Staple Food Market Summary

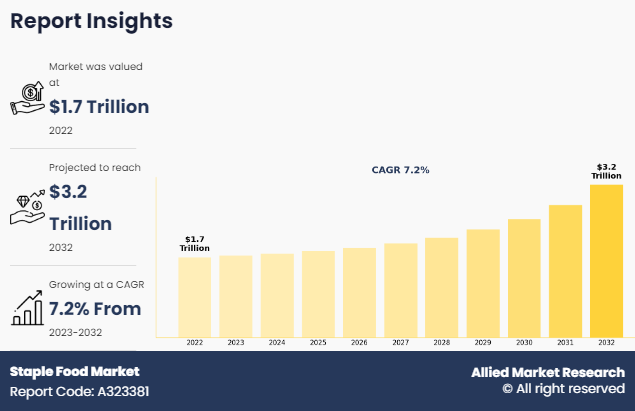

The global staple food market size was valued at $1.7 trillion in 2022, and is projected to reach $3.2 trillion by 2032, growing at a CAGR of 7.2% from 2023 to 2032.

Key Market Trends and Insights

Region wise, Asia-Pacific generated the highest revenue in 2022.

The global staple food market share was dominated by the cereals segment in 2022 and is expected to maintain its dominance in the upcoming years

The wholesale distributors segment is expected to witness the highest growth during the forecast

Market Size & Forecast

- 2022 Market Size: USD 1.7 Trillion

- 2032 Projected Market Size: USD 3.2 Trillion

- Compound Annual Growth Rate (CAGR) (2023-2032): 7.2%

- Asia-Pacific: Generated the highest revenue in 2022

Market Dynamics

A food staple is a food that makes up the dominant part of a population’s diet. Food staples vary from place to place, depending on the food sources available. Most food staples are inexpensive, plant-based foods. They are usually full of calories for energy.

Cereal grains and tubers are the most common food staples. There are more than 50,000 edible plants in the world, but just 15 of them provide 90% of the world’s food energy intake. Rice, corn (maize), and wheat make up two-thirds of this. Other food staples include millet and sorghum; tubers such as potatoes, cassava, yams, and taro; and animal products such as meat, fish, and dairy.

Innovations in agricultural technology, such as precision farming, genetic engineering, and advanced irrigation systems, drive efficiency and productivity in staple food production. This leads to higher yields and greater resilience against environmental factors. Government policies, including subsidies, agricultural incentives, and trade agreements, play a crucial role in supporting the staple food market.

Policies aimed at ensuring food security boost production and stabilize markets. The impact of climate change and environmental sustainability concerns affect the production of staple foods. Favorable weather conditions lead to increased production, while adverse conditions may disrupt the market, driving the need for adaptation and resilience. These factors are anticipated to drive the staple food market growth.

Adverse climate conditions, such as droughts, floods, or unpredictable weather patterns, significantly impact staple food production. Climate change poses a major restraint by affecting crop yields and increasing the risk of food insecurity. Disruptions in the supply chain, such as transportation issues, labor shortages, or infrastructure damage, create challenges for distributing staple foods. These disruptions lead to higher costs and reduced availability of staple diet foods.

Government regulations, food safety standards, and trade policies act as restraints in the market. Compliance with strict regulations may require additional resources, impacting the cost and efficiency of staple food production and distribution. These factors are anticipated to restrain the staple food industry growth.

The rise of e-commerce provides significant opportunities for the staple food market. As consumers increasingly turn to online shopping for convenience and safety, online retailers are expanding their offerings of staple foods. This creates new distribution channels and opens the market to a broader audience. The plant-based food trend continues to gain traction, driving demand for staple foods like lentils, legumes, and whole grains. This trend offers opportunities for developing new plant-based products and attracting health-conscious consumers seeking alternatives to animal-based proteins.

Consumers are becoming more environmentally conscious, leading to increased demand for sustainably sourced and organic staple foods. This trend presents opportunities for producers and retailers to differentiate their products through sustainability certifications and environmentally friendly practices. These factors are anticipated to drive the staple food market opportunities in the coming years.

Segments Overview

The staple food market is segmented on the basis of product type, nature and distribution channel and region. By product type, the market is sub-segmented into cereals, sugar, roots & tuber, fruit, vegetables, oil, and others. By nature, the market is classified into organic and conventional. By distribution channel, the market is classified into direct-to-consumer (d2c), retail stores, wholesale distributors, online retailers, and others. By region, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

By Product Type

The cereals sub-segment dominated the market in 2022. Consumers are increasingly seeking healthier options, boosting the popularity of whole grains like oats, quinoa, and brown rice. This trend drives demand for cereals that are less processed and have higher nutritional value. Advancements in agricultural technology are resulting in improved seeds, sustainable practices, and efficient irrigation, affecting cereal production, leading to changes in availability and cost. Changes in climate impact cereal production, affecting crop yields and potentially lead to fluctuations in supply.

By Nature

The conventional sub-segment dominated the global market share in 2022. Conventional staple foods are the foundational elements in global diets, typically referring to widely consumed and traditionally grown food items such as rice, wheat, corn, potatoes, and legumes. The driving factors behind the demand and production of these conventional staples are influenced by a complex interplay of social, economic, environmental, and cultural elements. Many conventional staple foods are deeply rooted in cultural and traditional practices. These foods are often central to the cuisine and identity of various regions, driving their continued demand. For example, rice is a staple in many Asian cultures, while wheat-based products like bread and pasta are central in Western diets.

By Distribution Channel

The wholesale distributors sub-segment dominated the global market share in 2022. Wholesale distributors in the staple food market play a crucial role in the food supply chain, acting as intermediaries between producers (such as farms and manufacturers) and retailers, restaurants, and other end users. Distributors are under pressure to improve supply chain efficiency, focusing on logistics, transportation, and inventory management. This is driven by the need to reduce costs and improve responsiveness to consumer demands. Building strong relationships with retailers, restaurants, and other customers is crucial for wholesale distributors. Providing excellent customer service, consistent product quality, and on-time deliveries are key factors that drive success in this market.

By Region

Asia-Pacific dominated the global staple food market in 2022. The Asia-Pacific region is one of the most densely populated regions globally. As populations grow and urbanization increases, the demand for staple foods rises. Urban consumers often have different dietary needs and buying patterns compared to rural populations, leading to shifts in markets. Many countries in the Asia-Pacific region have seen significant economic growth, leading to higher incomes and changing consumer behavior. As people earn more, they tend to diversify their diets, but the demand for staple foods remains strong due to their central role in traditional diets.

Governments in the region often focus on food security, implementing policies to ensure a steady supply of staple foods. This includes investments in agriculture, subsidies, and regulations to stabilize prices and support local farmers.

Competitive Analysis

The key players profiled in this report include Nestle, Pepsico, Cargill, ADM Company, Coca-cola, AB InBev, JBS S.A., Mondelez, Danone, and Diageo plc. Investment and agreement are common strategies followed by major market players.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the staple food market analysis from 2022 to 2032 to identify the prevailing market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the staple food market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global staple food market trends, key players, market segments, application areas, and market growth strategies.

- Based on region, the Asia-Pacific market registered the highest market share in 2022 and is projected to maintain its position during the staple food market forecast period.

Staple Food Market Report Highlights

| Aspects | Details |

| Market Size By 2032 | USD 3.2 trillion |

| Growth Rate | CAGR of 7.2% |

| Forecast period | 2022 - 2032 |

| Report Pages | 340 |

| By Product Type |

|

| By Nature |

|

| By Distribution Channel |

|

| By Region |

|

| Key Market Players | AB InBev, Nestle, ADM Company, JBS S.A., PepsiCo, Danone, Mondelez, DIAGEO PLC, Coca-Cola, Cargill |

The global staple food market size was valued at USD 1.7 trillion in 2022, and is projected to reach USD 3.2 trillion by 2032.

The global staple food market is projected to grow at a compound annual growth rate of 7.2% from 2023-2032 to reach USD 3.2 trillion by 2032.

The key players profiled in the reports includes Nestle, Pepsico, Cargill, ADM Company, Coca-cola, AB InBev, JBS S.A., Mondelez, Danone, and Diageo plc.

Asia-Pacific dominated in 2022 and is projected to maintain its leading position throughout the forecast period.

Consumers are increasingly prioritizing health and wellness, seeking staple foods that align with healthier lifestyles. This trend involves a growing preference for whole grains, reduced sugar and salt content, plant-based options, and organic foods. Staple food producers that offer healthier alternatives are likely to gain a competitive edge.

Loading Table Of Content...

Loading Research Methodology...