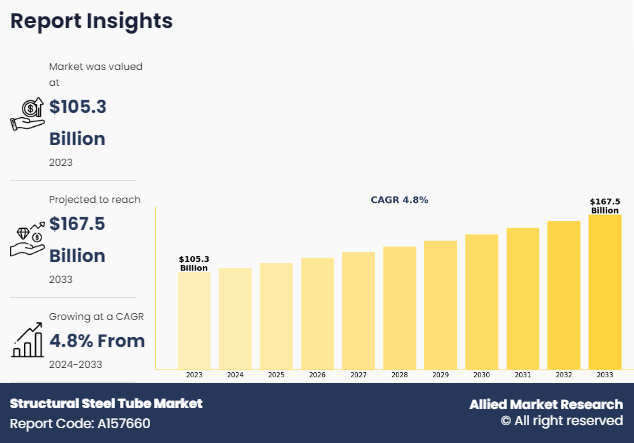

The global structural steel tube market was valued at $105.3 billion in 2023, and is projected to reach $167.5 billion by 2033, growing at a CAGR of 4.8% from 2024 to 2033. Structural steel tubes, also known as hollow structural sections (HSS), are essential components in construction and structural applications, characterized by their high strength-to-weight ratio and versatile usage. These tubes, available in rectangular, square, and circular cross-sections, are manufactured through welding, seamless rolling, and cold drawing, ensuring precise dimensions and durability. Their inherent properties make them ideal for load-bearing applications, reducing overall weight without compromising strength.

Structural steel tubes are widely used in building frameworks, bridges, tunnels, and various architectural features due to their clean lines and smooth surface finish. In addition, they are integral in industrial machinery and transportation structures. The high durability of these tubes, coupled with their resistance to compression, bending, and torsional stresses, ensures long-term performance and efficiency in material use, making them indispensable in modern construction and engineering.

Rapid urbanization and infrastructure expansion are key factors driving the structural steel tube market growth. As construction in cities grow, the demand for durable construction materials such as structural steel tubes rises, supported by significant investments in infrastructure projects globally. Major initiatives such as China's Belt and Road Initiative and U.S. infrastructure plans highlight this trend.

Structural steel tubes, with their high strength-to-weight ratio and versatility, are ideal for modern construction, aligning with sustainable practices due to their durability and recyclability. In addition, technological advancements in manufacturing, such as electric resistance welding (ERW) and seamless rolling, have improved corrosion resistance and strength of steel tubes. Innovations in digital design and modeling tools further enhance material efficiency and structural integrity. These advancements facilitate the construction of complex, aesthetically pleasing structures, driving the adoption of advanced structural steel tubes to meet the evolving needs of the construction and industrial sectors.

Fluctuating raw material prices significantly restrain the structural steel tube market forecast due to the volatility of steel costs, driven by global supply and demand, geopolitical tensions, and trade policies. These fluctuations impact manufacturers' cost structures and profitability, complicating long-term planning and potentially hindering the market growth. The reliance on a global supply chain further exacerbates these issues, as seen during the COVID-19 pandemic. In addition, intense competition within the market, characterized by numerous players globally and regionally, leads to price wars and low-profit margins. Established companies dominate the structural steel tube industry, making it challenging for smaller or newer entrants to gain market share. The pressure to innovate and reduce costs necessitates substantial investment in R&D, posing significant operational challenges, especially for companies with limited financial resources. This competitive environment demands continuous improvement and efficiency, further restraining new entrants in the market.

Emerging markets, particularly in Asia-Pacific, Africa, and Latin America, offer significant growth opportunities for the structural steel tube market due to rapid industrialization and urbanization. Countries such as India, Brazil, and Nigeria invest heavily in infrastructure projects requiring robust materials, making structural steel tubes an ideal product.

Supportive government policies from the abovementioned countries further enhance market potential in these regions. In addition, technological advancements such as development of new alloy steel, and coating in developing countries are creating opportunities for the development of the structural steel market growth. Innovations in production technologies, such as automation and digitalization, improve manufacturing efficiency and product quality. Tools such as advanced modeling software and Building Information Modeling (BIM) enable precise design and material usage, optimizing performance of structural steel pipe. Advancements in material science are also leading to new steel alloys with better properties, meeting the demands of modern construction and expanding application areas. These factors collectively provide ample opportunities for market expansion and growth.

The structural steel tube market is segmented on the basis of type, material, sales type, application, and region. On the basis of type, the market is segmented into hot-rolled steel and cold-rolled steel. On the basis of material, it is divided into stainless steel tube, carbon steel tube, alloy steel tube, and others. On the basis of sales type, it is segmented into direct and distribution. On the basis of application, it is segmented into industrial machinery, medical, aerospace and military, transportation, construction, automotive, energy, and others. Region-wise, the market is studied across North America, Europe, Asia-Pacific, and LAMEA. Currently, Asia-Pacific accounts for the largest share of the market, followed by North America and Europe.

The hot-rolled steel type segment dominates the structural steel tube market size due to its superior mechanical properties, cost-effectiveness, and versatility. Hot-rolled steel tubes are manufactured by rolling steel at high temperatures, which makes the steel easier to shape and form, resulting in stronger and more durable products. This process also allows the production of larger sizes and varied shapes, catering to diverse construction and industrial applications.

Hot-rolled steel tubes are preferred in construction projects for their robustness, that are essential for structural integrity in buildings, bridges, and other infrastructure. Additionally, they offer better weldability and machinability, simplifying fabrication and reducing labor costs. The lower production costs of hot-rolled steel compared to cold-rolled alternatives make it a more economical choice for large-scale projects. These factors collectively drive the dominance of hot-rolled steel tubes in the structural steel tube market, meeting the high demand for reliable and affordable building materials.

The carbon steel tube material segment dominates the structural steel tube market share due to its superior mechanical properties, cost-effectiveness, and wide availability. Carbon steel tubes offer high tensile strength, durability, and resistance to wear and tear, making them ideal for demanding construction and engineering applications. In addition, carbon steel is more affordable compared to other materials like stainless steel or aluminum, providing a cost-efficient solution for large-scale projects. Its versatility allows for easy fabrication and welding, further enhancing its appeal in various industries such as construction, automotive, and manufacturing. Moreover, advancements in carbon steel production techniques have improved its quality and performance, reinforcing its dominance in the market. The combination of these factors such as strength, affordability, versatility, and technological advancements ensures that carbon steel tubes remain the preferred choice for structural applications, driving their significant market share.

The distribution sales type segment dominates the structural steel tube market due to its extensive network, which ensures wide market coverage and accessibility. Distributors often have established relationships with numerous buyers, including small and medium-sized enterprises, enabling efficient supply chain management and timely delivery of products. Their ability to offer various products from multiple manufacturers also provides customers with a broader selection, enhancing their purchasing convenience.

Conversely, the direct sales type application segment is fastest growing due to the increasing preference for customized solutions and direct communication between manufacturers and end-users. This sales type allows for a better understanding of specific customer requirements, leading to tailored product offerings and enhanced customer satisfaction. Direct sales also help manufacturers build stronger brand loyalty and reduce intermediary costs, resulting in competitive pricing and higher profit margins. The growing emphasis on personalized customer service and efficiency drives the rapid growth of the direct sales segment in the structural steel tube market.

The construction segment dominates the structural steel tube market in 2023, due to the extensive use of these tubes in various infrastructure projects, including commercial buildings, residential complexes, and industrial facilities. Structural steel tubes offer high strength, durability, and flexibility, making them ideal for withstanding heavy loads and ensuring structural integrity in construction. In addition, the growing trend of urbanization and the need for modern infrastructure drive the demand for structural steel tubes in the construction industry.

However, the medical segment is the fastest-growing due to the increasing adoption of advanced medical equipment and devices. Structural steel tubes are essential in manufacturing hospital beds, surgical instruments, and diagnostic equipment due to their biocompatibility, corrosion resistance, and ease of sterilization. The rise in healthcare infrastructure development, coupled with advancements in medical technology, fuels the rapid growth of structural steel tubes in the medical sector, catering to the escalating healthcare demands.

Based on the region, Asia-Pacific held the highest market share in 2023. Rapid urbanization and industrialization in countries like China and India drive significant demand for construction and infrastructure projects. These nations invest heavily in building residential, commercial, and industrial structures, requiring substantial quantities of structural steel tubes for their strength and durability.

In addition, government initiatives and policies in the region, aimed at improving infrastructure and boosting economic growth, further stimulate market demand. The availability of raw materials and cost-effective manufacturing processes in Asia-Pacific contributes to its leading position. Moreover, the expansion of the automotive and aerospace industries in the Asia-Pacific region fuels the need for structural steel tubes in various applications. Technological advancements and innovations in steel production enhance product quality and performance, making the region a key player in the global structural steel tube market.

Major companies profiled in this report include Arcelor Mittal SA, Tata Steel Group, JFE Steel Corporation, Nippon Steel & Sumitomo Metal Corporation, POSCO AG, Baosteel Group Corporation, HYUNDAI Steel Co., Ltd., Nucor Corporation (Nucor Tubular Products), APL Apollo Tubes Ltd., and Gerdau S.A.

The rapid development of industrialization and modernization led to the development of the construction industry which drives the demand for the structural steel tube. In addition, growth strategies such as the expansion of production capacities, acquisition, partnership, and research & innovation in steel tube applications are key development trends in the global structural steel tube market.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the structural steel tube market analysis from 2023 to 2033 to identify the prevailing structural steel tube market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the structural steel tube market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global structural steel tube market trends, key players, market segments, application areas, and market growth strategies.

Structural Steel Tube Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 167.5 billion |

| Growth Rate | CAGR of 4.8% |

| Forecast period | 2023 - 2033 |

| Report Pages | 375 |

| By Application |

|

| By Type |

|

| By Material |

|

| By Sales Type |

|

| By Region |

|

| Key Market Players | Baosteel Group Corporation, Arcelor Mittal, HYUNDAI Steel, Nucor Corporation, NIPPON STEEL CORPORATION., JFE Steel Corporation, POSCO HOLDINGS INC., Tata Steel, Maanshan Iron & Steel Company Limited, APL Apollo Tubes Ltd., Gerdau S.A. |

Analyst Review

CXOs in the structural steel tube industry recognize the significant growth potential and opportunities during the forecast period. Rise in demand for structural steel tube , is driven by expanding infrastructure development and industrialization across various regions. The construction sector, in particular, is expected to have substantial growth due to rise in urbanization and investment in construction of manufacturing facilities.

CXOs acknowledge the critical role of structural steel tubes as fundamental components in modern construction and engineering. These tubes, available in types such as hot rolled steel, cold rolled steel, and welded options, offer versatile solutions that cater to diverse customer needs. The market's segmentation by material, including stainless steel tubes, carbon steel tubes, alloy steel tubes, and others, enables targeted applications across various industries. The versatility and adaptability of these materials ensure that structural steel tubes remain essential in the construction, industrial, medical, aerospace, military, and transportation sectors.

CXOs are confident in their ability to capitalize on several market drivers, including a strong consumer inclination towards durable and efficient building materials. Moreover, favorable government infrastructure projects and investments further boost market adoption. The steady increase in industrial activities, particularly in emerging economies, presents lucrative opportunities for growth and expansion of the market. With robust demand in various applications, structural steel tubes are expected to see significant market penetration and utilization.

Historical trends indicate that the hot-rolled steel segment emerged as a significant player in 2023, capturing a major share of the two-third market due to its robustness and wide application range. Similarly, the stainless steel tube segment has seen surge in demand in 2023 driven by its superior corrosion resistance and aesthetic appeal, making it a preferred choice in architectural and medical applications. These trends underscore the importance of material-specific advantages in driving market growth.

CXOs are attentive to market dynamics and forecast predictions indicating that the industrial application segment is expected to experience the highest growth rate during the forecast period. CXOs are strategically positioning their production and sales capacity to cater to potential demand and capture a significant share of market growth. The construction segment, which held the maximum market share in recent years, is expected to continue its dominance, fueled by rapid urbanization, and increasing consumer income levels, especially in emerging economies.

By leveraging both direct and distribution sales types, CXOs aim to optimize market reach and efficiency. The direct sales type allows for stronger customer relationships and tailored solutions, while the distribution channel expands market presence and accessibility. Overall, the structural steel tube market presents a favorable landscape for growth and innovation, with CXOs strategically positioned to harness these opportunities and drive market leadership.

$167.5 billion is the estimated industry size of Structural Steel Tube

Sustainability and green building initiatives, technological advancements, increased demand from emerging markets, rise in modular and prefabricated construction, expansion in end-use industries, fluctuating raw material prices and supply chain issues, innovation in alloy compositions, digitalization and industry 4.0, regulatory changes are the upcoming trends of Structural Steel Tube Market in the world.

Construction is the leading application of Structural Steel Tube Market.

Asia-Pacific is the largest regional market for Structural Steel Tube.

Arcelor Mittal SA, Tata Steel Group, JFE Steel Corporation, Nippon Steel & Sumitomo Metal Corporation, POSCO AG, Baosteel Group Corporation, HYUNDAI Steel Co., Ltd., Nucor Corporation (Nucor Tubular Products), APL Apollo Tubes Ltd., and Gerdau S.A are the top companies to hold the market share in Structural Steel Tube.

Loading Table Of Content...

Loading Research Methodology...