Spatial Computing Market Overview

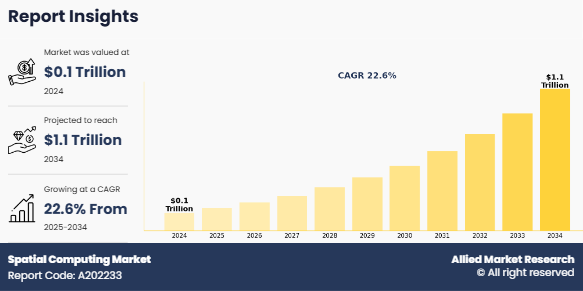

According to latest global spatial computing market insights the market was valued atUSD 135.4 billion in 2024, and is projected to reach USD 1061 billion by 2034, growing at a CAGR of 22.6% from 2025 to 2034.

Spatial computing involves the use of technologies and solutions that enable machines to interact with the physical world through spatial awareness and real-time data processing. It integrates advanced technologies such as augmented reality (AR), virtual reality (VR), mixed reality (MR), computer vision, sensors, AI, and 5G to create immersive and interactive digital experiences. Spatial computing is used across various industries including healthcare, manufacturing, retail, education, architecture, and defense for applications such as simulation, training, remote collaboration, and smart infrastructure. The market scope includes hardware, software, and services that support the development, deployment, and adoption of spatial computing solutions. The market is witnessing rapid growth and innovation driven by advancements in connectivity (such as 5G), increased demand for immersive technologies, and enterprise digital transformation, offering significant opportunities for future investment and adoption.

Key Takeaways:

- By Component, the hardware segment held the largest spatial computing market share for 2024.

- By Technology, the artificial intelligence and ML segment held the largest share in the spatial computing market for 2024.

- By End Use Industry, the healthcare segment held the largest share in the spatial computing market for 2024.

- Region-wise, North America held the largest market share in 2024. However, Asia-Pacific is expected to witness the highest CAGR during the forecast period.

Rise in proliferation of standalone devices such as the Apple Vision Pro is one of the significant trends simplifying user interaction by eliminating cables and enhancing mobility, making spatial experiences more accessible especially in gaming. In addition, there is a growing trend in the adoption of cloud gaming coupled with 5G connectivity, enabling high-quality AR/VR experiences on lightweight devices, significantly reducing the need for expensive hardware.

Furthermore, there is rise in emphasis on integrating spatial computing with technologies such as blockchain, NFTs, and the metaverse, which is opening up new opportunities for digital ownership, secure transactions, and more interactive virtual experiences. This integration allows users to create, own, and trade digital assets in immersive environments, enhancing the value and functionality of spatial computing across industries such as gaming, real estate, retail, and entertainment. In addition, cross-industry collaborations among gaming, tech, retail, and education sectors are gaining traction, expanding the reach and innovation of spatial computing across diverse markets.

Segment Review

The spatial computing market is segmented on the basis of component, technology, end user industry, and region. By component, it is bifurcated into life software and hardware. By technology, it is divided into artificial intelligence and ML, augmented reality, virtual reality, mixed reality, and others. By end user industry, it is classified into healthcare, architecture, engineering, and construction (aec), aerospace and defense, automotive, gaming, and others. By region, it is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

On the basis of component, the hardware segment dominated the spatial computing market size in 2024, driven by widespread adoption of AR/VR headsets, spatial sensors, and advanced imaging devices across industries like healthcare, manufacturing, and entertainment. However, the software segment is expected to grow at the highest rate during the forecast period, owing to increased demand for AI-enabled spatial computing platforms, cloud-based applications, and customized software solutions that enhance real-time data processing and immersive user experiences.

On the basis of region, North America dominated the spatial computing market size in 2024, fueled by significant investments in research and development, presence of leading technology companies, and early adoption of spatial computing technology in sectors such as defense, healthcare, gaming, and manufacturing. However, the Asia-Pacific region is expected to grow at the highest rate during the spatial computing market forecast, owing to rapid urbanization, expansion of 5G infrastructure, government initiatives promoting digital transformation, and rising consumer interest in AR/VR technologies in countries like China, India, Japan, and South Korea.

Top Impacting Factors

Driver

Advancements in AR/VR/MR technologies

Advancements in augmented reality, virtual reality, and mixed reality (AR/VR/MR) significantly drive the growth of the spatial computing market. Rise in hardware innovation and miniaturization accelerates the adoption of spatial computing, powered by high-performance processors such as the Snapdragon XR series, lightweight devices such as the Apple Vision Pro, and advanced sensors including LiDAR and eye tracking. Enhanced battery life further enables extended, uninterrupted use of spatial computing devices and applications across various industries, supporting more immersive and productive user experiences..

In addition, increase in use of 5G and edge computing boosts the spatial computing industry, enabling real-time responses, low-latency interaction, and faster local processing for seamless AR and MR experiences. Furthermore, the integration of AI and machine learning enhances spatial computing by enabling smarter environment recognition, predictive analytics, and more natural user interactions, making applications more adaptive and efficient. These factors are expected to contribute to the increased adoption of advanced technological solutions.

Moreover, spatial computing is increasingly adopted in enterprise and industrial sectors for use cases such as remote assistance, training, design, healthcare, and manufacturing. It offers high return on investment (ROI) by reducing costs, improving efficiency, and increasing workplace safety. In addition, the growth of the metaverse drives spatial computing market demand for shared 3D spaces, accelerating AR/VR/MR growth. Interest in virtual collaboration, training, and entertainment is rapidly expanding across both enterprise and consumer sectors.

For instance, in April 2024, Tencent Cloud partnered with Metavision, aimed at building advanced 3D visual and interactive experiences. This collaboration focuses on integrating immersive spatial computing, AI-generated content (AIGC), and XR technologies to support applications in areas such as e-sports, e-commerce, and virtual conferencing. Tencent Cloud is expected to provide infrastructure, AI capabilities, and 3D space modeling to power Metavision‐™s platforms, including its immersive spatial interaction engine, Fox Engine, and the 3D digital conference system, Fox Space. The partnership is expected to expand Metavision global reach and enhance user experiences across multiple industries, further boosting the spatial computing market growth.

Restraints

High costs of implementation

The major challenge for the growth of the spatial computing market is the high initial cost required to develop, deploy, and integrate advanced hardware, software, and infrastructure, which can be a barrier for widespread adoption of spatial computing technologies and solutions, especially among small and mid-sized enterprises. Spatial computing relies on a range of cutting-edge technologies, including AR/VR headsets, LiDAR sensors, edge computing infrastructure, and high-performance processors. These components often come with substantial costs, not only in terms of purchasing but also in terms of integration, customization, and maintenance. For organizations with limited budgets, the high cost of adopting spatial computing seems too risky, especially when the return on investment (ROI) is uncertain or difficult to quantify in the early stages.

In addition, implementing spatial computing solutions typically requires specialized technical skills, further increasing operational and training costs. As a result, some companies often delay adoption or opt for partial implementations, limiting the technology full potential. Furthermore, the need for ongoing upgrades and scalability significantly adds to the financial and operational challenges of adopting spatial computing. As technology rapidly evolves, organizations must frequently invest in updated hardware, software, and cybersecurity to ensure optimal performance and user experience. This continuous demand strains IT budgets and resources, especially for smaller companies that often lack the infrastructure or expertise to manage complex spatial systems. Expanding these solutions across multiple sites or departments also brings added costs for training, integration, and network upgrades. To address these challenges, collaboration among technology providers, governments, and investors is essential to make spatial computing more accessible and affordable. Solutions for overcoming cost and accessibility barriers could include modular systems that allow gradual scaling, flexible pricing models such as subscriptions or pay-as-you-go, and public funding or incentives to support innovation, especially for small and mid-sized businesses that often lack the resources for large-scale adoption.

Opportunity

Incorporation of spatial computing and adjacent technologies in aerospace & defense sector

The incorporation of spatial computing and adjacent technologies such as artificial intelligence (AI), Internet of Things (IoT), edge computing, 5G connectivity, and advanced sensors in aerospace & defense sector present numerous opportunities in spatial computing market to expand, as these technologies enhance training, boost situational awareness, streamline maintenance, and improve mission planning through immersive and real-time technologies. The increase in the adoption of augmented and virtual reality technologies in training and simulation offers immersive, cost-effective alternatives to traditional methods. These advanced technologies allow pilots, military personnel, and maintenance crews to engage in realistic, high-fidelity simulations of complex flight or combat scenarios. AR and VR reduce operational costs and significantly improve safety & readiness by minimizing reliance on expensive physical setups and live exercises. In addition, in aerospace manufacturing and maintenance, spatial computing enhances precision, collaboration, and efficiency. AR headsets provide technicians with real-time schematics and instructions, reducing errors and speeding up workflows. Remote experts guide operations through mixed-reality tools, essential for field units and remote facilities.

Moreover, the use of digital twins in aerospace enables virtual modeling of physical systems for enhanced design, real-time monitoring, and predictive maintenance, allowing for early fault detection, performance optimization, and extended asset life, improving operational efficiency and mission readiness. In addition, the surge in the adoption of spatial computing in defense enhances situational awareness and decision-making. AR headsets with spatial mapping deliver real-time data for navigation and threat detection, while AI and edge computing enable rapid, informed responses on the battlefield.

Furthermore, the upsurge in the adoption of adjacent technologies such as 5G, IoT, and cloud computing is accelerating the growth of spatial computing by enabling faster data transmission, real-time analytics, and scalable infrastructure, driving innovation and efficiency in the aerospace and defense sector. For instance, in August 2024, JEH Aerospace partnered with GridRaster to modernize aerospace manufacturing using Spatial AI and AR/VR technologies. Their collaboration focuses on immersive training, precision-guided inspections, and real-time work assistance. They aim to boost efficiency, reduce errors, and build the foundation for the next generation of future factories by integrating digital overlays and intelligent XR tools. This partnership is expected to set a new standard in aerospace manufacturing by boosting productivity, improving quality control, and accelerating production with immersive, data-driven spatial computing solutions, supporting market expansion.

Competition Analysis:

The report analyzes the profiles of key players operating in the spatial computing market are Microsoft Corporation, Apple Inc., Google LLC, Lenovo Group Limited, Magic Leap, Inc., Intel Corporation, IBM Corporation, NVIDIA Corporation, Qualcomm Technologies, Inc., Trimble Inc., Siemens AG, Amazon Web Services, Inc., Bentley Systems, Incorporated, Magnopus LLC, Anditi., Huawei Technologies Co., Ltd., Agronomeye, Vuzix Corporation, and Vivo Mobile Communications Co., Ltd. These players have adopted various strategies to increase their market penetration and strengthen their position in the spatial computing industry.

Recent Developments in the Spatial computing Market:

In March 2025, UK-based spatial computing technology startup Hadean has announced a collaboration with Google Cloud to integrate Google Gemini family of AI models with its Hadean‐™s spatial platform. The partnership looks to facilitate the creation of highly realistic and responsive simulations, optimising training exercises and planning scenarios to help organisations develop deeper understanding of potential situations

In February 2024, San Diego-based healthcare group Sharp HealthCare announced the launch of a Spatial Computing Center of Excellence in its Prebys Innovation and Education Center that will focus its development efforts on utilizing the Apple Vision Pro augmented reality headset to enhance patient care. Sharp is partnering with EHR vendor Epic and Dutch information analytics firm Elsevier on the project, which will explore how spatial computing could amplify effectiveness and productivity within various specialties and clinical roles.

Key Benefits For Stakeholders:

This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the spatial computing market analysis from 2024 to 2034 to identify the prevailing spatial computing market opportunity.

The market research is offered along with information related to key drivers, restraints, and opportunities.

Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

In-depth analysis of the spatial computing market segmentation assists to determine the prevailing market opportunities.

Major countries in each region are mapped according to their revenue contribution to the global market.

Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

The report includes the analysis of the regional as well as global spatial computing market trends, key players, market segments, application areas, and market growth strategies.

Spatial Computing Market Report Highlights

| Aspects | Details |

| Market Size By 2034 | USD 1061 billion |

| Growth Rate | CAGR of 22.6% |

| Forecast period | 2024 - 2034 |

| Report Pages | 249 |

| By End Use Industry |

|

| By Component |

|

| By Technology |

|

| By Region |

|

| Key Market Players | NVIDIA Corporation, Apple Inc., Magnopus LLC, Microsoft Corporation, Huawei Technologies Co., Ltd., Vivo Mobile Communications Co., Ltd, IBM Corporation, Qualcomm Technologies, Inc., Bentley Systems, Incorporated, Lenovo Group Limited, Siemens AG, Amazon Web Services, Inc., Trimble Inc., Vuzix Corporation, Intel Corporation, Agronomeye, Google LLC, Magic Leap, Inc., Anditi. |

Analyst Review

The spatial computing market is experiencing significant growth, driven by the increasing demand for immersive and interactive technologies that enhance user experience and operational efficiency. With the rapid evolution of AR, VR, and MR applications, organizations across sectors such as healthcare, retail, education, and manufacturing are adopting spatial computing to enable real-time collaboration, improve training processes, and streamline workflows. The expansion of 5G connectivity and integration with AI and IoT are further accelerating innovation and scalability. In addition, smart infrastructure initiatives supported by governments worldwide are contributing to widespread adoption of spatial computing technologies in urban planning, transportation, and public services. This ongoing technological advancement is expected to further fuel market growth in the coming years.

Furthermore, technological advancements are playing a pivotal role in accelerating the growth of the spatial computing market. Innovations in AR, VR, MR, and real-time 3D rendering technologies are enabling more seamless, immersive, and realistic user experiences across various applications. The integration of spatial computing with artificial intelligence, machine learning, and Internet of Things (IoT) is enhancing data processing, environment mapping, and predictive capabilities, making solutions smarter and more responsive. These advancements are not only improving productivity and decision-making in industries such as healthcare, automotive, manufacturing, and retail, however, also creating new possibilities in immersive entertainment and seamless virtual collaboration. As hardware becomes more affordable and software more sophisticated, spatial computing is transitioning from niche use cases to mainstream adoption, unlocking substantial economic and operational value.

Moreover, government policies and regulations aimed at advancing digital transformation and technological innovation are significantly driving the growth of the spatial computing market. Across various regions, governments are actively promoting the adoption of spatial computing technologies such as AR, VR, and mixed reality, to enhance productivity, foster innovation, and improve public services in sectors such as healthcare, education, defense, and urban planning. Initiatives including R&D funding, innovation grants, and infrastructure development, especially in support of 5G networks, are accelerating the deployment of spatial computing solutions. However, the market still faces challenges, particularly in areas such as regulatory compliance, data privacy, and the absence of standardized protocols for interoperability and safety. Concerns over the ethical use of immersive technologies and the protection of sensitive user data also persist. Despite these challenges, the spatial computing market is poised for strong growth, especially as industries increasingly seek immersive, intelligent, and scalable digital tools to drive operational efficiency and enhance user engagement.

The Spatial computing Market is estimated to grow at a CAGR of 22.6% from 2025 to 2034.

The Spatial computing Market is projected to reach $1,061 billion by 2034.

The Spatial computing Market is expected to witness notable growth include rise rise in proliferation of standalone devices such as the Apple Vision Pro.

The key players profiled in the report include Microsoft Corporation, Apple Inc., Google LLC, Lenovo Group Limited, Magic Leap, Inc., Intel Corporation, IBM Corporation, NVIDIA Corporation, Qualcomm Technologies, Inc., Trimble Inc., Siemens AG, Amazon Web Services, Inc., Bentley Systems, Incorporated, Magnopus LLC, Anditi., Huawei Technologies Co., Ltd., Agronomeye, Vuzix Corporation, and Vivo Mobile Communications Co., Ltd.

The key growth strategies of Spatial computing market players include product portfolio expansion, mergers & acquisitions, agreements, geographical expansion, and collaborations.

Loading Table Of Content...

Loading Research Methodology...