White Cement Market Overview

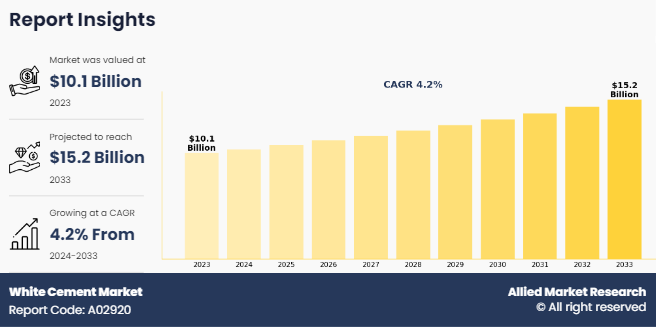

The global white cement market size was valued at USD 10.1 billion in 2023, and is projected to reach USD 15.2 billion by 2033, growing at a CAGR of 4.2% from 2024 to 2033. The increase in development in architectural and decorative construction industry is expected to fuel the demand for white cement globally. The growing use of white cement in applications such as cladding panels for interior and exterior walls, median barriers, kerbstones, and decorative garden concrete products is driving market growth.

Rising construction activities, combined with strong collaboration between white cement producers and manufacturers of white cement-based products, are further fueling demand. Additionally, white cement is increasingly preferred for high-quality finishing of both interior and exterior walls, highlighting its versatility and aesthetic appeal in modern construction projects.

Introduction

White cement is a premium variant of ordinary Portland cement, valued for its bright color, aesthetic appeal, and versatility. Its high whiteness provides a clean, uniform canvas for architectural and decorative applications, allowing vibrant finishes and intricate designs. Unique properties include superior strength, smooth texture, and compatibility with various pigments and additives, enabling polished, textured, or stained surfaces. White cement also offers durability, resistance to weathering, and low thermal conductivity, making it suitable for both interior and exterior projects. These attributes make it a preferred choice for high-end residential, commercial, and renovation projects where aesthetics and performance are equally important.

White cement has low energy consumption and is often combined with pigments. Thus, it enables the creation of colored concretes and mortars that are not achievable with ordinary gray cement. Its whiteness is derived from carefully selected raw materials, such as low-iron and low-manganese components, and the use of fuel oil instead of coal, with iron oxide content kept below 0.4%. A specialized cooling process further preserves its color. White cement is widely used in architectural and decorative applications, including terrazzo tiles, paints, pavers, and prefabricated products such as artificial walls and tile adhesives.

White cement is widely used in architectural and decorative applications due to its bright color and versatility. It is ideal for creating aesthetically appealing structures, including interior and exterior wall finishes, flooring, terrazzo tiles, and decorative facades. White cement is commonly used in precast and prefabricated elements, pavers, garden ornaments, and kerbstones. Its compatibility with pigments allows vibrant colored concretes and mortars. Additionally, it is used in high-end residential and commercial projects, historical restorations, and artistic creations where appearance is critical. Its durability, smooth texture, and design flexibility make white cement a preferred choice for modern construction and renovation projects.

Key Takeaways

The key players in the white cement market report are Cementir Holding SPA, Çimsa Cement Industry and Trade Inc., JK Cement, Cemex, The Cementos Portland Valderrivas, Birla White (Ultratech), Federal White Cement, Saveh White Cement Co., Adana Cement, and Saudi White Cement Co. The other key players include Lafargeholcim, Secil, Dyckerhoff, Royal El Minya Cement, Fars & Khuzestan Cement Co., SCG, Italcementi, Rakwhitecement.Ae, Union Cement Company, Royal White Cement, and Neyeariz White Cement Company.

The segment analysis of each country in terms of value and volume during the forecast period 2023-2033 is covered in the global white cement market report.

More than 6,765 product literatures, industry releases, annual reports, and other such documents of major industry participants along with authentic industry journals, trade associations' releases, and government websites have been reviewed for generating high-value industry insights.

Market Dynamics

Drivers

Rising demand for aesthetically appealing construction and decorative solutions is a major driving factor for the white cement market. Rapid urbanization and increasing disposable incomes are fueling the adoption of premium materials in residential, commercial, and hospitality projects. Growing use of white cement for cladding panels, flooring, precast elements, and decorative products further supports market expansion. Sustainability trends and eco-friendly construction practices are encouraging innovation in white cement formulations. Additionally, technological advancements, such as improved durability, pigment compatibility, and versatile finishes, enhance its appeal among architects and designers. Strong collaborations between cement producers and product manufacturers also bolster market growth.

Restraints

The white cement market faces constraints due to its higher cost compared to ordinary gray cement, limiting adoption in price-sensitive projects. Production requires carefully selected raw materials and specialized processes, increasing manufacturing expenses. Additionally, lack of awareness in certain regions about its aesthetic and functional benefits restricts market penetration. Fluctuating raw material availability and energy-intensive production methods also pose challenges. These factors collectively hinder widespread use, particularly in small-scale construction and developing markets, slowing overall growth despite rising demand for premium construction solutions.

Opportunities

Growing urbanization and the expansion of high-end residential, commercial, and hospitality projects are creating new applications for white cement in flooring, cladding, precast elements, and decorative finishes. Innovations in eco-friendly formulations and pigment-compatible products enable manufacturers to cater to evolving customer preferences. Additionally, restoration of heritage buildings and rising interest in customized architectural designs offer further potential. Strategic collaborations between cement producers and construction product manufacturers can enhance distribution and market reach, supporting long-term growth in this premium segment. Thus, the demand for sustainable and aesthetically appealing construction solutions is expected to create lucrative opportunities for the white cement industry.

The increasing use of white cement in decorative concrete for roofing and flooring creates visually appealing and soothing effects, driving growth opportunities in the global white cement market. Expansion in white cement applications for flooring, roofs, and other decorative surfaces is expected to boost demand, offering lucrative prospects for manufacturers and suppliers.

Ongoing innovations in white cement technology further support market expansion. Companies are developing advanced formulations, specialized additives, and improved production techniques to enhance performance, durability, and environmental sustainability. By staying at the forefront of technological innovation, manufacturers can capitalize on emerging trends and evolving customer preferences, strengthening their market position and driving sustained growth.

Segments Overview

The global white cement industry is segmented based on type, end use, and region. On the basis of type, it is classified into white Portland cement, white masonry cement, and others. On the basis of end use, it is divided into residential, commercial, and industrial. By region, the white cement market share is analyzed across North America, Europe, Asia-Pacific, Latin America and MEA.

By type, the white Portland cement segment accounted for more than two-thirds of global white cement market share in 2023 and is expected to maintain its dominance during the forecast period. White Portland cement has aesthetic appeal and versatility in architectural and decorative applications. Its bright white color provides a pristine canvas for architectural designs, enabling the creation of visually striking structures and surfaces. Architects, designers, and builders prefer white cement for projects where aesthetics play a crucial role, such as high-end residential buildings, commercial spaces, and historical restoration projects. All these factors drive the demand for the white Portland cement segment in the white cement market.

By end use, the residential segment accounted for less than half of global white cement market share in 2023 and is expected to maintain its dominance during the forecast period. White cement offers exceptional flexibility in design, enabling the creation of bespoke features tailored to individual preferences. Its adaptability to various finishes, such as polished, textured, or stained, allows for the realization of diverse design concepts, ranging from minimalist to lavish. This versatility fosters creativity and innovation, empowering architects, and designers to explore new possibilities in residential construction and renovation projects.

Asia-Pacific accounted for two-fifths of the global white cement market share in 2023 and is expected to maintain its dominance during the forecast period. The surge in disposable incomes and changing lifestyles of consumers in Asia-Pacific are influencing the demand for premium construction materials such as white cement. As aspirations for modern and luxurious living spaces increase, there is a growing preference for high-end finishes and architectural elements that utilize white cement. In addition, the rise in tourism and hospitality sectors in many Asia-Pacific countries are contributing to the demand for white cement. The construction of hotels, resorts, shopping malls, and entertainment complexes requires materials that exude elegance and sophistication, making white cement a preferred choice for interior and exterior applications.

Who Are the Primary End Users Driving Market Adoption?

The primary end users driving white cement market adoption include architects, builders, contractors, and interior designers who prioritize aesthetics and high-quality finishes in construction projects. Residential developers use white cement for premium homes, luxury apartments, and renovation projects, while commercial and hospitality sectors apply it in hotels, resorts, shopping malls, and office complexes. Additionally, precast and decorative product manufacturers rely on white cement for terrazzo tiles, pavers, garden ornaments, and façade elements. Increasing awareness among end users about its versatility, durability, and compatibility with pigments further boosts demand, making these stakeholders key drivers of market growth in both domestic and international markets.

What Role Do Digital Technologies Play in Improving Products and Services?

Digital technologies are transforming the white cement industry by enhancing product quality, operational efficiency, and customer service. Advanced data analytics and process automation optimize production, ensuring consistent whiteness, strength, and durability. Digital tools enable real-time monitoring of raw materials, energy use, and emissions, supporting sustainable and cost-effective manufacturing. Additionally, 3D modeling, virtual design software, and AI-assisted simulations allow architects and builders to visualize and customize white cement applications in flooring, facades, and decorative elements. Smart supply chain platforms improve delivery accuracy and reduce lead times. Collectively, these technologies drive innovation, improve product performance, and elevate service standards in the white cement market.

What Technological Innovations Are Creating New Growth Opportunities?

Technological innovations in the white cement industry are creating significant growth opportunities by enhancing performance, sustainability, and versatility. Advanced formulations and specialized additives improve durability, whiteness, and resistance to weathering, enabling use in high-end architectural and decorative applications. Innovations in pigment compatibility allow for vibrant colored concretes and mortars, expanding design possibilities in residential, commercial, and hospitality projects. Energy-efficient and low-emission production technologies reduce environmental impact while lowering operational costs, aligning with the growing demand for sustainable construction. Additionally, the adoption of digital process controls and automation ensures consistent quality, precise mixing, and optimized resource utilization. Prefabrication and 3D printing techniques further open new avenues for customized structural and decorative elements. By integrating these technological advancements, manufacturers can diversify product offerings, cater to evolving customer preferences, and strengthen their competitive position in the expanding white cement market.

How Are Consumer Preferences Shaping Market Trends?

Consumer preferences are strongly influencing trends in the white cement market, particularly the demand for aesthetics, customization, and sustainable construction. Homeowners, architects, and designers increasingly seek visually appealing finishes, vibrant colors, and smooth textures for residential and commercial projects. Growing interest in eco-friendly and low-energy materials is driving manufacturers to develop sustainable white cement formulations. Additionally, preferences for premium and durable products are fueling the adoption of white cement in flooring, facades, roofing, and decorative elements. By responding to these evolving expectations, manufacturers can introduce innovative products, expand their offerings, and capitalize on the rising demand for stylish, high-performance construction solutions.

What is the Long-Term Outlook for the Market?

The long‑term outlook for the global white cement market remains positive through the next decade, supported by growing construction demand, urbanization and aesthetic and performance‑driven applications. Growth drivers include heightened use in decorative architectural finishes, heat‑reflective roofing, façade cladding and high‑end residential and commercial projects, especially in Asia‑Pacific, the Middle East & Africa and India, where demand is stronger. Sustainability trends also support long‑term demand, as regulations and green‑building practices favor materials with lower embodied emissions and premium performance.

However, higher cost relative to grey cement and raw material availability constraints could temper adoption in price‑sensitive segments. Overall, the white cement market is projected to expand steadily over the long term as construction activity and urbanization continue, with opportunities in customized and eco‑friendly product lines.

Competitive Analysis

The key players profiled in the white cement market report include Cementir Holding SPA, Çimsa Cement Industry and Trade Inc., JK Cement, Cemex, The Cementos Portland Valderrivas, Birla White (Ultratech), Federal White Cement, Saveh White Cement Co., Adana Cement, and Saudi White Cement Co. The other key players include Lafargeholcim, Secil, Dyckerhoff, Royal El Minya Cement, Fars & Khuzestan Cement Co., SCG, Italcementi, Rakwhitecement.Ae, Union Cement Company, Royal White Cement, and Neyeariz White Cement Company.

Recent Key Developments in the White Cement Market

In October 2025: Asian Paints’s subsidiary Asian White Inc. FZE commenced commercial production at a new white cement plant in Fujairah, UAE, with an initial capacity of ~265,000 t/yr, marking the company’s strategic expansion into international white cement manufacturing.

In September 2025: CEMEX launched a new range of eco‑friendly white cement products to meet growing sustainable construction demand.

In August 2025: LafargeHolcim partnered with a technology firm to develop a digital supply‑chain platform aimed at enhancing operational efficiency and customer responsiveness.

In June 2025: Çimsa announced investment plans at its Buñol white cement plant in Spain to develop alternative fuels and energy‑efficient processes.

In February 2025: Mannok introduced “Ultra White Cement,” a high‑reflectance product for architectural use, broadening product offerings in Europe.

In April 2025: UltraTech Cement agreed to acquire Wonder WallCare’s white cement assets, strengthening its putty and wall‑covering portfolio in India.

Key Benefits for Stakeholders

This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the white cement market analysis from 2023 to 2033 to identify the prevailing white cement market opportunities.

The white cement market research is offered along with information related to key drivers, restraints, and opportunities.

Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

In-depth analysis of the white cement market segmentation assists to determine the prevailing market opportunities.

Major countries in each region are mapped according to their revenue contribution to the global market.

Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

The report includes the analysis of the regional as well as global white cement market trends, key players, market segments, application areas, and market growth strategies.

White Cement Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 15.2 billion |

| Growth Rate | CAGR of 4.2% |

| Forecast period | 2023 - 2033 |

| Report Pages | 280 |

| By Type |

|

| By End Use |

|

| By Region |

|

| Key Market Players | Cementir Holding SPA, Adana Cement, JK Cement, CEMEX, S.A.B. de C.V., Birla White (Ultratech), Çimsa Cement Industry and Trade Inc., Federal White Cement, The Cementos Portland Valderrivas, Saudi White Cement Co., Saveh White Cement Co. |

Analyst Review

According to the insights of the CXOs of leading companies, the white cement market is driven by rapid urbanization and the construction of new infrastructure projects, such as airports, bridges, and highways, contribute to the demand for white cement. Emerging economies undergoing significant urbanization typically exhibit strong demand for construction materials, including white cement.

White cement is valued for its aesthetic appeal and versatility in architectural design. Trends favoring modern and minimalist designs, as well as the use of white or light-colored materials, can boost demand for white cement products. Manufacturers are continuously innovating to develop new white cement formulations with improved performance characteristics, such as strength, durability, and workability. Innovations in production processes and the introduction of eco-friendly or sustainable white cement variants can stimulate market growth.

The white cement market was valued at $10.1 billion in 2023, and is estimated to reach $15.2 billion by 2033, growing at a CAGR of 4.2% from 2024 to 2033.

Asia-Pacific is the largest regional market for White Cement

Rapid demand for aesthetics in the construction industry and rapid urbanization in developing countries are the leading drivers for the White Cement Market

Residential industry is the leading application of White Cement Market

Sustainable construction practices is the upcoming trends of White Cement Market in the world

Asia-Pacific is the fastest growing region for the White Cement Market

The major companies profiled in the report include Cementir Holding SPA, Çimsa Cement Industry and Trade Inc., JK Cement, Cemex, The Cementos Portland Valderrivas, Birla White (Ultratech), Federal White Cement, Saveh White Cement Co, Adana Cement, and Saudi White Cement Co.

Loading Table Of Content...

Loading Research Methodology...