Metal Forging Market Overview - 2034

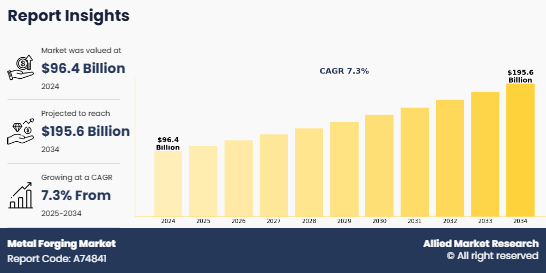

The global metal forging market was valued at $96.4 billion in 2024, and is projected to reach $195.6 billion by 2034, growing at a CAGR of 7.3% from 2025 to 2034. This is driven by rising demand from automotive and aerospace sectors, technological advancements in forging processes, and increased use of high-strength materials in industrial applications. These factors are expected to boost market expansion in the coming years, as industries seek stronger, more durable components to meet evolving performance and safety standards.

Market Dynamics & Insights

- The metal forging industry in Asia-Pacific held a significant share of over 72.7% in 2024.

- The metal forging industry in China is expected to grow significantly at a CAGR of 5.6% from 2025 to 2034

- By raw material, carbon steel segment is one of the dominating segments in the market and accounted for the revenue share of over 41.9% in 2024.

- By application, others application segment is the fastest growing segment in the market.

Market Size & Future Outlook

- 2024 Market Size: $96.4 Billion

- 2034 Projected Market Size: $195.6 Billion

- CAGR (2025-2034): 7.3%

- Asia Pacific: Largest market in 2024

- Asia Pacific: Fastest growing market

Metal forging refers to heating metal at a specific temperature to shape it using force. The metal is heated till it becomes easily deformable, which is then placed between dies or hit with hammer to achieve a desired shape. This process is used since a long time and is adopted to make the metal strong and durable. Metal forging has been known to improve the properties of the metal as well.

Open-die forging refers to process where the metal is compressed between flat or simple-shaped dies that do not completely enclose the material. Closed-die forging refers to the process where the metal is placed in a die that contains a pre-shaped cavity. When the dies close, the metal flows into the cavity and takes the exact shape of the die, producing more precise and complex components. Press forging refers to the process where continuous pressure is applied to the metal using a forging press rather than repeated hammer blows. Roll forging is also used to reduce the thickness and shape of metal bars by passing them through rotating rolls. Further, forging can also be done at room temperature. This is referred to cold forging.

What is Meant by Metal Forging

Metal forging is a manufacturing process that shapes metal using compressive forces, typically applied through hammers, presses, or dies. This process enhances the strength, durability, and structural integrity of metal components by refining their grain structure. Commonly used in industries such as automotive, aerospace, construction, and defense, metal forging produces high-performance parts like crankshafts, gears, and turbine blades. It is classified into open die, closed die, and seamless rolling forging, each suited for specific applications.

Key Market Dynamics

Developments in the automotive industry is one of the major factors that fosters the growth of the metal forging market. Forged components play an important role in vehicles due to their high strength and durability. Thus, the demand for forged metal components surges with increase in global vehicle production, especially in emerging economies like India, China, and Brazil. Further, aircraft manufacturers require components that can withstand extreme stress, temperature variations, and fatigue. Thus, expansion of the aerospace industry also drives the growth of the market. Forged parts provide superior mechanical properties and reliability. This makes them an important part in aerospace applications. Infrastructure projects require strong and durable metal components. Forged steel parts are commonly used in structural applications, heavy machinery, and construction equipment. Therefore, growth of the construction and infrastructure sector also contributes to the demand for forged metal products.

High initial investment cost required for forging equipment, dies, and infrastructure limits the growth of the metal forging market. In addition, fluctuation in raw material prices and changes in global supply and demand and trade policies also deter the market growth.

Despite these restraints, increase in adoption of lightweight materials in automotive and aerospace industries help improve fuel efficiency and reduce emissions. Also, growth of renewable energy sectors surges the demand for forged parts in renewable energy infrastructure. The development of electric vehicles also presents new opportunities for forging companies. These factors are anticipated to foster the growth of the metal forging sector in the upcoming years.

Segment Review

The metal forging market is segmented into raw material, technique, application, and region. By raw material, the market is categorized into carbon steel, aluminum, stainless steel, and others. Depending on technique, the market is classified into open die forging, closed die forging, and ring forging. By application, it is divided into automotive, aerospace & defense, railway, industrial machinery, oil & gas, power generation, and others. Region wise, it is analyzed across North America (U.S., Canada, and Mexico), Europe (Germany, France, Italy, UK, and rest of Europe), Asia-Pacific (China, India, Japan, South Korea, and rest of Asia-Pacific), and Latin America (Brazil, Argentina, Chile, and rest of Latin America), Middle East(Saudi Arabia, UAE, Rest Of GCC, and rest Of Middle East), and Africa (North Africa and Southern Africa).

- The North America metal forging market experienced steady growth, driven by increase in investments in renewable energy, infrastructure modernization, and industrial expansion. The region's strong presence in industries such as automotive, aerospace, power generation, and oil & gas has fueled the demand for high strength, precision-forged components.

- The Europe metal forging market experienced steady growth, driven by advancements in automotive manufacturing, aerospace expansion, renewable energy projects, and infrastructure modernization. Countries such as Germany, France, the UK, and Italy play a crucial role in the global forging industry, with well-established manufacturing bases and a strong emphasis on precision engineering and high-performance materials. The region's commitment to sustainability, electrification, and advanced manufacturing technologies is shaping the future of metal forging. In the automotive sector, Europe remains a global leader, with major automakers such as Volkswagen, BMW, Mercedes-Benz, and Stellantis continuously innovating.

- The Asia-Pacific region is one of the fastest-growing markets for the metal forging industry, driven by rapid industrialization, infrastructure development, and increase in demand for forging from key industries such as automotive, aerospace, construction, and railway. Countries such as China, India, Japan, and South Korea are major contributors to the market due to their strong manufacturing bases and expanding production capacities. The region's robust economic growth and government investments in industrial development have further fueled the demand for forged metal components.

- The Latin America metal forging market witnessed steady growth, driven by increasing investments in automotive production, infrastructure development, energy expansion, and industrial manufacturing. Countries such as Brazil, Chile, and Argentina are at the forefront of the region’s forging industry, benefiting from strong demand in automotive manufacturing, oil & gas, and renewable energy. Government initiatives to boost local production, attract foreign investments, and modernize industries are also supporting the expansion of the forging sector.

What Is the Current Market Size and How Is the Market Expected to Grow?

As per the report by Allied Market Research, the global metal forging market was valued at $96.4 billion in 2024. The market is projected to grow substantially and is expected to reach $195.6 billion by 2034. This growth represents a compound annual growth rate of 7.3% from 2025 to 2034. The growth outlook indicates that the metal forging industry will experience two-fold growth in size during the forecast period.

Increase in demand from the automotive industry, where forged metal components are widely used in engines, transmission systems, crankshafts, and other structural parts fosters the growth of the market. Forged components offer high strength and reliability, which are essential for vehicle performance and safety. Similarly, the aerospace and defense sector relies majorly on forged metals for aircraft components, turbine parts, and landing gear systems, further boosting market demand.

Further, rise in level of industrialization and infrastructure development, particularly in emerging economies also foster the growth of the market. Countries such as India and China are investing heavily in infrastructure projects including bridges, railways, airports, and energy facilities. These projects require strong and durable metal components, which increases the demand for forging processes. As a result, the Asia-Pacific region currently dominates the global metal forging market and is expected to maintain its leading position during the forecast period.

Technological advancements are also playing a key role in market growth. The adoption of advanced forging technologies such as precision forging, automated forging systems, and Industry 4.0 integration has improved production efficiency and reduced material waste. These innovations allow manufacturers to produce complex components with higher accuracy and lower costs, encouraging industries to adopt forging techniques more widely.

Competition Analysis

Competitive analysis and profiles of the major players in the metal forging market is provided in the report. Major companies included in the report include ATI Inc., American Axle & Manufacturing Holdings, Inc., Bruck GmbH, Ellwood Group, Inc., Berkshire Hathaway Inc. (Precision Castparts Corp.), Asahi Forge Corporation, Trenton Forging, Nippon Steel Corporation, Bharat Forge Limited, and Canada Forgings Inc. Moreover, acquisition has been a key development strategy adopted by the key players to increase their market share.

How Are Consumer Preferences Shaping Market Trends?

Consumer preferences play an important role in shaping trends in the metal forging market. Manufacturers are adapting forging processes, materials, and technologies to meet these expectations as industries demand stronger, lighter, and efficient components. One of the major shifts in consumer preference is the demand for high-strength and durable components. Industries such as automotive and aerospace require parts that can withstand extreme pressure, temperature, and mechanical stress. Forged metal products provide superior strength and reliability compared to other manufacturing methods, making them the preferred choice for safety-critical components. As a result, manufacturers are increasingly adopting forging processes to produce components like crankshafts, gears, axles, and turbine parts that meet strict performance standards.

Another important trend is the growing preference for lightweight materials. Modern consumers and industries are focusing on energy efficiency, especially in transportation. Automakers are looking for lightweight materials that can reduce vehicle weight and improve fuel efficiency or battery performance in electric vehicles. This shift has increased the demand for forged aluminum and advanced steel components that provide strength while keeping the overall structure lighter. According to Allied Market Research, the expansion of electric vehicle production is further boosting the use of lightweight forged materials in vehicle manufacturing.

Consumer preferences for high-performance and reliable products are also driving innovation in the metal forging industry. Companies are investing in advanced forging technologies such as precision forging, automated forging systems, and digital manufacturing solutions. These technologies help improve product quality, reduce material waste, and increase production efficiency. As customers demand better performance and consistent quality, manufacturers are adopting these modern technologies to remain competitive in the market.

Whare are the Recent Developments in Metal Forging Industry

- In February 2025, ATI opened its state-of-the-art Additive Manufacturing Products facility in Margate, Florida. The vertically integrated greenfield build includes design, manufacturing, heat treating, machining and inspection capabilities for large-format Additive Manufacturing.

- In October 2024, ATI collaborated with Advanced Forming Research Centre (AFRC) for advanced engineering and materials science to support sustainable air travel. Through this strategy AFRC offers its Future Forge facility for the development of the next generation of materials and process technologies for aircraft. Future Forge features a 2,000-tonne press with open die, closed die, and iso-thermal forging.

What are the Key Benefits for Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the metal forging market analysis from 2024 to 2034 to identify the prevailing Metal Forging Market Opportunity.

- The market research is offered along with information related to Forged Metal key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the metal forging market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global metal forging market trends, High-Strength Forging key players, Metal Forging Market segments, application areas, and market growth strategies, Metal Forging Market Size, Metal Forging Market Share, Metal Forging Market Growth and Metal Forging Market Forecast

Metal Forging Market Report Highlights

| Aspects | Details |

| Market Size By 2034 | USD 195.6 billion |

| Growth Rate | CAGR of 7.3% |

| Forecast period | 2024 - 2034 |

| Report Pages | 339 |

| By Application |

|

| By Raw Material |

|

| By Technique |

|

| By Region |

|

| Key Market Players | Ellwood Group, Inc., Berkshire Hathaway Inc. (Precision Castparts Corp.), Bharat Forge, American Axle & Manufacturing Holdings, Inc., Nippon Steel Corporation, ASAHI FORGE CORPORATION, Trenton Forging, Canada Forgings Inc., Bruck GmbH, ATI |

Adoption of Green and Sustainable Forging Practices, and Integration of Automation and Smart Manufacturing Technologies are the upcoming trends of Metal Forging Market in the globe

Automotive is the leading application of Metal Forging Market

Asia-Pacific is the largest regional market for Metal Forging

In 2024, $96 billion was the estimated industry size of Metal Forging

ATI Inc., American Axle & Manufacturing Holdings, Inc., Bruck GmbH, Ellwood Group, Inc., Berkshire Hathaway Inc. (Precision Castparts Corp.), Asahi Forge Corporation, Trenton Forging, Nippon Steel Corporation, Bharat Forge Limited, and Canada Forgings Inc are the top companies to hold the market share in Metal Forging

Loading Table Of Content...

Loading Research Methodology...