Radiopharmaceuticals Market Size and Forecast 2023 to 2033

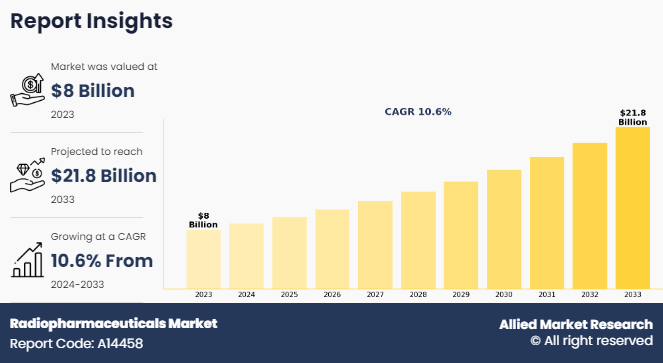

The radiopharmaceuticals market size was valued at $7.9 billion in 2023 and is estimated to reach $21.8 billion by 2033, exhibiting a CAGR of 10.6% from 2024 to 2033. The radiopharmaceuticals market is driven by rise in prevalence of chronic diseases, surge in technological advancements, and increase in diagnostic and therapeutic procedure applications.

Market Dynamics & Insights

- The radiopharmaceuticals industry in North America held a significant share of over 40% in 2023.

- The radiopharmaceuticals industry in China is expected to grow significantly at a CAGR of 12.5% from 2024 to 2033.

- By application, cancer is one of the dominating segment in the market and accounted for the revenue share of over 52.2% in 2023.

- By type, the Technetium 99m segment is the dominant segment in the market in 2023.

Market Size & Future Outlook

- 2023 Market Size: $7,959.65 million

- 2033 Projected Market Size: $21,820.94 million

- CAGR (2024-2033): 10.6%

- North America: Largest market in 2023

- Asia Pacific: Fastest growing market

Market Introduction

Radiopharmaceuticals are drugs that contain radioisotopes that emit radiation. This radiation is detected by imaging equipment outside the body by devices such as gamma cameras or PET scanners. These isotopes are combined with certain molecules to target specific tissues, organs, or physiological processes in the patient’s body. Radiopharmaceuticals are used by healthcare professionals for various applications such as diagnostic imaging in nuclear medical procedures, examination of functions, diagnosis and treatment of different disorders by visualizing and evaluating various life functions.

Key Takeaways

- The radiopharmaceuticals market share study covers 20 countries. The research includes a segment analysis of each country in terms of value for the projected period 2023-2033.

- More than 1, 500 Product & Service literatures, industry releases, annual reports, and other such documents of major radiopharmaceuticals industry participants along with authentic industry journals, trade associations' releases, and government websites have been reviewed for generating high-value industry insights.

- The study integrated high-quality data, professional opinions and analysis, and critical independent perspectives. The research approach is intended to provide a balanced view of global markets and to assist stakeholders in making educated decisions in order to achieve their most ambitious growth objectives.

Key Market Dynamics

Drivers

Technological advancements such as positron emission tomography (PET) and single photon emission computed tomography (SPECT) enable more accurate diagnosis and monitoring of diseases. Thus, these techniques increase the demand for radiopharmaceuticals. Additionally, increase in the number of people suffering from cancer along with other chronic diseases, particularly among elderly individuals, requires diagnostic imaging, which fuels the radiopharmaceuticals market growth. Furthermore, there is increasing awareness about benefits associated with using radiation therapy methods among healthcare providers. This has resulted in higher demand for radiopharmaceuticals, which drives the market growth.

Investment in healthcare infrastructure such as nuclear medicine units comprising modern imaging technology boosts the demand for radiopharmaceuticals market. Increased use of therapeutic applications in areas such as cancer treatment through targeted radionuclide therapy lead to expansion of the radiopharmaceuticals market. In addition, evolving technologies such as precision medicine and personalized healthcare have led to development of novel radiopharmaceuticals tailored to specific patient populations, which drives investment and innovation in the sector.

Restraints

High costs associated with the development, production, and distribution of radiopharmaceuticals hampers their adoption. Radiopharmaceutical manufacturing requires specialized facilities and equipment, along with stringent quality control measures and safety regulations, which contribute to high production costs. Moreover, the short half-lives of many radioisotopes used in radiopharmaceuticals require just-in-time manufacturing and rapid distribution, which significantly increases operational and logistics costs. These elevated expenses can restrict accessibility and affordability—particularly in emerging markets—thereby posing a challenge to the growth and overall forecast of the radiopharmaceuticals market demand.

Opportunities

Rising cancer incidence, expanding nuclear medicine applications, and advancements in targeted therapies are expected to be opportunistic for the radiopharmaceuticals market. One major opportunity lies in theranostics, which combines diagnostic imaging and targeted treatment using the same molecular platform. This approach supports personalized medicine and is gaining rapid adoption in oncology.

The growing development of targeted alpha therapies (TAT) using isotopes such as Actinium-225 offers strong potential for treating resistant and metastatic cancers with improved precision. Expanding PET imaging applications in neurology and cardiology also create new revenue streams.

Emerging markets in Asia-Pacific, Latin America, and the Middle East offer untapped potential due to improving healthcare infrastructure and increasing government investment in nuclear medicine facilities.

Additionally, innovations in isotope production, including cyclotron-based manufacturing, present opportunities to address supply shortages and improve distribution efficiency. Strategic collaborations between biotech firms, hospitals, and research institutions further accelerate product development and commercialization.

How Are Consumer Preferences Shaping Market Trends?

Consumer preferences are increasingly shaping trends in the radiopharmaceuticals market by driving demand for safer, more personalized, and more convenient diagnostic and therapeutic options.

Patients and clinicians are preferring precision medicine approaches. There is growing preference for radiopharmaceuticals that enable tailored diagnosis and therapy (theranostics), allowing doctors to target disease at the molecular level and monitor treatment response in real time. This shift boosts development and adoption of agents that deliver better outcomes with fewer side effects.

Safety and quality of life are top priorities for many patients, especially in oncology. Consumers are more aware of radiation exposure and expect imaging and therapy choices that minimize risk while maximizing benefit. As a result, there is increased demand for high-resolution imaging agents and therapies with limited off-target effects.

Convenience and accessibility matter as patients prefer solutions that reduce hospital visits, such as longer-lasting tracers or outpatient treatment options. This in turn influences clinicians and healthcare systems to adopt technologies that support shorter procedures and easier scheduling.

Greater patient engagement, awareness, and access to health information encourage consumers to ask and know about treatment options and outcomes. This transparency encourages manufacturers and providers to focus on products backed by clear clinical evidence and strong safety profiles, further shaping priorities toward innovation and patient-centric solutions in the radiopharmaceuticals market.

Market Segmentation

The radiopharmaceuticals market is segmented on the basis of type, application, radioisotope, end user, and region. By type, it is segregated into diagnostic, and therapeutic. By application, it is classified into cancer, cardiology and others. On the basis of radioisotope, it is segmented into Iodine I, Gallium 68, Technetium 99m, Fluorine 18, Copper 64, Strontium 89, Yttrium 90, Radium 223, Actinium 225, Lutetium 177, Copper 67, Terbium 161, Zirconium 89, others. By end user, the radiopharmaceuticals market is categorized into hospitals and clinics, medical imaging centers, and others. Region wise, the radiopharmaceuticals market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Which Segment Holds the Largest Radiopharmaceuticals Market Share and Why?

The diagnostic segment holds the largest share of the radiopharmaceutical market. This dominance is primarily driven by the widespread use of nuclear imaging procedures for early and accurate disease detection. Diagnostic radiopharmaceuticals are extensively used in techniques such as Positron Emission Tomography (PET) and Single Photon Emission Computed Tomography (SPECT), which are critical in diagnosing cancer, cardiovascular diseases, neurological disorders, and other chronic conditions.

This segment witnesses high growth owing to prevalence of cancer and heart diseases globally, which require precise imaging for staging, monitoring, and treatment planning. Technetium-99m (used in SPECT) and Fluorine-18 (used in PET scans) are among the most commonly utilized isotopes, which significantly contribute to radiopharmaceuticals market revenue due to their frequent clinical application.

Additionally, diagnostic procedures are performed more frequently than therapeutic nuclear treatments, resulting in higher overall demand. The growing adoption of hybrid imaging systems such as PET/CT and SPECT/CT further supports segment expansion by improving diagnostic accuracy and efficiency.

Favorable reimbursement policies in developed countries and continuous advancements in imaging technology also make the diagnostics segment the largest contributor to the global radiopharmaceuticals market.

How Do Government Policies and Regulations Impact Regional Market Growth?

Government policies and regulations influence regional growth in the radiopharmaceuticals market by shaping approval pathways, reimbursement, production infrastructure, and safety standards.

In North America and Europe, well-established regulatory frameworks such as the FDA in the U.S. and EMA in the EU provide clear pathways for clinical trial approval and market authorization. Strong regulatory procedures ensure product safety and efficacy. However, lengthy approval timelines and high compliance costs can slow the introduction of novel agents, especially smaller biotech entrants.

Reimbursement policies significantly influence utilization. Regions with comprehensive coverage for nuclear imaging and therapeutic radiopharmaceuticals see higher adoption, as there is a less burden on both hospitals and patients regarding expenses. Conversely, in parts of Asia Pacific and Latin America, limited or inconsistent reimbursement can restrain demand despite clinical need.

Government investment in radioisotope production infrastructure—such as funding for cyclotrons or research reactors—boosts regional supply security. For example, national support for domestic isotope production reduces reliance on imports and mitigates global shortages, particularly in emerging markets.

Regulatory harmonization efforts (e.g., ICH guidelines) and expedited review pathways for breakthrough therapies are creating new growth opportunities by accelerating access to innovative diagnostics and treatments. Meanwhile, stringent radiation safety and waste disposal regulations ensure public and environmental protection but require significant compliance effort by manufacturers and healthcare facilities.

How Will Emerging Trends Shape the Future of the Radiopharmaceuticals Market?

Emerging trends are set to significantly transform the future of the radiopharmaceuticals market by accelerating innovation, expanding clinical applications, and improving patient outcomes. One of the most influential trends is the rise of theranostics, which integrates diagnostics and targeted therapy using the same molecular compound. This approach supports precision medicine by enabling disease detection, treatment, and monitoring through a single platform, particularly in oncology.

The growing adoption of targeted alpha therapies (TAT) is also reshaping the landscape. Alpha-emitting isotopes such as Actinium-225 offer high tumor-killing potency with minimal damage to surrounding healthy tissues, opening new possibilities for treating resistant and metastatic cancers.

Advancements in imaging technologies, including digital PET/CT and PET/MRI systems, are improving diagnostic sensitivity and accuracy. These innovations increase demand for advanced radiotracers and support earlier disease detection.

Additionally, investments in radioisotope production infrastructure, such as cyclotrons and modular production facilities, are strengthening supply chains and reducing dependence on aging nuclear reactors. The integration of artificial intelligence in imaging analysis further enhances efficiency and diagnostic precision.

What Technological Innovations Are Creating New Growth Opportunities?

Several technological innovations are creating strong growth opportunities in the radiopharmaceuticals market by improving diagnostic accuracy, therapeutic effectiveness, and production efficiency.

One major advancement is the development of theranostics—agents that combine therapy and diagnostics. This approach uses the same molecule labeled with different radionuclides for imaging and treatment, enabling personalized medicine. For example, Lutetium-177 and Gallium-68 labeled peptides are used for both detecting and treating neuroendocrine tumors, improving patient outcomes.

Next-generation imaging technologies, such as digital PET and hybrid PET/MRI systems, are enhancing sensitivity and image resolution. These allow clinicians to detect diseases at earlier stages and monitor treatment responses more precisely. Better imaging directly increases demand for radiopharmaceutical tracers and supports clinical adoption.

Innovations in radioisotope production—like cyclotron-based methods and small modular reactors—are addressing historic supply shortages of key isotopes such as Technetium-99m and enabling more localized, reliable production. This supports broader geographic accessibility and reduces dependence on aging nuclear reactors.

Additionally, automation in manufacturing is boosting quality and scalability. Automated synthesis modules and advanced quality control systems reduce human error, comply with stringent regulatory standards, and cut production costs.

Finally, progress in targeted alpha therapies (TAT) using alpha-emitting radionuclides (e.g., Actinium-225) is opening new avenues for treating resistant cancers with high therapeutic potential.

Radiopharmaceuticals Market Dynamics

Radiopharmaceuticals market trends include technological advancements such as positron emission tomography (PET) and single photon emission computed tomography (SPECT) that allow more accurate diagnosis and monitoring of diseases; which increase the demand for radiopharmaceuticals in these procedures. Additionally, rise in the number of people suffering from cancer along with other chronic diseases, particularly among elderly individuals, necessitates wider applications as well as diagnostic imaging, thus fueling the market‐™s growth rate. Furthermore, there is increasing knowledge about benefits associated with using radiation therapy methods among healthcare providers which has resulted in higher uptake rates, thereby driving the radiopharmaceuticals market growth.

The radiopharmaceuticals market growth is due to investment in healthcare infrastructure such as nuclear medicine units that have modern imaging technology. Another factor that has created opportunities for growth is the increased use of therapeutic applications in areas such as cancer treatment through targeted radionuclide therapy. The evolving landscape of precision medicine and personalized healthcare has led to the development of novel radiopharmaceuticals tailored to specific patient populations, thus driving innovation and investment in the sector.

However, the high cost associated with the development, production, and distribution of radiopharmaceuticals limits the adoption rate. The specialized facilities and equipment required for radiopharmaceutical manufacturing, along with stringent quality control measures and safety regulations, contribute to high production costs. Additionally, the short half-life of many radioisotopes used in radiopharmaceuticals necessitates just-in-time production and distribution, further adding to the expenses. These high costs can limit accessibility and affordability, particularly in emerging markets, thereby impeding the radiopharmaceuticals market forecast.

The radiopharmaceuticals market analysis is segmented on the basis of type, application, radioisotope, end user, and region. By type, it is segregated into diagnostic, and therapeutic. By application, it is classified into cancer, cardiology and others. On the basis of radioisotope, it is segmented into Iodine I, Gallium 68, Technetium 99m, Fluorine 18, Copper 64, Strontium 89, Yttrium 90, Radium 223, Actinium 225, Lutetium 177, Copper 67, Terbium 161, Zirconium 89, others. By end user, the radiopharmaceuticals sector is categorized into hospitals and clinics, medical imaging centers, and others. Region wise, the radiopharmaceuticals market growth is analyzed across North America (U.S. and Canada), Europe (Germany, UK, France, Spain, Italy, and Rest of Europe), Asia-Pacific (India, China, Australia, Japan, South Korea, Thailand, Malaysia, Indonesia, Singapore, Taiwan, Province Of China, and Rest of Asia-Pacific), and LAMEA (Brazil and Rest of LAMEA).

By Type

The diagnostic segment dominated the radiopharmaceuticals market share in 2023. This is attributed to diagnostic imaging procedures using radiopharmaceuticals play a critical role in disease detection, characterization, and monitoring across various medical specialties. However, the therapeutics segment is expected to register the highest CAGR during the forecast period owing to advancements in targeted radionuclide therapy (TRT) that have expanded the applications of radiopharmaceuticals in the treatment of various cancers and other medical conditions. In addition, increase in prevalence of cancer and other chronic diseases has fueled the demand for novel therapeutic interventions thereby driving the radiopharmaceuticals market opportunity.

By Application

The cancer segment dominated the radiopharmaceuticals market share in 2023 and is expected to register the highest CAGR during the forecast period. This is attributed to the increase in prevalence of cancer, rise in technological advancements, shift towards personalized medicine approaches, and investment in oncology care. In addition, the growing adoption of personalized medicine approaches in oncology, driven by advancements in genomics, molecular profiling, and biomarker identification, is fueling the demand for tailored therapeutic strategies, including radiopharmaceutical-based precision oncology.

By Radioisotope

The Technetium 99m segment dominated the radiopharmaceuticals market size in 2023 and is expected to register the highest CAGR during the forecast period. This is attributed to it being a most widely used radioisotope in nuclear medicine due to its favorable characteristics, including its suitable physical properties, availability from generator systems, and compatibility with a variety of radiopharmaceutical formulations.

By End User

The hospitals and clinics segment dominated the radiopharmaceuticals market share in 2023 and is expected to register the highest CAGR during the forecast period. This is attributed to the increase in prevalence of cancer and other chronic diseases, combined with the aging population, which has led to a growing demand for diagnostic imaging and therapeutic interventions in hospitals and clinics. In addition, advancements in imaging technologies and the development of novel radiopharmaceuticals have expanded the applications of nuclear medicine in hospitals and clinics, thereby supporting the segment growth.

By Region

The radiopharmaceuticals industry is analyzed across North America, Europe, Asia-Pacific, and LAMEA. North America accounted for the largest share in the radiopharmaceuticals market and is expected to remain dominant during the forecast period. This dominance is attributed to its advanced healthcare infrastructure and a well-established pharmaceutical industry, facilitating the development, production, and distribution of radiopharmaceuticals. In addition, favorable regulatory policies and supportive reimbursement frameworks encourage investment in radiopharmaceutical research and development and thereby drive the radiopharmaceuticals market growth in this region. However, the Asia-Pacific region is anticipated to register the highest CAGR during the forecast period. This is attributed to growing healthcare infrastructure, with increased investments in hospitals, diagnostic centers, and research facilities and rise in prevalence of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions.

Competitive Landscape

The report provides an extensive competitive analysis and profiles of the key radiopharmaceuticals market players such as South African Nuclear Energy Corporation (Necsa), Eckert & Ziegler, PRECIRIX, Nihon Medi-Physics Co. Ltd, Isotopia Molecular Imaging, Fusion Pharmaceuticals Inc., Actinium Pharmaceuticals, Inc., Lantheus, Bayer AG, Cardinal Health, Eczacibasi, ITM Isotope Technologies Munich SE, The State Atomic Energy Corporation ROSATOM, Bracco, SOFIE, Clarity Pharmaceuticals, NorthStar Medical Radioisotopes, Telix Pharmaceuticals Limited, GE Healthcare, Curium Pharma, Novartis AG, Jubilant Pharmova Limited, and Eli Lilly and Company. These players have adopted strategies such as agreement, acquisition, expansion, clinical trials, product approval, product upgrade and development to increase their market share and maintain their foothold in the radiopharmaceuticals market.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the radiopharmaceuticals market segments, current trends, estimations, and dynamics of the drug abuse testing market analysis from 2025 to 2033 to identify the prevailing drug abuse testing market opportunity.

- The radiopharmaceuticals market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the drug abuse testing market segmentation assists to determine the prevailing radiopharmaceuticals market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the radiopharmaceuticals market players.

- The report includes the analysis of the regional as well as global drug abuse testing market trends, key players, market segments, application areas, and radiopharmaceuticals market growth strategies.

Radiopharmaceuticals Market Report Highlights

| Aspects | Details |

| Forecast period | 2023 - 2033 |

| Report Pages | 500 |

| By End User |

|

| By Radioisotope |

|

| By Application |

|

| By Type |

|

| By Region |

|

| Key Market Players | Jubilant Pharmova Limited, Fusion Pharmaceuticals Inc., GE Healthcare, Clarity Pharmaceuticals, NorthStar Medical Radioisotopes, Telix Pharmaceuticals Limited, Eczacibasi, Eli Lilly and Company, Eckert & Ziegler, Curium Pharma, ITM Isotope Technologies Munich SE, Novartis AG, Lantheus, Actinium Pharmaceuticals, Inc., Isotopia Molecular Imaging, South African Nuclear Energy Corporation (Necsa), Bracco, Bayer AG, SOFIE, Cardinal Health, Nihon Medi-Physics Co. Ltd, The State Atomic Energy Corporation ROSATOM, PRECIRIX |

Analyst Review

This section provides various opinions of top-level CXOs in the global radiopharmaceuticals market. According to the insights of CXOs, the global radiopharmaceuticals market is driven by surge in prevalence of chronic disease, rise in investments for R&D activities, upsurge in demand for sophisticated healthcare facilities, and rise in healthcare expenditure. However, side effects of radiopharmaceuticals and high cost of development and implementation of radiopharmaceuticals limit the growth of the radiopharmaceuticals market.?

CXOs further added that the key players have adopted various strategies to strengthen their foothold in the competitive market. In addition, ongoing advancements in imaging technology, such as hybrid imaging modalities (PET-CT, SPECT-CT), molecular imaging probes, and imaging software, create opportunities for improved diagnostic accuracy, enhanced visualization, and personalized treatment planning, which further propels the market growth.

Furthermore, North America dominated the market share, in terms of revenue, owing to surge in cases of cancer, easy availability of radiopharmaceuticals, high healthcare expenditure, and strong presence of key players in this region. However, Asia-Pacific is anticipated to witness notable growth owing to an initiative by government & non-governmental organizations (NGOs) to promote awareness regarding use of radiopharmaceuticals and increase in public–private investments in the healthcare sector.

The total market value of radiopharmaceuticals market is $7.9 billion in 2023.

The market value of radiopharmaceuticals market in 2033 is $21.8 billion.

The forecast period for radiopharmaceuticals market is 2024 to 2033.

The base year is 2023 in radiopharmaceuticals market.

North America is accounted for the largest market share in 2023 owing to well established healthcare infrastructure, substantial investments in research and development, and the widespread availability of radiopharmaceuticals products.

Radiopharmaceuticals are pharmaceutical compounds that contain radioactive isotopes, known as radionuclides. These substances are used in nuclear medicine for diagnostic or therapeutic purposes.

The growth of the radiopharmaceuticals market is primarily driven by increasing prevalence of chronic diseases such as cancer and cardiovascular disorders, advancements in radiopharmaceutical research and development, rising demand for personalized medicine, and supportive regulatory frameworks and reimbursement policies

Commonly used radiopharmaceuticals include Technetium-99m (Tc-99m), Fluorine-18 (F-18) for PET imaging, and Iodine-131 (I-131) for thyroid cancer therapy, among others.

Loading Table Of Content...

Loading Research Methodology...