Hybrid Cloud Market Overview

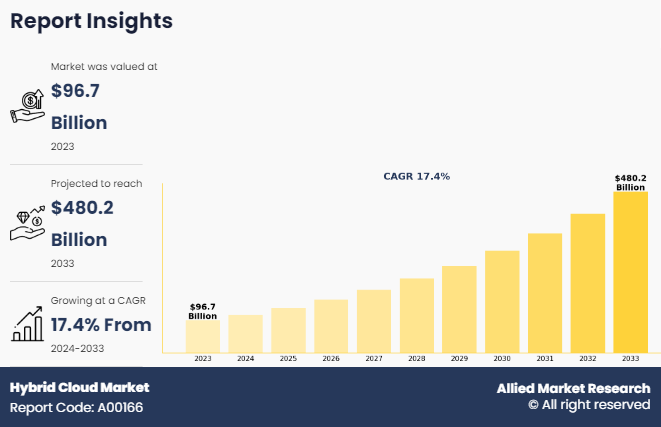

The global hybrid cloud market size was valued at USD 96.7 billion in 2023, and is projected to reach USD 480.2 billion by 2033, growing at a CAGR of 17.4% from 2024 to 2033.

Factors such as increase in availability of cloud-based services, increase in the adoption of advanced technologies, and growth in usage of mobile devices positively impacted the growth of the market. However, the cost and budget constraints and inability to integrate with internal systems are expected to hamper the growth of the global market. Moreover, rise in the adoption of Industry 4.0 to enable real-time processing of data and reduce latency and the adoption of cloud computing to enable scalability, flexibility, and cost-effectiveness of hybrid cloud solutions are also anticipated to create lucrative opportunities for hybrid cloud market growth.

Introduction

A hybrid cloud, sometimes called a cloud hybrid, is a computing environment that combines an on-premises data center (also called a private cloud) with a public cloud, allowing data and applications to be shared between different clouds. Hybrid cloud architecture is sometimes defined as "multi-cloud" structures, in which a company employs many public clouds in addition to its on-premises data center. While less sensitive data can be kept in the cloud, several regulated sectors require that specific types of data be kept on-site. By using this type of hybrid cloud architecture, businesses can continue to fulfill industry standards while gaining the flexibility of the public cloud for less regulated computing operations.

Furthermore, the integration of advanced technologies has the potential to create several benefits for businesses and consumers. Hybrid cloud solutions can help improve efficiency and productivity for businesses, as well as reduce costs. Moreover, it can provide enhanced convenience and a better data storage experience for consumers. In addition, the use of technologies in conjunction with IoT can help to improve hybrid cloud solutions, as well as provide businesses with a better understanding of their products. Such enhanced factors are expected to provide lucrative opportunities for market growth during the forecast period.

The report focuses on growth prospects, restraints, and trends of the Hybrid cloud market analysis. The study provides Porter’s five forces analysis to understand the impact of various factors, such as bargaining power of suppliers, competitive intensity of competitors, threat of new entrants, threat of substitutes, and bargaining power of buyers, on the Hybrid cloud market.

Key Findings

By component, the solution segment accounted for the largest Linux software market share in 2023.

By service model, the SaaS segment accounted for the largest Linux software market share in 2023.

By enterprise size, the large enterprises segment accounted for the largest Linux software market share in 2023.

By industry vertical, the BFSI segment accounted for the largest Linux software market share in 2023.

Region wise, Asia-Pacific generated the highest revenue in 2023.

Segment Review

The hybrid cloud market size is segmented into component, enterprise size, service model, industry vertical, and region. On the basis of component, the market is divided into solutions and services. On the basis of enterprise size, the market is bifurcated into large enterprises and small and medium-sized enterprises. On the service model, the market is divided into software as a service (SaaS), infrastructure as a service (IaaS), and platform as a service (PaaS). On the basis of industry vertical, the market is divided into IT & telecom, healthcare, BFSI, retail, government, media & entertainment, transportation & logistics, manufacturing, and others. Region wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

On the basis of component, the hybrid cloud industry is divided into solution and services. In 2023, the solution segment dominated the market in terms of revenue, reflecting strong demand for integrated cloud solutions that allow businesses to leverage both private and public cloud environments effectively. Moreover, the services segment is projected to attain the highest CAGR during the forecast period. This anticipated growth is driven by an increasing reliance on managed services, consulting, and support to navigate complex hybrid cloud architectures.

By region, North America dominated the market share in 2023 for the hybrid cloud market. The presence of technological businesses is insistently influencing the advancement of the hybrid cloud market. Moreover, the expansion of advanced technologies such as IoT, cloud computing, and others, further contribute to the growth of the global market.

Key Market Players

The market players operating in the hybrid cloud market share are Amazon Web Services, Inc., Alphabet Inc. (Google LLC), IBM Corporation, SAP SE, Teradata, Alibaba, Tencent Holdings Limited, Broadcom, Inc., Microsoft Corporation, Oracle Corporation, Cisco System Inc., Dell Technologies, Hewlett Packard Enterprise Company, Tata Consultancy Services (TCS), NTT Communications Corporation, Atos SE, Huawei Technologies Co. Ltd., Fujitsu Ltd, T-Systems International GmbH and Telstra Group Limited. These major players have adopted various key development strategies such as business expansion, new product launches, partnerships, among others, which help to drive the growth of the hybrid cloud market globally.

Top Impacting Factors

Increase in availability of cloud-based services

The surge in the expansion of hybrid cloud services is a key driver for the growth of the global market. Cloud computing provides the underlying infrastructure and resources needed to deliver digitalization to end-users, making it an essential enabler for businesses. This is attributed to the rising number of countries committing to adopt hybrid cloud solutions. Further, government policies are undertaking increased initiatives to embrace advanced technology, with plans for integrating a new digital solution. For instance, in April 2023, the Japanese government raised $31.7 million in funding to develop shared quantum computing using a business-friendly cloud platform. The Japanese government intends to broaden quantum computing's accessibility so that businesses may take advantage of its benefits. Therefore, hybrid cloud solutions gained wider traction among end-users, taking advantage of cloud computing solutions in several industries.

Moreover, hybrid cloud solutions leverage the economies of scale provided by cloud computing. Organizations may avoid the upfront costs associated with purchasing and maintaining on-premises hardware infrastructure. Consequently, regional governments and private and public businesses invest in hybrid cloud solutions. For instance, in April 2023, Ericsson partnered with the Government of Canada to raise $352.40 million in funding to enhance the presence of the global leaders in advanced 5G, 6G, AI, cloud RAN, and core network technologies. Such investments and advancements in hybrid cloud solutions are expected to eventually contribute to the growth of the global market.

Increase in the adoption of advanced technologies

The growth in demand for advanced technologies and efficient operations is a significant driver of the hybrid cloud market. Technologies include using IoT devices and AI technology to automate processes and operations in businesses such as manufacturing, logistics, and agriculture. Hence, by automating processes and operations, businesses can improve efficiency, reduce costs, and enhance productivity. Moreover, these advanced technologies enable more accurate data analysis, predictive modeling, and process automation, allowing organizations to streamline data storage activities and improve efficiency across several industries. Such factors are further expected to significantly contribute to the huge potential for the growth of the hybrid cloud market.

In addition, the implementation of AI and cloud technologies helps in determining specific inefficiencies and avoiding them by simulating business processes in different scenarios. It also prevents the anticipated process inefficiency through predictive simulation. Hence, several companies and government authorities are leveraging advanced technologies intending to improve business operations. For instance, in April 2024, AVEVA expanded CONNECT, its leading industrial intelligence platform with data and visualization services for hybrid Manufacturing Execution System (MES) solutions. AVEVA’s new hybrid MES solution enables manufacturing companies to manage production data in the cloud, to improve supply chain agility with enterprise-wide visibility into distributed plant operations. Therefore, such initiatives are expected to further accelerate the use of technologies, which play a significant role in the continued growth of the hybrid cloud market.

Growth in usage of mobile devices

The increasing adoption of the internet and mobile devices propels growth opportunities for the global hybrid cloud market. The growing connectivity and proliferation of mobile devices have created a demand for advanced technological services, which in turn has surged the demand for hybrid cloud solutions among end users. The growing adoption of the internet and mobile devices enables organizations to increase their hybrid cloud solution implementation. Cloud-based AI solutions allow users to access applications, and data securely from their own devices. This flexibility empowers organizations to support a business operation efficiently, improving productivity and work-life balance. These aforementioned factors are significantly contributing to the huge potential for the growth and development of the hybrid cloud market.

In addition, the emerging trend of mobile devices has fueled the bring your own device (BYOD) trend. In corporate organizations, hybrid cloud solutions accommodate BYOD policies by enabling users to access virtual desktops and corporate resources securely from their personal devices. This reduces the need for organizations to provide company-owned devices, thereby saving costs and increasing employee satisfaction. It also increases the quality of life of the entire organization by responding to the comprehensive challenges of sustainability. Thus, the public and private sectors are increasingly using and implementing hybrid cloud solutions. For instance, in October 2024, Zoom Video Communications launched its cloud phone solution, Zoom Phone, in India, starting with the Maharashtra Telecom Circle (Pune). This service is a significant milestone as it is the country's first licensed cloud private branch exchange (PBX) service, approved by the Department of Telecommunications (DoT). Therefore, such development strategies further pave the way for the deployment of hybrid cloud, which eventually drives market growth.

Recent Developments in the Hybrid Cloud Industry

In June 2024, the Department of Telecommunications (DoT) launched a new initiative aimed at aiding medium, small, and micro enterprises (MSMEs) and startups through the adoption of industry-emerging technologies.

In March 2024, Tackle.io launched an expansion of its capabilities to operationalize and scale sales transaction workflows for independent software vendors (ISVs) selling through Google Cloud Marketplace. This strategic initiative further helps in propelling the solution segment in the global hybrid cloud market.

Key Benefits for Stakeholders:

This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the hybrid cloud market forecast from 2023 to 2032 to identify the prevailing market opportunities.

Market research is offered along with information related to key drivers, restraints, and opportunities of the hybrid cloud market outlook.

Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders to make profit-oriented business decisions and strengthen their supplier-buyer network.

In-depth analysis of the hybrid cloud industry segmentation assists in determining the prevailing Hybrid cloud market opportunity.

Major countries in each region are mapped according to their revenue contribution to the global market.

Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

The report includes an analysis of the regional as well as global Hybrid cloud market trends, key players, market segments, application areas, and market growth strategies.

Hybrid Cloud Market Report Highlights

| Aspects | Details |

| Forecast period | 2023 - 2033 |

| Report Pages | 427 |

| By Service Model |

|

| By Enterprise Size |

|

| By Industry Vertical |

|

| By Component |

|

| By Region |

|

| Key Market Players | Amazon Web Services, Inc., Broadcom Inc., Hewlett Packard Enterprise Company, Microsoft Corporation, Fujitsu Ltd., Teradata, Alibaba Group Holding, Telstra Group Limited, Tata Consultancy Services Limited, Dell Technologies Inc., Oracle Corporation, Tencent Holdings Limited, SAP SE, Cisco System Inc., Atos SE, IBM Corporation, NTT Communications Corporation, T-Systems International GmbH, Huawei Technologies Co. Ltd., Google LLC (Alphabet Inc.) |

Analyst Review

As the hybrid cloud software industry continues to evolve, CXOs are evaluating the opportunities and challenges regarding this emerging technology. The hybrid cloud software industry has grown rapidly in response to the massive amounts of data generated by Internet of Things (IoT) devices, and the need for AI-powered analytics and decision-making. Businesses are considering the benefits that hybrid cloud software can offer, such as the ability to provide a unified and scalable solution for managing and processing the data, enabling real-time insights and decision-making. In addition, next-generation digital businesses are leveraging cloud capabilities and preparing for a future of integrated solutions. These include vendor selection, migration tactics, process optimization, cloud security, multi-cloud environments, hybrid & digital infrastructures, data center outsourcing strategies, cloud optimization, cloud computing, PaaS, IaaS, SaaS, and others. Such factors are expected to provide lucrative opportunities for market growth during the forecast period.

However, businesses also recognize the challenges associated with hybrid cloud software. One significant challenge is the industry's fragmentation, with multiple vendors offering different solutions and technologies, which can make it challenging for organizations to select the right platform for their needs. In addition, hybrid cloud software requires significant investment in infrastructure, data analytics capabilities, and talent, which can be a barrier to entry for small and medium-sized enterprises (SMEs).

Furthermore, ethical and regulatory concerns related to data privacy and security are expected to hamper the growth of global hybrid cloud market growth, as hybrid cloud involves storing and processing data across both public and private infrastructures. Businesses must evaluate the services based on their industry-specific needs and requirements, including factors such as real-time monitoring and process optimization in almost every sector.

By addressing these challenges, businesses can unlock the full potential of hybrid cloud solutions to transform their operations, create value, and gain a competitive advantage in this industry. For instance, in October 2024, Sify Technologies launched a GPU cloud offering, which gives users access to GPUs on a pay-as-you-go basis, designed to support workloads such as machine learning, artificial intelligence (AI), deep learning, and rendering.

The hybrid cloud market is experiencing rapid growth, driven by an increasing demand for flexible, scalable IT solutions that bridge on-premises infrastructure with public and private cloud resources.

The solution is the leading component of the Hybrid Cloud Market.

North America is the largest regional market for Hybrid Cloud in 2023.

$480.2 billion is the estimated industry size of Hybrid Cloud in 2032.

Amazon Web Services, Inc., Alphabet Inc. (Google LLC), IBM Corporation, SAP SE, Teradata, Alibaba, Tencent Holdings Limited, Broadcom, Inc., Microsoft Corporation, Oracle Corporation, Cisco System Inc., Dell Technologies, Hewlett Packard Enterprise Company, Tata Consultancy Services (TCS), NTT Communications Corporation, Atos SE, Huawei Technologies Co. Ltd., Fujitsu Ltd, T-Systems International GmbH, and Telstra Group Limited. are the top companies to hold the market share in Hybrid Cloud.

Loading Table Of Content...

Loading Research Methodology...