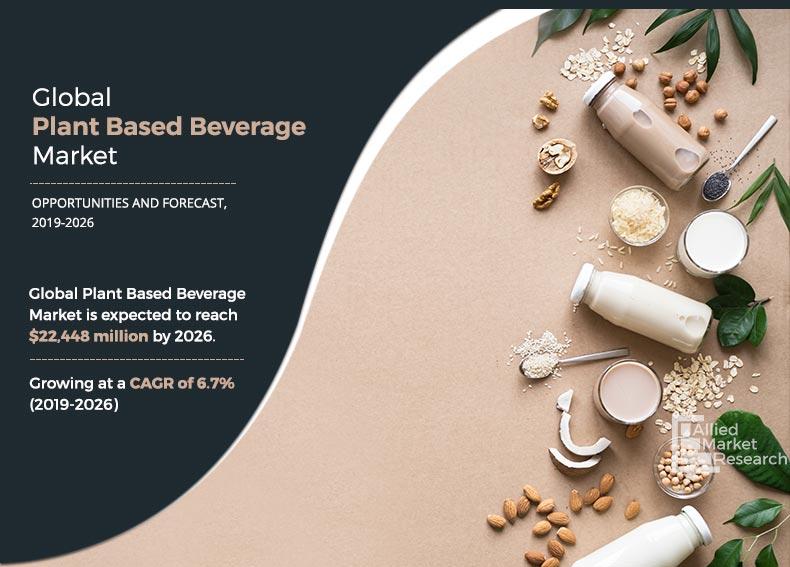

The plant-based beverage market size was valued at $13,560 million in 2018, and is estimated to reach $22,448 million by 2026, registering a CAGR of 6.7% from 2019 to 2026.

Plant-based beverage are drinks that can be used as a substitute for dairy. These beverages are derived from plants and are considered a very healthy alternative to dairy. Soymilk, rice milk, and almond milk are among the most popular choice for plant-based beverages worldwide. They are considered healthy, owing to presence of several essential vitamins and minerals. They are also low on fats, cholesterol, and has zero concentration of lactose.

Plant-based beverage has been very popular in the mature and emerging market. This can be attributed to rise in the number of people allergic to dairy. Furthermore, growth in health awareness and increase in disposable income fuel the growth of the plant-based beverage market. Moreover, introduction of additional healthy ingredients by different market players are some other factors that further drive the growth of the market. However, fluctuating prices of raw materials and high cost act as the major restraint for this market. On the contrary, growth in demand for plant-based beverage by vegan population and introduction of new flavor & variety of plant-based beverages are anticipated to provide lucrative growth opportunities for the plant-based beverage market.

The plant-based beverage market is segmented on the basis of source, type, distribution channel, and region. By source, the market is divided into fruits, nuts, rice, soy, and others. On the basis of type, it is fragmented into RTD tea & coffee, plant-based milk, and juices. By distribution channel, it is categorized into hypermarkets & supermarkets, convenience stores, specialty stores, and online. Regionally, the plant-based beverage market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

By Source

Nuts segment would exhibit the highest CAGR of 8.1% during 2019-2026.

Based on source, the fruits segment generated the highest revenue in 2018 and is expected to remain dominant throughout the forecast period. This can be attributed to increase in demand for products with high vitamins, zinc, and iron for proper body health, in countries such as India and China. Moreover, increase in penetration of high nutrition and cholesterol-free plant-based beverage products is expected to boost the demand for nuts-based beverage in the countries such as the U.S. However, the nuts segment is expected to grow at the highest CAGR throughout the forecast period, owing to better taste, low cholesterol, and low fat coupled with increase in demand for cholesterol-free products by consumers in countries such as Canada is expected to unfold attractive opportunities for the plant-based beverage market.

By Type

RTD Tea and Coffee segment would exhibit the highest CAGR of 9.9% during 2019-2026.

By type, the plant-based milk was the most prominent segment accounting for maximum share in the global market. This can be attributed to increase in demand for plant-based chemical-free milk by lactose intolerant population. However, the plant-based milk segment is expected to witness notable growth, with a CAGR of 5.8% from 2019–2026.

By Distribution Channel

Online segment would exhibit the highest CAGR of 9.1% during 2019-2026.

Based on the distribution channel, the speciality stores segment was the leading distribution channel with most of the plant-based beverage market share in 2018. The growth in the market can be attributed to increase in adoption of large retail formats such as supermarket and hypermarkets in both the mature and emerging markets. Moreover, the one stop solution provided by these retail formats makes it a very popular option for shopping for consumers. However, the online segment is expected to witness the fastest growth throughout the forecast period, owing to rapid internet and smartphone penetration.

By Region

North America would exhibit the highest CAGR of 4.3% during 2019-2026.

By region, North America was the most prominent regional market in 2018. This can be attributed to increase in trend of veganism and rise in consumers’ awareness regarding health and fitness in the region.

The players in the plant-based beverage industry have adopted product launch and acquisition as their key development strategy to increase profitability and improve stance in the dairy alternatives market. The key players have also relied on business expansion to stay relevant in the global market. The key players profiled in the report include WhiteWave Foods Company, Blue Diamond Growers, SunOpta Inc., Earth’s Own Food Inc., Living Harvest Foods Inc., Kikkoman Corporation, Rebel Kitchen, Organic Valley, Panos Brands LLC, The Hain Celestial Group Inc., and Eden Foods Inc.

Key Benefits for Stakeholders:

- The report provides a quantitative analysis of the current dairy alternatives market trends, estimations, and dynamics of the market size from 2018 to 2026 to identify the prevailing opportunities.

- Porter’s five forces analysis highlights the potency of the buyers and suppliers to enable stakeholders to make profit-oriented business decisions and strengthen their supplier–buyer network.

- In-depth analysis and the market size and segmentation assists in determining the prevailing plant-based beverage market opportunities.

- The major countries in each region are mapped according to their revenue contribution to the global market.

- The market player positioning segment facilitates benchmarking and provides a clear understanding of the present position of the market players in the industry.

Plant-Based Beverage Market Report Highlights

| Aspects | Details |

| By Source |

|

| By Type |

|

| By Distribution Channel |

|

| By Region |

|

| Key Market Players | ORGANIC VALLEY CROPP COOPERATIVE, PANOS BRANDS LLC (KONINKLIJKE WESSANEN N.V.), Archer Daniels Midland Company, Pepsico, Inc., SUNOPTA INC., BLUE DIAMOND GROWERS, The Coca-Cola Company, WHITEWAVE FOODS COMPANY INC. (DANONE), HAIN CELESTIAL GROUP, INC., LIVING HARVEST FOODS INC. |

Analyst Review

Over the past few years, the plant-based beverage market has witnessed a notable growth. The developing countries such as India and China have witnessed an increase in demand for these beverages. Furthermore, rise in demand for innovative products with vegan addition is an important factor that boost the growth of the global plant-based beverage market. Moreover, increase in demand for energy drinks is one of the major factors for expansion of this market in countries such as Brazil and Africa.

The almond milk is the fastest growing segment, followed by other sources such as coconut, hemp, oat, cashew nut, and hemp milk. The others segment is expected to face prominent growth in the global market, owing to consumers’ movement toward product with a new taste and a different flavor.

Leading companies in the plant-based beverages market such as WhiteWave Foods Company, Sunopta Inc., and Hain Celestial Group have witnessed a significant growth in the past few years. Wide varieties of food and beverage products, launched by these players, have increased their overall consumer base. Moreover, other players operating in the market such as Panos Brands LLC, Living Harvest Foods Inc, Pascual Group, and others are expected to strengthen their product line with higher quality innovative products to meet the increase in demands of the consumers. Players operating in the plant-based beverages market have focused on the development and launch of high-quality products, depending on the needs and preferences of consumers. They are regularly engaged in manufacturing of differentiated products with new taste, formulation, and flavor. Moreover, innovative marketing and positioning strategies of players have helped increase the overall market size.

The plant-based beverage market size was valued at $13,560 million in 2018, and is estimated to reach $22,448 million by 2026

The global Plant-Based Beverage market is projected to grow at a compound annual growth rate of 6.7% $22,448 million by 2026

PANOS BRANDS LLC (KONINKLIJKE WESSANEN N.V.), Archer Daniels Midland Company, ORGANIC VALLEY CROPP COOPERATIVE, The Coca-Cola Company, BLUE DIAMOND GROWERS, Pepsico, Inc., HAIN CELESTIAL GROUP, INC., LIVING HARVEST FOODS INC., SUNOPTA INC., WHITEWAVE FOODS COMPANY INC. (DANONE)

North America would exhibit the highest CAGR

Surge in demand for plant-based milk, increase in disposable income, and rise in vegan population propel the growth of the global plant-based beverage market.

Loading Table Of Content...