Engineered Wood Market Research, 2033

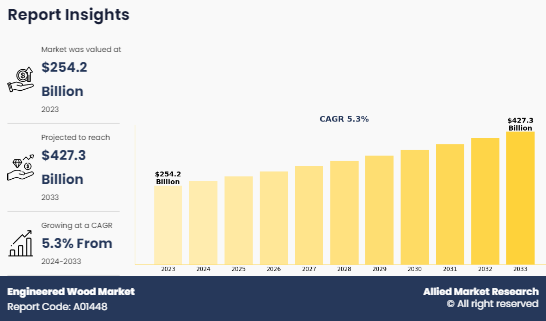

The global engineered wood market size was valued at $254.2 billion in 2023, and is projected to reach $427.3 billion by 2033, growing at a CAGR of 5.3% from 2024 to 2033. Increasing demand for sustainable building materials, rapid urbanization, growth in residential and commercial construction, and advancements in manufacturing technologies are key factors driving the growth of the engineered wood market.

Report Key Highlighters

- The report presents a comprehensive analysis of the engineered wood market, highlighting current developments as well as emerging trends and market dynamics.

- By product type, the plywood segment accounted for the largest share of market revenue in 2023.

- In terms of application, the construction segment dominated the market and held the highest share in 2023.

- By end-user industry, the residential segment represented the largest revenue share in 2023. Furthermore, this segment is anticipated to record the fastest CAGR during the forecast period.

- The Asia-Pacific region is expected to witness the highest growth rate in the engineered wood market over the coming years.

- Major companies operating in the engineered wood market are profiled in the report, and their business strategies are analyzed in detail to provide a clear understanding of the competitive landscape.

- The report also offers a detailed evaluation of ongoing market trends along with potential growth opportunities.

- A thorough industry analysis has been conducted by developing market estimates and forecasts for key segments covering the period from 2024 to 2033.

Report Overview and Definition

The engineered wood market comprises the production, distribution, and sale of wood-based products manufactured by binding or fixing strands, particles, fibers, veneers, or boards of wood together with adhesives or other bonding methods. Engineered wood products are designed to enhance strength, stability, and durability compared to traditional solid wood. Common types include plywood, laminated veneer lumber (LVL), cross-laminated timber (CLT), oriented strand board (OSB), medium-density fiberboard (MDF), and particleboard. These materials are widely used in construction, furniture manufacturing, flooring, cabinetry, and interior design applications.

The manufacturing process typically involves wood fiber processing, drying, adhesive application, layering or pressing, and finishing to achieve uniform strength and performance. Advanced production technologies, automated pressing systems, precision cutting equipment, and quality control processes play a crucial role in ensuring consistent product standards and structural reliability. Engineered wood products offer benefits such as efficient raw material utilization, improved load-bearing capacity, and resistance to warping or cracking, making them suitable for modern construction needs.

Increasing demand for eco-friendly construction materials, rising adoption of modular and prefabricated building techniques, and growing awareness of sustainable forestry practices are contributing to market expansion. Additionally, government initiatives promoting green buildings and carbon-efficient materials are encouraging the use of engineered wood in structural and architectural applications.

As construction activities continue to expand and sustainability remains a key focus, the engineered wood market is expected to witness steady growth between 2024 and 2033, supported by technological innovation, product diversification, and expanding global supply chains.

Market dynamics

The engineered wood market is influenced by rapid urbanization, increasing demand for sustainable construction materials, expansion of residential and commercial infrastructure, and continuous technological advancements in wood processing. Growing awareness of eco-friendly building practices, rising adoption of modular and prefabricated construction techniques, and efficient utilization of forest resources are significantly shaping market growth. In addition, the rising demand for durable, cost-effective, and structurally reliable building materials in furniture manufacturing, flooring, and interior applications is accelerating the adoption of engineered wood products across multiple industries.

Drivers

The engineered wood market is primarily driven by the increasing need for sustainable and high-performance construction materials. As global construction activities expand, builders and developers are increasingly adopting engineered wood products due to their strength, dimensional stability, and efficient use of raw materials. Products such as plywood, cross-laminated timber (CLT), laminated veneer lumber (LVL), and medium-density fiberboard (MDF) offer improved load-bearing capacity and design flexibility, making them suitable for modern architectural and structural applications.

Technological advancements in wood processing and manufacturing techniques are also key drivers of market growth. Automated production lines, advanced pressing technologies, precision cutting systems, and improved adhesive formulations enhance product quality, durability, and consistency. Additionally, engineered wood products allow manufacturers to utilize smaller wood fibers and recycled materials, reducing waste and supporting sustainable forestry practices. Government initiatives promoting green buildings, carbon reduction, and environmentally responsible construction materials are further encouraging the adoption of engineered wood in infrastructure and building projects.

Restraints

Despite favorable growth prospects, the engineered wood market faces certain challenges. Fluctuations in raw material availability and prices, particularly timber and wood fibers, can impact production costs and supply stability. Environmental regulations related to forestry management and logging activities may also affect raw material sourcing. In addition, concerns regarding formaldehyde emissions from adhesives used in some engineered wood products may limit adoption in certain regions with strict environmental standards. Competition from alternative construction materials such as steel, concrete, and plastic composites can also pose challenges to market growth.

Opportunities

The engineered wood market presents significant opportunities driven by innovation, sustainability initiatives, and expanding construction activities worldwide. Increasing adoption of mass timber construction and advanced structural wood products in multi-story buildings is creating new growth avenues for manufacturers. Sustainable building certifications and green construction standards are encouraging the use of engineered wood as a renewable and carbon-efficient material.

Emerging economies with rapidly growing urban populations and infrastructure development projects offer substantial market potential. Furthermore, investments in research and development, improved manufacturing technologies, and strategic collaborations among industry players are expected to strengthen production capabilities and expand global distribution networks. As sustainability and efficiency remain key priorities in the construction industry, the engineered wood market is projected to experience steady growth between 2024 and 2033.

Segmental Overview

The Engineered wood market is segmented on the basis of type, application, end-user industry, and region. Depending on type, the market is segregated into particle board, plywood, medium density fiberboard (MDF), cross laminated timber (CLT), laminated veneer lumber, oriented strand board, and glue laminated timber. By application, it is categorized into construction, flooring, furniture, transport, packaging, and others. By end user industry, it is bifurcated into residential, and non-residential. By region, it is analyzed across North America, Europe, Asia-Pacific, Latin America and Middle East & Africa.

By type, the plywood segment accounted for the largest share of market revenue in 2023. Its dominance is attributed to its high strength, durability, and wide range of applications in construction and furniture manufacturing. Meanwhile, the medium-density fiberboard (MDF) segment is expected to register the highest CAGR during the forecast period. The growth of MDF is largely driven by its cost-effectiveness, increasing use in furniture and interior applications, and ongoing improvements in manufacturing technologies that enhance product quality and performance.

By application, the construction segment held the largest market share in 2023. This is primarily due to the significant demand for engineered wood products such as beams, panels, and structural components used in residential and commercial building projects. The growing focus on sustainable building materials and the expansion of global infrastructure development have further strengthened the adoption of engineered wood in construction activities. On the other hand, the furniture segment is projected to witness the fastest growth during the forecast period.

By end-user industry, the residential segment accounted for the largest share of the engineered wood market in 2023. The growing demand for housing and residential infrastructure has significantly increased the use of engineered wood materials in construction projects. Additionally, the residential segment is anticipated to grow at the highest CAGR during the forecast period. Increasing urbanization, rising disposable incomes, and a growing preference for sustainable and cost-effective construction materials are major factors supporting this growth.

By region, Asia-Pacific held the highest engineered wood market share in 2023, primarily due to the rapid urbanization, industrial growth, and increasing construction activities in countries like China, India, and Southeast Asia. The region's large population, coupled with a growing demand for affordable housing and infrastructure projects, has significantly driven the consumption of engineered wood products. Moreover, Asia-Pacific is expected to grow with a higher CAGR during the forecast period. The region strong economic growth, expanding real estate sector, and increasing awareness of sustainable building materials are key factors driving this growth. Additionally, government initiatives supporting eco-friendly construction and urban development further bolster the demand for engineered wood in the region.

Regional Market Outlook

Asia-Pacific dominated the engineered wood market in 2023. Rapid urbanization, industrial expansion, and increasing construction activities in countries such as China, India, and several Southeast Asian nations have significantly boosted the demand for engineered wood products in the region. Furthermore, Asia-Pacific is expected to register the highest CAGR during the forecast period. Strong economic growth, a rapidly expanding real estate sector, and increasing awareness of environmentally sustainable construction materials are key factors contributing to the region’s continued market growth. Government initiatives promoting green construction and urban infrastructure development are also supporting the rising adoption of engineered wood products across the region.

Engineered Wood Market Value Chain Analysis

The engineered wood market value chain begins with the sourcing of raw materials such as timber, wood chips, veneers, and wood fibers. Forestry companies and timber suppliers play a crucial role in providing logs that are harvested from sustainably managed forests or plantations. These raw materials are transported to processing facilities where they are converted into veneers, strands, particles, or fibers depending on the type of engineered wood product being manufactured. Chemical suppliers also contribute to the value chain by providing adhesives, resins, and bonding agents used to bind wood components together and improve durability and performance.

Manufacturers then process these materials using advanced production techniques such as drying, layering, pressing, and curing to produce engineered wood products including plywood, medium-density fiberboard (MDF), oriented strand board (OSB), laminated veneer lumber (LVL), cross-laminated timber (CLT), and glue-laminated timber (glulam). These products are designed to offer improved strength, dimensional stability, and efficient use of wood resources compared to traditional solid wood. Equipment suppliers support the production process by providing automated cutting systems, pressing machines, and finishing technologies that ensure consistent product quality and efficient manufacturing.

After production, engineered wood products are distributed through wholesalers, distributors, and logistics providers. These intermediaries manage storage, transportation, and delivery to construction companies, furniture manufacturers, retailers, and other end users. Retail outlets, home improvement stores, and online platforms also play a role in making engineered wood products accessible to consumers and businesses.

Which consumer segments are contributing significantly to the growth of the engineered wood market?

The expansion of the engineered wood market is largely driven by construction companies, furniture manufacturers, real estate developers, and residential consumers. Construction firms and infrastructure developers are major consumers of engineered wood products, as these materials are widely used in structural components such as beams, panels, and framing systems. The growing adoption of engineered wood in large-scale construction projects and sustainable building initiatives has significantly increased demand from this sector.

Furniture manufacturers also represent an important consumer group, utilizing engineered wood products such as MDF, particle board, and plywood to produce cabinets, wardrobes, office furniture, and decorative interior elements. Residential consumers contribute to market growth through home renovation, interior design, and do-it-yourself (DIY) projects that involve engineered wood materials.

What key trends are currently influencing the engineered wood industry?

A major trend shaping the engineered wood market is the increasing emphasis on sustainable construction and environmentally responsible materials. Engineered wood products are gaining popularity as they allow efficient utilization of timber resources and support green building initiatives. Another important trend is the growing adoption of mass timber construction techniques, including cross-laminated timber (CLT), which enables the development of multi-story wooden buildings while reducing carbon emissions compared to traditional construction materials.

Additionally, rising demand for prefabricated and modular construction is boosting the use of engineered wood products due to their dimensional stability and ease of installation.

How is technological advancement transforming the engineered wood market?

Technological advancements are playing a vital role in improving manufacturing efficiency, product performance, and sustainability in the engineered wood market. Automated production lines, high-pressure pressing technologies, and precision cutting systems enable manufacturers to produce engineered wood products with consistent quality and structural reliability. Advanced adhesive formulations and improved bonding techniques enhance the durability and moisture resistance of these products.

Digital technologies are also helping manufacturers optimize production planning, monitor supply chains, and maintain quality standards. Innovations in processing methods allow the use of smaller wood fibers, recycled materials, and wood residues, contributing to resource efficiency and reduced environmental impact.

What innovations are strengthening the growth of the engineered wood market?

Innovation in the engineered wood market is largely focused on developing advanced structural wood products, improving sustainability, and expanding application areas. Products such as cross-laminated timber, laminated veneer lumber, and glue-laminated timber are increasingly being used in modern architectural and structural designs. These materials offer high strength-to-weight ratios and allow architects and engineers to construct complex and durable wooden structures.

In addition, manufacturers are introducing eco-friendly adhesives, low-emission boards, and recyclable materials to meet strict environmental regulations and green building standards. Improvements in surface finishing, decorative laminates, and design flexibility are also enhancing the aesthetic appeal of engineered wood products used in furniture and interior applications.

Competitive Landscape

The global engineered wood market consists of a combination of large multinational manufacturers, regional producers, and specialized wood processing companies. Key participants in the market include Boise Cascade Company, Celulosa Arauco y Constitución S.A., Huber Engineered Woods LLC, Louisiana-Pacific Corporation (LP), Norbord Inc., Patrick Industries, Inc., Raute Group, Shenzhen Risewell Industry Co., Ltd., Universal Forest Products, Inc., and Weyerhaeuser Company. These companies focus on expanding production capabilities, strengthening supply chains, and adopting sustainable forestry practices to maintain their competitive position in the market.

Market players are actively investing in advanced manufacturing technologies, product innovation, and sustainable material development to meet the increasing demand for high-performance engineered wood products across construction, furniture, and industrial applications.

Recent Development in the Engineered Wood Market

- In December 2022, Boise Cascade strengthened its distribution network through the acquisition of two significant land parcels: a 45-acre site in Walterboro, South Carolina, and a 34-acre property in Hondo, Texas. These acquisitions are intended to improve the company’s service capabilities and operational reach in key markets across South Carolina and Texas.

- In February 2021, West Fraser completed the acquisition of Norbord Inc., a leading manufacturer of engineered wood products such as OSB, MDF, and LVL. This strategic move expanded West Fraser’s production footprint across Canada and the southern U.S., enhancing its overall capacity and presence in the engineered wood market.

Key Benefits for Stakeholders

- The report offers a comprehensive analysis of both current and emerging trends and dynamics in the engineered wood market.

- A detailed market assessment has been conducted by developing estimations for key segments over the period from 2023 to 2033.

- The study includes an extensive evaluation of the engineered wood industry, focusing on product positioning and the strategic activities of leading competitors within the market.

- A regional analysis is provided to identify prevailing opportunities and growth prospects across different geographies.

- The report also presents a forecast of the engineered wood market from 2024 to 2033, highlighting expected trends and developments.

- Key market players are profiled in detail, and their strategies are analyzed to provide insights into the competitive landscape and overall market outlook of the engineered wood industry.

Engineered Wood Market Report Highlights

| Aspects | Details |

| Forecast period | 2023 - 2033 |

| Report Pages | 197 |

| By Application |

|

| By End User Industry |

|

| By Type |

|

| By Region |

|

| Key Market Players | Raute Group, Lamiwood™ Designer Floor, Boise Cascade Company, Louisiana-Pacific Corporation (LP), Huber Engineered Woods LLC, Universal Forest Products, Inc., PFEIFER GROUP, Celulosa Arauco Y Constitucion SA, Norbord Inc., Weyerhaeuser Company |

Analyst Review

The global engineered wood market is gaining popularity worldwide owing to its exquisite design, eco-friendly nature, greater wood strength, and molding capabilities. In addition, growth in awareness about the benefits of engineered wood, its technological advantage over other products, and rise in disposable income further boost the market growth.

Non-residential construction spendings gained impetus in 2015, leading to the growth of engineered wood usage in commercial buildings. In addition, new housing development and lodging further propelled the market growth, thereby highlighting the recovery in residential construction market. For instance, in 2014, mortgage rates declined in the U.S., thus leading to growth in new home sales.

The market is dominated by Europe and especially Western Europe and Scandinavian countries, such as Germany, Austria, Finland, Denmark and UK, owing to the widespread forest area coupled with rise in demand for engineered wood. Although, Brazil, Chile, and South Africa in LAMEA region possess huge growth potential owing to large untapped rainforest cover.

North America possesses second highest growth potential market due to vast forest availability, better technology and utilization of resources, and higher awareness among population. Major engineered wood companies are present in the U.S. and Canada.

Countries such as India, Japan, and China are anticipated to be major exporters to North American and European countries owing to the high raw wood production.

Market players, such as Weyerhaeuser and Arauco, have established retail outlets worldwide and have adopted latest technologies such as timberland LSL floor joists and easy pack to maintain their foothold. In addition, intensive marketing campaigns and attractive designs and product type by prominent companies have increased brand awareness in the global market among consumers, thus leading to the growth of the engineered wood market.

Increased use of engineered wood over other building materials, rise in reconstruction, renovation, and remodeling of old buildings, and surge in focus on affordable homes drive the growth of the global Engineered wood market.

The latest version of the Engineered wood market report can be obtained on demand from the website.

The Engineered wood market size was valued at $254.2 billion in 2023.

The Engineered wood market size is estimated to reach $427.2 million by 2032, exhibiting a CAGR of 5.3% from 2024 to 2033

The forecast period considered for the Engineered wood market is 2024 to 2033, wherein, 2023 is the base year, 2024 is the estimated year, and 2033 is the forecast year.

Plywood segment is the largest market for Engineered wood market.

The key players profiled in the report include Boise Cascade Company, Celulosa Arauco Y Constitucion SA, Huber Engineered Woods LLC, Louisiana-Pacific Corporation (LP), Norbord Inc., Patrick Industries, Inc., Raute Group, Shenzhen Risewell Industry Co., Ltd, Universal Forest Products, Inc., and Weyerhaeuser Company.

The report contains an exclusive company profile section, where leading companies in the market are profiled. These profiles typically cover company overview, geographical presence, market dominance (in terms of revenue and volume sales), various strategies, and recent developments.

Loading Table Of Content...

Loading Research Methodology...