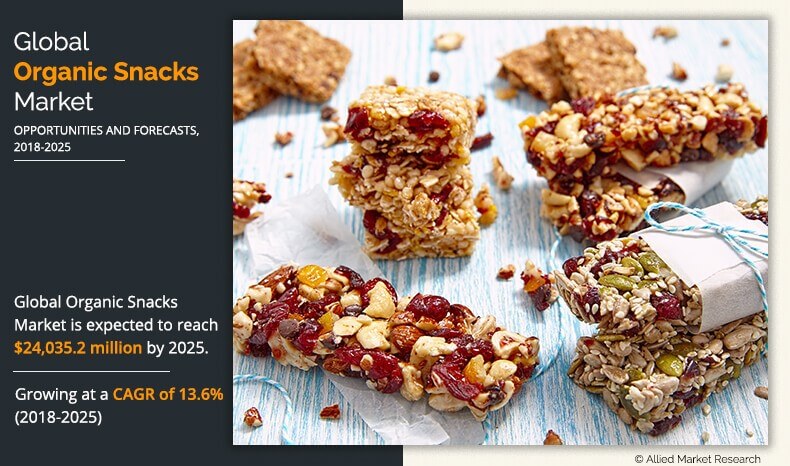

Organic Snacks Market Outlook - 2025

The global organic snacks market was valued at $8,783.2 million in 2017, and is expected to garner $24,035.2 million by 2025, registering a CAGR of 13.6% from 2018 to 2025. Snacks are small servings of food eaten between main meals. Organic snacks are produced organically using organic-certified ingredients that do not contain artificial additives and genetically modified organisms (GMOs). Organic snack foods are products that contain nutritious and healthy ingredients such as proteins, vitamins, and minerals. The organic snack foods such as potato chips, tortilla chips, and corn chips; bakery products such as pancakes, bagel, pretzels, and cookies; and confectionery such as candies, chocolates, raisins, etc. contain organic ingredients that are nutritious and gluten-free as compared with conventional snacks.

Increase in demand and consumption of organic foods in the emerging markets of Asia-Pacific such as India and China has significantly fueled the growth of the global organic snacks market. Furthermore, rise in disposable income and change in lifestyle & food habits further boost the organic snacks market growth. Moreover, rapid increase in number of large retail chains, including hypermarkets and supermarkets, propels the demand for organic snacks. In addition, rise in inclination for readymade and convenient food products, increase in spending capacity of people, and growth in demand for organic food increase the demand for organic snacks, thereby accelerating the organic snacks market growth. However, high cost of production hampers the widespread adoption and act as the major restraint for the global organic snacks market. On the contrary, rise in disposable income and increase in willingness of people on buying premium and environment-friendly products in the emerging nations are expected to provide opportunities for the growth in the coming years.

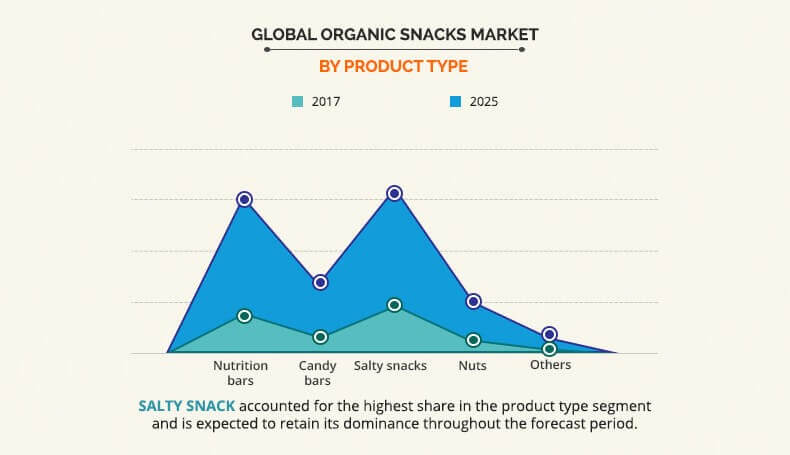

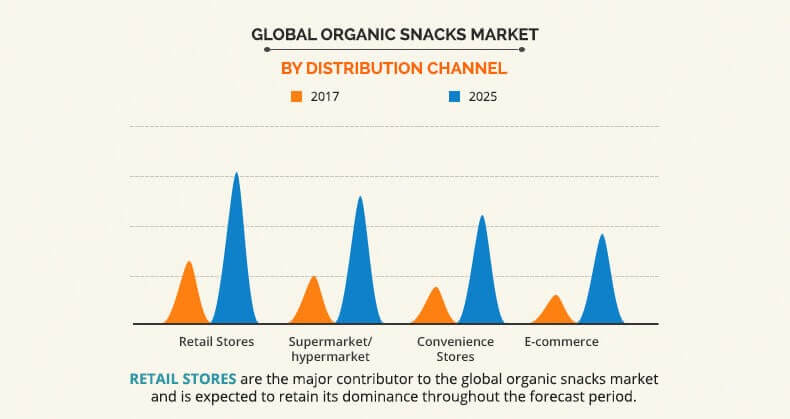

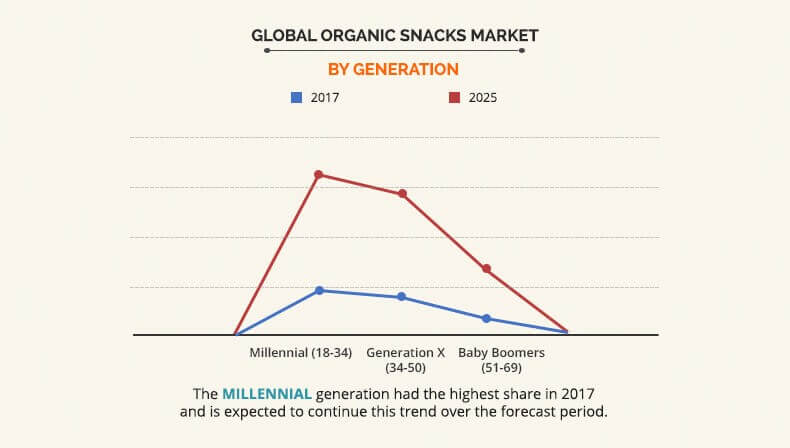

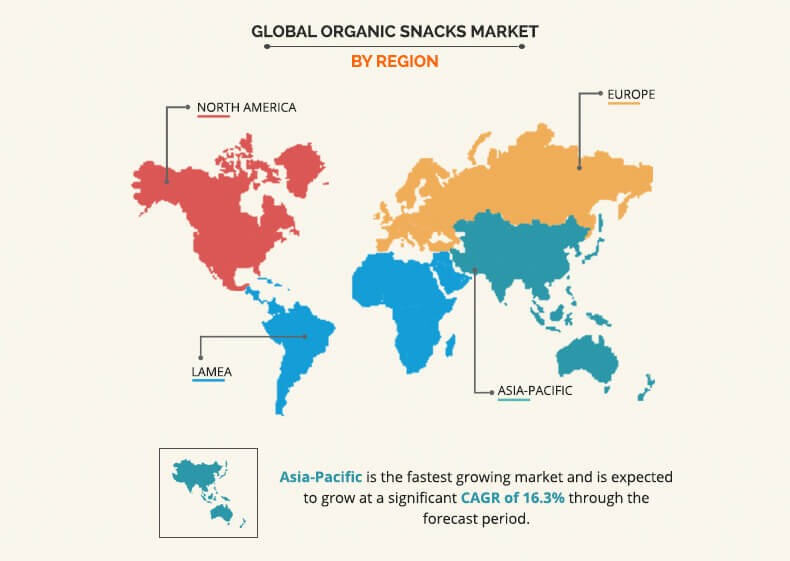

The report segments the global organic snacks market based on product type, distribution channel, generation, and region. Based on type, the market has been bifurcated into nutrition bars, candy bar, salty snacks, nuts, and others. Based on distribution channel, the market has been segmented into retail stores, supermarket/hypermarket, convenience stores, and e-commerce. Based on generation, the market has been classified into millennial with age ranging between 18 and 34 years, generation X with age ranging between 34 and 50 years, and baby boomers having ages between 51 and 69 years. By region, the global organic snacks market has been studied and analyzed across North America, Europe, Asia-Pacific, and LAMEA.

In 2017, the salty snack segment accounted for the highest share in the product type segment. The market for salty snacks is driven by increase in consumption of convenient food items and easy availability of such products all over the world. The ingredient used to make these products are organic and are considered healthy that goes in line with the trend of consuming healthy food, which further adds to the popularity of this product in the global market. The candy bars segment is expected to witness the substantial growth with CAGR of 15.2% throughout the forecast period. This was attributed to organic candy bars having no additives and being healthier alternative to the regular candy bars. This character of being less harmful to the health act as the major driving factor for the candy bar category in the product type segment.

In 2017, the retail stores dominated the distribution channel segment in the organic snacks market. This was attributed to favorable demography and rise in inclination toward healthy snacking option boost the growth of the market. In retail stores, customers can check and compare products before buying and can own them immediately. This option of having choice combined with improving retail infrastructure all around the world supplements the growth of the retail store segment in the organic snacks market.

In 2017, the millennial generation had the highest organic snacks market share and is expected to continue this trend over the forecast period. This was attributed to millennials having had more affinity consumer packaged products such as the organic snacks. Moreover, increase in concerns about health and body image in this generation has also aided the growth of organic snacks.

In 2017, North America is expected to dominate the market for organic snacks due to rise in inclination for on-the-go snacking and a growing demand for organic food. According to the Organisation for Economic Co-operation and Development (OECD), adult obesity rates in 2017 were highest in the U.S. and Mexico. This can be attributed to the high consumption of carbohydrate- and fat-rich snacks. The growing trends of low-calorie snacks and snacks with natural additives are expected to boost the growth of the regional organic snacks market during the forecast period.

Players have adopted product innovations as their key strategies to increase their market share and to remain competitive in the market. The leading players in the organic snacks industry focus on providing customized solution to consumers as their key strategies to gain a significant market share globally. The key players profiled in the report include Pure Organic, PRANA, Made in Nature, Kadac Pty Ltd, Navitas Naturals, Hormel Foods, Hain Celestial, Conagra Brands, General Mills, and Woodstock Farms Manufacturing.

The other market players (not profiled in this report) include SunOpta, Simple Squares, YummyEarth, Inc., Utz Quality Food, LLC, Eat Real, Creative Snacks Co., NurturMe, Annies Homegrown Inc, Navitas Organics, Clif Bar & Company, My Super Foods, Sprout, Peeled Snacks, Beanitos Inc., Late July Snacks LLC, 8 Rabbits, Cussons Australia Pty Ltd, Kraft Heinz, Kewpie Corporations, Louisville Vegan Jerky Co., and Organic Food Bar.

Key Benefits for Organic Snacks Market:

- The report provides a quantitative analysis of the current organic snacks market trends, estimations, and dynamics of the market size from 2017 to 2025 to identify the prevailing market opportunities.

- The key countries in all the major regions are mapped based on their market share.

- Porters five forces analysis highlights the potency of buyers and suppliers to enable stakeholders to make profit-oriented business decisions and strengthen their supplierbuyer network.

- In-depth analysis and the organic snacks market size and segmentation assists in determining the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global organic snacks market.

- Market player positioning segment facilitates benchmarking and provides a clear understanding of the present position of market players.

- The report includes revenue generated from the sales and organic snacks market forecast across North America, Europe, Asia-Pacific, and LAMEA.

- The organic snacks market report includes the organic snacks market analysis at regional as well as the global level, key players, market segments, application areas, and growth strategies.

- Competitive intelligence of the industry highlights the business practices followed by key players across geographies and the prevailing market opportunities.

Organic Snacks Market Report Highlights

| Aspects | Details |

| By Product Type |

|

| By DISTRIBUTION CHANNEL |

|

| By GENERATION |

|

| By Region |

|

| Key Market Players | General Mills, Pure Organic, PRANA, Made in Nature, Navitas Naturals, Hormel Foods, Woodstock Farms Manufacturing, Hain Celestial, Kadac Pty Ltd, Conagra Brands |

Analyst Review

Globally, the organic snacks market share is estimated to escalate at a higher growth rate due to its preserved nutritional profile.

Based on the interviews of various top-level CXOs of leading companies, the increase in sale of organic snacks is driven by changing consumer’s preference and adoption of organic food consumption trend. Organic snacks are free of any chemical and are known to boost up the immune system thereby improving body’s metabolic functions. Rise in inclination for readymade and convenient food products is increasing the sale of organic snacks in the market as a potential healthy snacks option. The health benefits obtained from organic snacks backed up by its high anti-oxidant content is also supporting its sale among the consumers. Furthermore, increase in consumption of natural food products has a positive impact on the organic snacks market. To meet the consumer’s demand to expand their business organic snacks manufacturers across various regions follow the strategy of improving their existing products as well as increasing the manufacture of flavored organic snacks. This is one of the major factors due to which the demands of organic snacks are experiencing a surge. U.S. is among the dominating countries holding a major share in organic snacks market and exports the product in various other countries, which include China, Canada, Mexico, U.K., and others.

However, as per CXOs’ perspectives, high cost of production hampers the widespread adoption and act as the major restraint for the global organic snacks market.

The global organic snacks market was valued at $8,783.2 million in 2017, and is expected to garner $24,035.2 million by 2025

The global Organic Snacks market is projected to grow at a compound annual growth rate of 13.6% from 2018 to 2025 $24,035.2 million by 2025

Hain Celestial, Pure Organic, Woodstock Farms Manufacturing, Made in Nature, Navitas Naturals, Kadac Pty Ltd, General Mills, PRANA, Conagra Brands, Hormel Foods

North America

Increase in awareness about health, development in the retail structure, and rise in demand for convenience food drive the growth of the global organic snacks market.

Loading Table Of Content...