Liquid Hydrogen Micro Bulking Systems Market Overview

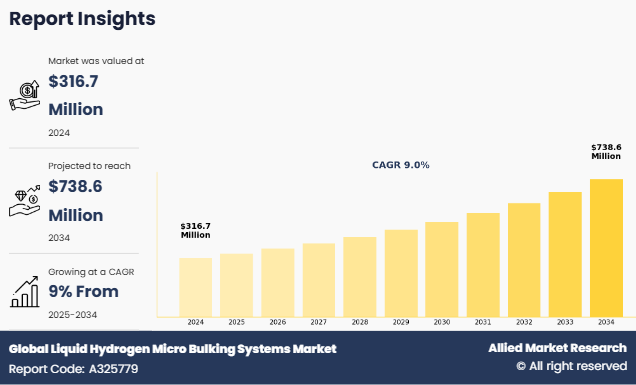

The global liquid hydrogen micro bulking systems market was valued at USD 316.7 million in 2024, and is projected to reach USD 738.6 million by 2034, growing at a CAGR of 9% from 2025 to 2034. The global liquid hydrogen micro bulking systems market is expanding rapidly due to rising demand for clean energy in aerospace, defense, and industrial sectors. Compact, efficient, and advanced cryogenic systems are enabling decentralized hydrogen storage and fueling, making them crucial for future-ready energy infrastructure and sustainable global decarbonization efforts.

Key Market Trend & Insights

- Vacuum insulated cryogenic tanks segment accounted for over one-fourth of market revenue in 2024.

- Industrial segment led the market in 2024 in terms of revenue.

- North America dominated the liquid hydrogen micro bulking systems market.

- Asia-Pacific projected to grow at the highest CAGR of 11.0% during the forecast period.

Market Size & Forecast

- 2034 Projected Market Size: USD 738.6 million

- 2024 Market Size: USD 316.7 million

- Compound Annual Growth Rate (CAGR) (2025-2034): 9%

Introduction

Liquid hydrogen micro bulking systems are essential components for mid-scale cryogenic hydrogen storage and delivery. These systems are designed for use in environments where large-scale bulk storage is impractical but where reliability, thermal insulation, and compact delivery are critical such as in space launches, portable power systems, remote industrial operations, and aerospace applications. These systems enable consistent handling of liquid hydrogen by maintaining extremely low temperatures and minimizing product losses through high-performance insulation and cryocooling technologies.

Key Takeaways

- Quantitative data in the report includes value forecasts ($Million), CAGR analysis, and segment-wise annual growth rates from 2025–2034.

- The study provides detailed qualitative insights, including market dynamics, key trends, restraints, and opportunities.

- Top players profiled include Chart Industries, GenH2, Cryostar, Inox India, Wessington Cryogenics, and others.

- The report serves as a valuable reference for space, energy, and industrial sectors, offering strategic direction based on current and emerging market forces.

Market Dynamics

The global liquid hydrogen micro bulking systems industry is being driven by multiple forces that reflect the increasing global momentum toward clean energy adoption and green hydrogen economy development. One of the primary drivers is the rising demand for sustainable hydrogen storage and distribution solutions, particularly in space and aerospace sectors, where liquid hydrogen is a preferred fuel due to its high energy density and clean combustion profile. Governments and private entities alike are increasing their investments in green hydrogen infrastructure, space exploration programs, and national hydrogen strategies, creating a robust foundation for market expansion. Additionally, technological advancements in cryogenic storage systems, such as vacuum-insulated tanks, cryocoolers, and advanced composite pressure vessels, are enhancing the efficiency, safety, and durability of liquid hydrogen storage. These innovations reduce hydrogen boil-off, enable more precise temperature control, and improve the operational flexibility of hydrogen systems in off-grid and mobile settings.

However, several challenges hinder the market’s growth. The high capital expenditure required for developing cryogenic infrastructure, as well as the complexity of engineering and safety protocols, act as significant restraints particularly for small- and medium-scale adopters. Moreover, the intermittency of hydrogen production and inconsistencies in liquid hydrogen supply chains pose logistical challenges for widespread commercial deployment. Despite these hurdles, the market is witnessing substantial opportunities. Increasing interest in hybrid and decentralized hydrogen refueling systems, especially for industrial and defense use, is paving the way for micro bulking systems. The integration of IoT-based monitoring, advanced insulation materials, and digital twin technologies into cryogenic systems promises to improve real-time tracking, system performance, and predictive maintenance catalyzing long-term liquid hydrogen micro bulking systems market growth.

Segment Overview

The liquid hydrogen micro bulking systems market forecast is segmented on the basis of technology, application, and region. By technology, the market is segmented into vacuum insulated cryogenic tanks, composite overwrapped pressure vessels (COPVs), cryocoolers, and others. By application, the market is divided into aerospace and space launch systems, stationary and portable energy systems, industrial, and others. Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

By Technology

In terms of technology, the vacuum insulated cryogenic tanks segment held the largest market share in 2024. These tanks are designed to safely store and transport liquid hydrogen at extremely low temperatures, while significantly minimizing hydrogen loss through boil-off. Their widespread use in aerospace, energy storage, and transportation systems makes them indispensable to the liquid hydrogen micro bulking systems industry. The segment's growth is further bolstered by continuous R&D in high-performance insulation materials and modular tank designs, which improve space utilization and portability.

Composite Overwrapped Pressure Vessels (COPVs) offer the benefit of being lightweight yet robust, which is vital for applications requiring mobility and compact system configurations, such as military and mobile refueling systems. Cryocoolers, on the other hand, are crucial in maintaining liquid hydrogen temperatures during prolonged storage, especially in space launch and stationary applications. The “others” category includes advanced vaporizer systems and hybrid technologies combining multiple storage methods.

By Application

From an application standpoint, industrial segment, particularly sectors like semiconductors, metallurgy, and glass production, is dominating the global market share also expected to grow steadily as hydrogen becomes a key decarbonization tool. Meanwhile, stationary and portable energy systems are gaining traction as hydrogen is increasingly being used as a clean backup power source. The aerospace and space launch systems continue to dominate the liquid hydrogen micro bulking systems market size, owing to the historic and ongoing reliance on liquid hydrogen as rocket fuel. The surge in private space enterprises and increased satellite launches globally further support this segment's dominance.

By Region

The regional landscape of the liquid hydrogen micro bulking system market reveals a diverse adoption pattern led by technology maturity, government support, and sector-specific demand. In 2024, North America emerged as the dominant in liquid hydrogen micro bulking systems market share and is expected to maintain its lead through 2034. This leadership is primarily due to the United States’ significant investments in hydrogen infrastructure, robust aerospace industry, and initiatives such as the U.S. Department of Energy’s Hydrogen Energy Earthshot, which aims to reduce the cost of clean hydrogen by 80% within a decade. The presence of leading players like Chart Industries, Plug Power, and Air Products ensures advanced technological adoption and capacity expansion within the region.

Europe follows closely, supported by the EU’s ambitious hydrogen strategy and strong investments in hydrogen mobility, aerospace decarbonization, and industrial clean energy transitions. Countries like Germany and France are making large-scale investments in hydrogen hubs, which require reliable liquid hydrogen storage systems like micro bulking units. Europe's focus on sustainability and circular economy further enhances the uptake of scalable, reusable storage systems.

However, Asia-Pacific is projected to exhibit the fastest growth during the forecast period. Nations like Japan, South Korea, China, and Australia are aggressively scaling up their green hydrogen production capabilities and associated transport infrastructure. Their focus on hydrogen-powered public transport, defense modernization, and portable power systems is contributing to a surging demand for micro bulking systems that support decentralized storage. Strategic alliances with Western hydrogen technology providers are helping them leapfrog traditional infrastructure barriers.

Lastly, LAMEA is witnessing a gradual uptake, particularly in hydrogen export projects from the Middle East and pilot projects in South Africa and Brazil. The potential for exporting liquid hydrogen to Europe and Asia from low-cost solar and wind-powered facilities in LAMEA could unlock significant regional market opportunities over the next decade.

Which are the Top Liquid Hydrogen Micro Bulking Systems companies

The following are the leading companies in the market. These players have adopted various strategies to increase their market penetration and strengthen their position in the liquid hydrogen micro bulking systems industry.

- Culligan International Company

- Kinetico UK Limited

- NuvoH2O, LLC.

- US Water Systems

- EcoWater

- IEI

- Hague Quality Water

- Harvey Water Softeners Ltd

- Pentair

- Canature

Key Benefits for Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the global liquid hydrogen micro bulking systems market analysis from 2024 to 2034 to identify the prevailing global liquid hydrogen micro bulking systems market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the global liquid hydrogen micro bulking systems market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global global liquid hydrogen micro bulking systems market trends, key players, market segments, application areas, and market growth strategies.

Liquid Hydrogen Micro Bulking Systems Market Report Highlights

| Aspects | Details |

| Market Size By 2034 | USD 738.6 million |

| Growth Rate | CAGR of 9% |

| Forecast period | 2024 - 2034 |

| Report Pages | 274 |

| By Application |

|

| By Technology |

|

| By Region |

|

| Key Market Players | Chart Industries, Inc., Steelhead Composites, Inc., CMB.TECH, Bluefors Cryogenics OY, Cryospain, INOX India Limited, Wessington Cryogenics Limited, Faber Industrie S.p.A., GENH2, Cryostar SAS, CIMC Enric Holdings Limited |

Analyst Review

According to industry CXOs, the liquid hydrogen micro bulking systems market is poised for remarkable growth in the coming years, driven by the global push toward clean energy transitions, rapid expansion of hydrogen-based applications, and rise in demand for decentralized and flexible hydrogen supply systems. CXOs recognize liquid hydrogen micro bulking systems as a critical enabler of the hydrogen economy, providing safe, efficient, and scalable storage and distribution solutions that bridge the gap between centralized production facilities and diverse end-use applications across industries, mobility, aerospace, defense, and energy sectors.

CXOs emphasize that industries such as aerospace, heavy-duty transport, steel, chemicals, and power generation are turning toward liquid hydrogen as a viable alternative to fossil fuels, necessitating advanced micro bulking systems to ensure safe and reliable handling, storage, and fueling capabilities. In addition, rise in adoption of liquid hydrogen in space exploration, defense operations, and critical infrastructure further underscores the strategic importance of investing in robust, mobile, and high-efficiency liquid hydrogen micro bulking solutions.

CXOs highlight that the scalability, portability, and modularity of liquid hydrogen micro bulking systems provide significant competitive advantages, enabling industries and operators to integrate hydrogen into their operations without large-scale infrastructure investments. The flexibility to deploy these systems in off-grid, remote, or temporary locations enhances energy security, disaster resilience, and operational continuity, which are important considerations in today’s dynamic geopolitical and environmental landscape. Furthermore, the ongoing expansion of hydrogen refueling infrastructure, especially for hydrogen-powered vehicles, drones, marine vessels, and aviation, is opening new avenues for liquid hydrogen micro bulking systems to serve as mobile and decentralized fueling solutions, supporting last-mile delivery and enabling the development of hydrogen corridors and clean logistics hubs.

However, CXOs also acknowledge the challenges such as high capital costs, technical complexities, and stringent regulatory requirements associated with cryogenic hydrogen handling in the market. Addressing these challenges require continued investments in research and development, innovation in insulation materials, smart monitoring systems, and automation technologies to enhance system performance, safety, and affordability. CXOs view strategic partnerships between technology providers, hydrogen producers, transportation operators, and policymakers as essential to fostering innovation, scaling up deployment, and overcoming market barriers.

CXOs also emphasize the need to align the development of liquid hydrogen micro bulking systems with global sustainability objectives, such as circular economy practices, energy transition plans, and efforts to combat climate change. Companies that position themselves as leaders in providing safe, efficient, and environmentally responsible liquid hydrogen micro bulking solutions are expected to gain significant market traction and secure long-term growth opportunities. CXOs believe that by prioritizing technological innovation, cost efficiency, customer-focused offerings, and strong commitment to sustainability, the liquid hydrogen micro bulking systems industry is strategically poised to become a key driver in the global hydrogen economy and the wider transition to clean energy.

The market was valued at $316.7 million in 2024 and is expected to reach $738.6 million by 2034, growing at a CAGR of 9.0%.

Key trends include the rise of IoT-enabled monitoring, decentralized hydrogen delivery, hybrid liquid-gas systems, and innovations in insulation and compact tank design.

Aerospace and space launch systems dominate due to liquid hydrogen’s efficiency as rocket fuel and increasing space missions.

North America leads the market, driven by strong aerospace activity, hydrogen policy support, and advanced cryogenic infrastructure in the U.S.

Major players include Chart Industries, GenH2, Cryostar, Inox India, Faber Industrie, and CIMC Enric, among others.

Loading Table Of Content...

Loading Research Methodology...